THE ALTA REPORT.

A quarterly compilation derived from our unique vantage point at the intersection of markets. Touching approximately 20% of the world’s investable assets gives us insight into key trends, helping you navigate the future arc of markets and macro developments.

HEADLINES

01

Equity Demand Shows

02

Endowments Raise Cash Allocations

03

US Fixed Income Demand Begins to Wane

Dash for Cash

SUMMARY

The aftereffects of the recent banking turmoil appear contained, for now. Cash was withdrawn from small and midsize banks and placed into government money market mutual funds (MMF) at a pace not seen since the onset of the pandemic in 2020. Deposits at some large banks also increased, reflecting the search for safety. MMF inflows were invested in short-term Treasurys and repos, including repos at the Fed. However, the growing margin balances pledged between counterparties in non-cleared derivatives held in our margin segregation business was an important indicator of the overall resilience of the financial system.

Money in Motion

As deposits migrated mostly out of smaller and midsize banks, the cash largely made its way into MMFs, Global Systemically Important Banks and short-term Treasury securities. Our LiquidityDirect short-end investment portal logged an increase of up to 16% in MMF flows in mid-March. Almost all of that flow went into government MMFs, which typically gain in popularity in times of market uncertainty. We suspect MMFs are likely to remain popular for some time as investors look for higher yields during a period of market volatility.

MMF Balance Growth, LiquidityDirect vs. Industry

Yield Dispersion Fades

Rising rates were already benefiting MMFs as investors were looking for additional yield on their cash, but not all MMFs performed equally. The Fed has been raising interest rates for the past year, giving MMF portfolio managers a chance to show their mettle when picking individual securities. At one point in mid-February, there was a divergence of up to 21bp in the yields of two government MMFs (see chart). Many funds were locked into longer-duration positions, which became problematic as interest rates rose. By contrast, funds that were short duration benefited from the Fed’s rate hikes. The average gap (yield dispersion) narrowed to 12bp as of March 28 as the banking situation prompted more buying in the short end.

MMF Yield Dispersion

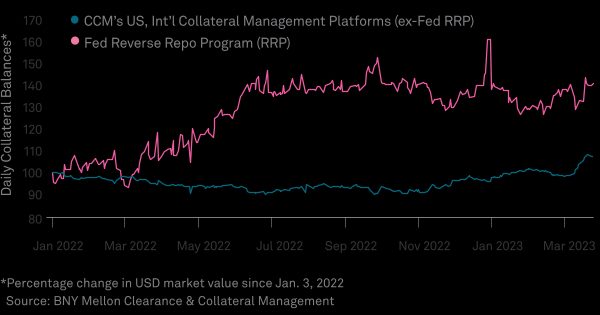

Collateral Balances Climb

Our collateral balances have risen to record levels. The movement of cash from smaller banks to secured investments such as repos and MMFs also drove record participation levels in the Fed’s reverse repo (RRP) facility. The increase in repos with the Fed squeezed out traditional triparty repo trades with broker-dealers. However, overall collateral balances across our US and international triparty businesses each climbed 8% between March 1 and April 5, reaching new highs in our records.

CCM Daily Collateral Balances

Regional Banks, Shorted

Our Agency Securities Finance business experienced plenty of volatility in March. There was a 35% increase in the demand for borrowing regional bank equities to facilitate short sales or hedging by our hedge fund clients from March 1 to April 11.

Cost to Borrow US Regional Bank Equities

WHAT'S NEXT

Watching for Wobbles

Investors are waiting for the next shoe to drop. In addition to concerns about a potential recession, however mild, certain segments of the markets still face a variety of uncertainties, including commercial real estate, where we are seeing some signs of potential weakening, and private debt markets, because of higher rates and the potential for pressure on term loans that were underwritten in a low-interest-rate environment. The concern is that these highly leveraged borrowers will be facing a more challenging operating environment, which could result in preemptive drawings under their lines of credit. In addition, they could be shut out of the leveraged loan and high-yield markets. The upshot of all this could be tighter credit conditions, including lending standards and higher credit spreads.

Contagion Fears Abate

The recent banking troubles are unlikely to be systemic. We think the underlying health of the banking system remains sound, judging from bank capital and liquidity levels as well as margin practices. There are some additional protections provided by the $205bn in regulatory collateral, or initial margin, pledged between counterparties of non-cleared derivatives in our margin segregation business that were not there in the 2007–2009 financial crisis. The chart to the right depicts the non-cleared regulatory initial margin balances we see in our Margin Services business. Of the total, $170bn is non-cleared margin posted by medium to large financial institutions, such as broker-dealers and banks. Small regional banks are not posting, so the margin is not protecting counterparties that have exposure to them.

Non-Cleared Margin Balances

Rates & Recession

SUMMARY

Markets have been operating without much conviction, in part because macro themes are reversing as quickly as they appear. It is still unclear, for example, whether the recent banking issues will have spillover effects into the broader economy or how much tighter it has made credit conditions. If growth and employment are negatively impacted by more conservative lending practices, this could hit consumption, potentially bringing inflation lower as well.

Our view is that the Fed is leaning toward more policy firming in the short term — with a May hike of 25bp possible — and then a pause as evidence accumulates that the banking sector woes have not spread. We believe that the European Central Bank will continue tightening in the short term. If credit is only modestly crimped, and central bank liquidity goes where it’s needed, inflation should moderate. But for as long as higher rates pinch corporate profits (as the latest US corporate earnings appear to show) and prices hurt purchasing power, inflation volatility is set to remain a worldwide problem. Ideally, the tightening generates only a brief slowdown (mild recession) that brings inflation back toward the Fed’s 2% target. With all these potential scenarios yet to play out, active management could be useful in this environment. Breaking it down…

Inflation Trading Recedes

With concerns about inflation receding, and the rate cycle likely turning from hikes to cuts, our iFlow platform shows that institutional investors are no longer putting money into US stocks that perform well in high inflationary periods, as they were in the first half of 2022. In fact, inflation-related equity trading fell to -0.5 as of April 12, from 0.25 last July. The question now is just how slowly inflation will fall.

Demand for Inflation-Related US Equities

Timing TIPS, Tricky

How to protect against inflation has also been a point of focus. Our US asset owner activities show that among the 41 US asset owners invested in inflation-linked bonds and Treasury inflation-protected securities (TIPS), their allocations fell by about a fifth to 2.7% in February 2023 from 3.3% in February 2022, factoring in performance and decisions to change the portfolio.

Allocation to TIPS, Inflation-Linked Bonds

Rate Hedges

Meanwhile, clients are mostly positioned for US rates to eventually fall below 4.5%, based on activity from our Asset Servicing division, which prices over-the-counter interest rate swaps (average tenor 11 years). Big banks, pension funds and insurance companies that have been collecting higher interest payments on longer-term bonds are hedging against any downside move in rates, particularly in Europe, where pension liabilities have been large for years as a result of low bond yields.

Yield Curve Control

The effects of potential policy changes in Japan are already reverberating. Some policymakers there have talked about ending their long-held practice of buying government bonds (JGBs) sometime around June to depress yields, an effort designed to counteract low inflation. While overall triparty balances have grown, we are observing international collateral providers on our triparty collateral management platform (mostly broker-dealers) scaling back their yen-denominated JGB balances, pulling out of medium-term bonds (2–10yrs) and exchanging them for other collateral types. The par value held by those international collateral providers in JGB had fallen about 40% from its peak in September but has since recovered slightly. Meanwhile, Japanese provider holdings have been relatively steady in comparison, falling only about 20% from the peak before stabilizing recently.

Japanese Yen Collateral Balances

Carry Trade Weakening

Some conviction is forming over the yen’s outlook. With US dollar yields sinking in March, it appears that the new outlook would be for the yen to appreciate, with Japanese investors now more likely to sell dollars and move back into yen as the short yen/long dollar carry trade becomes less attractive. Where we price FX options in our Asset Servicing business, most of the clients are positioned with dollar puts around USD/JPY 130.

USD/JPY Options by Maturity and Strike

Recession Watch

Another example of oscillation is cyclical vs. defensive stocks. Since early 2021, flows have zigzagged between cyclical and defensive stocks, landing between +7 and -6 in our index, indicating that investors are uncertain about whether the US economy will reaccelerate or decelerate.

Comparison of Cyclical to Defensive Stocks

Markets have been operating without much conviction, in part because macro themes are reversing as quickly as they appear

Debt Ceiling

X Date Dilemma

When it comes to debt ceiling negotiations, the climax “X date” when the Treasury runs out of money may be sooner than the market thinks (current view is August 15, with payments due on several notes and bonds). With the Fed tightening rapidly in 2022, capital losses on investments were the second worst in records going back 65 years. Offsets on taxes from these losses may be sufficient to lower the effective tax rate by about 5 percentage points. We can’t be sure that households will harvest all these losses for tax purposes, but if they did, it would represent a $500 billion miss on Treasury revenue that would more than offset the effect of higher income last year. The conclusion is that politicians may likely have much less time than they expect in negotiating a safe landing on the debt ceiling. An earlier X date puts anyone at risk with exposure to bills maturing from July through all of August.

Emerging Markets

SUMMARY

Overall, emerging markets (EMs) have been surprisingly resilient given the recent flight to safety. They came into 2023 rallying because China was reopening after lockdown and the US dollar was weakening. They dipped briefly in February when the dollar strengthened and investors sold out of some early-year positions, but now appear on a more comfortable footing again. There is a question, however, over how long the calm lasts given the possibility of a US downturn that could constrain worldwide growth, as well as the potential that activity growth related to China’s reopening starts to slow. Breaking it down…

EM Currency Inflows

EM currencies are enjoying inflows after many of these economies raised rates further than the US and Europe and attracted foreign investment. But if the consensus view is that the US and Europe keep policy firmer for longer, that could be a challenge to some EM markets. Apart from brief periods in February and early March, where scored flows dipped to an index level of -0.3 — the lowest since October 2022 — flows into EM currencies have outperformed flows into G10 currencies.

Institutional EM/G10 Currency Flows

China Rising

China’s reopening is an anchor theme this year, with the MSCI China index rising nearly 60% between November 1 and January 27 in anticipation of greater economic activity and higher corporate profits. Investment flows are responding slowly, however.

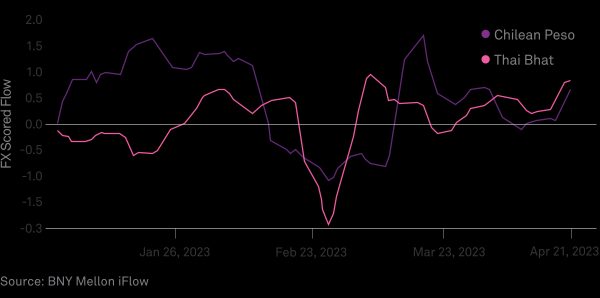

Chilean Peso, Thai Baht

One proxy for China’s growth outlook is the Chilean peso. Our iFlow data shows that investors have been anticipating more demand for lithium and copper, both exports of Chile, for Chinese electric vehicles, infrastructure and property development. Another proxy is Thai baht, recent inflows into which have been an indicator of China tourism demand, which is recovering after three years of effectively closed borders.

Institutional Flows into Chilean Peso

Border Crossings

Traffic patterns are another useful indicator for the China rebound story. An analysis by Newton Investment Management concludes that daily cross-border traffic between mainland China and Hong Kong has recovered to around half of pre-COVID-19 levels. Residential real estate sales are recovering too, and are now back into positive territory on a year-on-year basis.

Border Crossings – Mainland China into HK vs. Normalized Levels

There is a question over how long the calm lasts given the possibility of a US downturn

Alternatives,

More Mainstream

SUMMARY

Because of the formerly low-yield environment and the disappointing performance of traditional stocks and bonds in 2022, many large asset owners globally have moved into illiquid alternatives (alts) such as private equity, private credit and infrastructure. Our view is that some asset owners may reconsider their allocation to private markets due to the changing economic environment, portfolio rebalancing relating to the falling valuations in public market assets, and improved funding ratios among pensions.

Separately, institutional investors in the US, UK and elsewhere have turned to liquid alts such as trend-following, macro and commodity funds, as well as to other investment vehicles that can perform better in an uncertain market by employing less-correlated strategies. Private equity, real estate and infrastructure have also attracted inflows because they can deliver higher risk-adjusted returns when locking up capital for longer. There is also renewed but selective interest in hedge funds. Breaking it down…

Hedge Funds to Benefit

Hedge funds are not currently driving the alts trend among large US asset owners. However, a 2022 Pershing Institutional survey of 80 institutional and private wealth investors globally showed 38% of respondents planning to increase or maintain their hedge fund allocations.

Weightings Lifted

Endowments and foundations (E&Fs) are highly invested in alts. As of Q4 2022, they had an average 62% allocation to alts, according to our assets under custody and administration, up from 58% in Q4 2019. Over the past three years, their alts assets have grown (performance changes and allocations) at a compound annual rate of 9%.

Global Endowment & Foundation Alts Allocations

Eyeing Private Equity

Private equity is a focus for US public pension

plans, foundations and endowments. We are seeing some large US asset owners decrease allocations to traditional fixed income and increase their allocations to private equity. Based on the custody activities we conduct for 300 large US asset owners, where we see 100% of their portfolios, the average equal-weighted allocation for February 2023 was 19.5% for private equity and 15.2% for hedge funds. That compares to 17.9% and 15.9% as of end 2021, respectively.

Tipped By Retail Brokers

Net sales of alternative mutual funds and ETFs by retail broker-dealers reached their highest levels in three years last year. In fact, alternatives was the only asset class to see positive mutual fund sales in 2022, according to our Growth Dynamics platform, which tracks MFs, ETFs and separately managed accounts (SMAs). First-quarter activity has been slower due to tax-loss harvesting, but alternative active equity ETFs have seen inflows because they purport to deliver income with less volatility and can be used to hedge against market downturns.

Retail Broker Net Sales by Asset Class

Rethinking 60/40

Our Wealth data show fewer firms trusting the traditional 60/40 portfolio model as a ballast against market turbulence. Our recent annual 10-Year Capital Markets Assumptions highlighted the increasing importance of alternatives within a well-diversified portfolio. In a higher rate and inflationary environment, investments in traditional infrastructure (such as toll roads and utilities) and non-traditional infrastructure (such as cell towers and renewable energy) often have built-in inflation hedges, providing explicit protection. Other real assets such as real estate and natural resources have substantially outperformed 60/40 portfolios in past periods of higher inflation. Private debt is an all-weather strategy that can provide consistent, attractive risk-adjusted returns, in part due to the illiquidity premium. It also tends to be floating rate, making it attractive in a rising rate environment.

Our vantage comes from:

Touching

20%

of the world’s investable assets

Safekeeping

$46.6T

in assets (custody and/or administration) as the world’s largest custodian

Settling

$10T

in US government securities daily

Servicing

$5.5T

in US and international collateral

Processing

$2.5T

of US dollar payments daily

Managing

$1.9T

in assets for our asset & wealth management clients

Financing

$4.5T

in lendable securities

Investing

$280B

in wealth management assets

Data as of March 31st, 2023