Why Europe Is Creating a New Path for Retirement Savings

Why Europe Is Creating a New Path for Retirement Savings

February 2022

By Xavier van den Brande

and Marvin Vervaart

As Europe’s aging population and existing pension arrangements add mounting pressure on public finances, will the long-awaited Pan-European Personal Pension Product (PEPP) be the accelerator to a more sustainable pension system for Europe?

PEPP at a Glance

- Expected to be effective from March 22, 2022, the new European Union (EU) PEPP offers EU citizens a new voluntary cross-border savings product.

- The use of PEPPs has been introduced as a second regime regulation, and not a directive, so EU Member States must apply it as such.

- A PEPP can be established in any of the EU or European Economic Area (EEA) Member States and promoted across the region on a passported basis. It is accessible to all EU citizens working in or outside the EU or EEA, whether they are employed or self-employed.

Over the next 50 years, the number of individuals of retirement age compared to the working population is forecast to double in Europe. Reforms to national pension systems are deemed essential by many with a special emphasis on increased individual accountability.

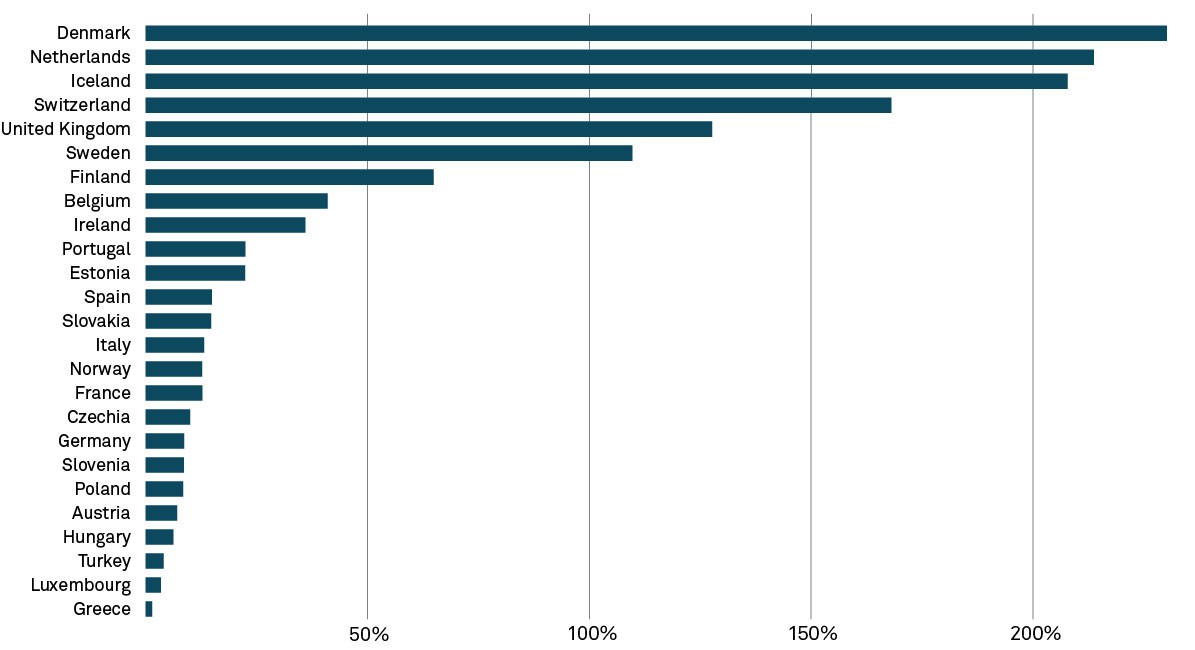

PEPPs are being positioned by the EU as an important new option for EU citizens to save for retirement in an active manner. This may prove particularly relevant in those EU markets that have traditionally lacked a strong pension industry, such as in Eastern and Southern Europe (see Figure 1). In addition, a PEPP could become an important savings tool for the growing number of self-employed such as in the Netherlands.

Figure 1: Pension funds as a share of gross domestic product (GDP)

Source: Statista; data released on Nov 2021; survey period taken in 2020.

As well as helping address the long-term sustainability of the EU pension system through higher individual accountability, PEPPs are expected to yield additional ancillary benefits for the EU – one example would be increased investment into new long-term infrastructure PEPP funds. Essentially, the EU hopes the PEPP will be a key instrument towards achieving more sustainable pensions while promoting regional economic growth and further contributing to the development of the Capital Markets Union.

“Many people don’t start thinking about their retirement income until they are getting close to retirement and for many people this is too late. The reality of today is that many Europeans are probably not saving enough for their retirement to keep their standards of living,” said Sandra Hack, Principal Expert on Policy at the European Insurance and Occupational Pensions Authority (EIOPA).

While PEPPs seem to offer clear benefits conceptually, much uncertainty remains both in terms of design and practical implementation. The industry expects to receive further guidance from EU rule makers on the design, such as the proposed cross-border PEPP tax treatment in the context of heterogeneous national tax regimes.

In the meantime, there are key preliminary considerations for three distinct groups of market participants — consumers, pension providers and custodians — as they navigate the implementation of PEPP.

Consumers

PEPPs are intended to provide consumers with more choice and more competitive financial products, based on a number of intrinsic features.

- Portability – Since PEPP is a cross-border product, consumers can benefit from a single consolidated pension wherever they work and whenever they change their residency.

- Flexibility – Consumers can, in principle, switch providers every five years at a capped cost.

- Choice – Insurance companies, asset managers, pension funds, investment firms and banks can all offer PEPP products. The broad offer is designed to provide maximum choice to consumers.

- Transparency – A PEPP provider is obliged to disclose detailed information to consumers through a pre-purchase Key Information Document. Furthermore, PEPP providers need to provide a personalized pension benefit statement during the product’s lifecycle.

- Consumer protection

- BASIC PEPP: Providers are obliged to offer a basic, default investment option, for which the costs are capped at 1% of the accumulated capital per annum. Basic PEPP will protect consumers’ invested capital.

- Advice: It is mandatory for a provider to offer personalized advice to consumers which can be done digitally.

Plan Sponsors and Providers

The commercial potential of PEPPs is still uncertain, but there are a number of key points for market participants to consider.

From a sponsor perspective, PEPPs offer an attractive solution to multinational corporations that need to consider cross-border pension solutions for their employees, and to corporations in domiciles that traditionally do not have a strong pension provision.

For plan providers, PEPPs create a new savings product that can be passported throughout Europe and possibly third countries on the basis of regulatory equivalence. Given their existing experience in managing investment funds, insurance companies and investment managers – both EU and non-EU based – would appear to be natural providers of PEPPs. A few additional points to consider are:

- “Green PEPPs” are likely to be in demand, boosted by younger generations working across borders. This will benefit institutional investors with strong responsible investment credentials.

- PEPP providers may focus on Eastern and Southern European countries as new growth markets. Distribution partnerships with regional institutions may be a feature.

- Providers could choose traditional fund markets such as Ireland and Luxembourg to launch a PEPP, but they may also consider other developed EU jurisdictions. The Netherlands, for example, has a strong pension tradition and will give providers access to a professional pension market, an experienced regulator and local suppliers with a pension focus.

- Providers should be aware of the fee cap of 1% for the BASIC PEPP and the mandatory requirement to provide personalized advice to members. These reflect efforts to protect users, but they can be potential barriers for market entry.

- With an eye on cost efficiency and user experience, providers may leverage existing practices from the wealth management industry, including robo-advice.

- Technology companies are looking to introduce PEPP SaaS (Software as a Service) and PEPP IaaS (Infrastructure as a Service) offerings that comply with EU regulations – and that non-EU providers can lease to launch their PEPPs. .

“Lacking a strong complementary pension system, the PEPP is a great opportunity to revamp saving for retirement in Portugal,” said Valdemar Duarte, General Manager of Ageas Pensões. “It is a simple, flexible, modern and cost-effective product with strong investor protection. Given the mandatory 1% cost cap, a certain minimum scale is required for commercial success and up-front tax incentives should be considered.”

Custodian Point of View

Notably, PEPPs do not differ in principle from fund structures that custodians are servicing today. In practice, this means custodians can position their core fund service offering to support PEPPs via custody, fund accounting and transfer agency. However, PEPPs include some components that will allow custodians to provide additional value-added services – these include, but are not limited to Environmental, Social and Governance (ESG) data and analytics services, customized reporting and compliance monitoring. Additional areas where custodians may play an important role for PEPP providers are:

- Cost control: Transparency is key within PEPPs when it comes to cost and custodians can provide the required tools for monitoring and control.

- Depository: While PEPP legislation does not prescribe the mandatory appointment of a depository, some industry participants argue that an independent “second line of defense” is recommended to protect consumers. It is important to remember that EU law states the depository is appointed in the jurisdiction of registration, but freedom of services allows this depository to offer its services throughout the EU.

- Investment strategy and fund structures: The need to set up sub-accounts to comply with national systems of taxation can likely be supported through virtual pooling and unitization structures. This should help minimize operational complexity and impact on investment policy.

“Given the focus on sustainability, plan sponsors and providers need transparency to make ESG investing a reality. Custodians can assist by acting as the single ESG data hub, which plans can leverage for stakeholder reporting and analysis of ESG risks and opportunities” said Hani Kablawi, Chairman of International at BNY Mellon.

Europe Paves the Way

While there is still uncertainty over how PEPPs will work in practice, more clarity will emerge throughout the year. Success will depend on strong supervision and close cooperation between national regulators across EU Member States – and effective communication to market participants.

It’s expected some market participants will begin launching PEPPs in the second half of this year to capture new flows. As they consider their options in this process, custodians will be well placed to advise and guide PEPP providers on the best operational outcomes for both themselves and their customers alike.

Learn more by visiting BNY Mellon Asset Owner Academy, a platform to share bold ideas, insights and learnings to help asset owners stay agile as they transform their operating models.

Asset Servicing Global Disclosure

© 2022 The Bank of New York Mellon Corporation. All rights reserved.