Decoding the Full Potential of RQFII

A Greater Gateway Series, Issue 5

Decoding the Full Potential of RQFII

A Greater Gateway Series, Issue 5

August 2018

By Magdalene Tay, John Sin

The Renminbi Qualified Foreign Institutional Investor (RQFII) scheme is one of the five schemes that supports foreign access to China’s capital markets. The challenge then becomes which one to invest through or should it be more than one?

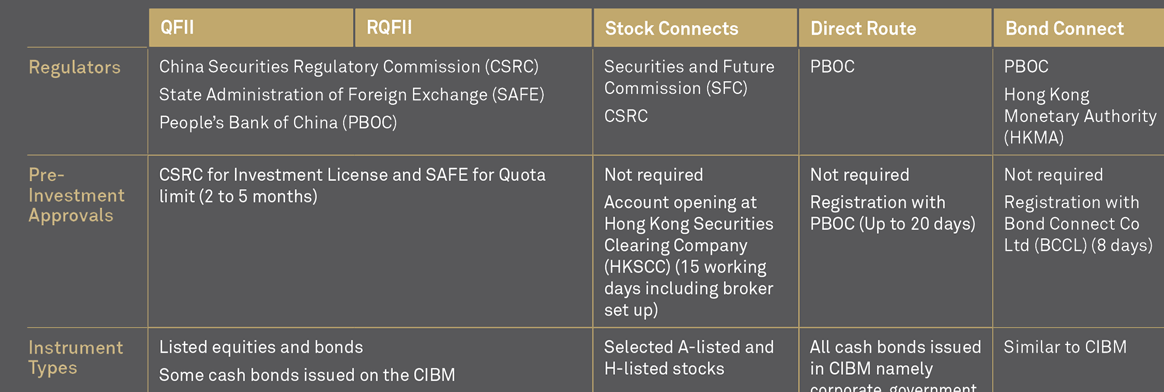

The Renminbi ("RMB") Qualified Foreign Institutional Investor ("RQFII") scheme is one of the current five schemes enabling foreign investors to invest and trade in onshore securities in the People’s Republic of China ("PRC") – the others being the Qualified Foreign Institutional Investor ("QFII") scheme, the Stock Connects (Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect), the Bond Connect, and the China Interbank Bond Market ("CIBM") Direct Access Scheme. (see Figures 1 and 4, which outline the major differences between each of these schemes).

With these five different schemes in existence and the "Exchange-Traded Funds Connect" (or the "ETF Connect") looming, the quandary becomes which one (or more) to choose as an independent investment strategy or in tandem with your current investments through other schemes.

RQFII: Past, Present and Future

Experts from BNY Mellon and K&L Gates examine the past, present and future of the RQFII scheme. They explain the trends and market appetite for RQFII and compare it with the other access schemes.

Figure 1: China Access Schemes At-A-Glance

Key RQFII Scheme Developments

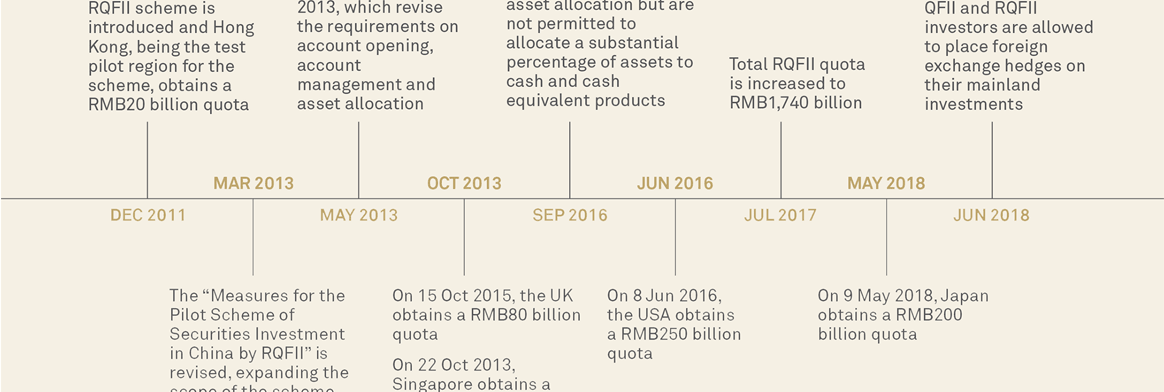

Originally, when introduced in December 2011, the RQFII pilot scheme was intended to be an expansion of the existing QFII scheme, the key difference being that QFII quota-holders had to convert foreign currency into RMB in order to invest directly in PRC securities, whereas RQFII quota-holders could invest directly into PRC domestic capital markets with offshore RMB. As Hong Kong was the test pilot region for the scheme, the initial scheme made a RMB20 billion quota available to Hong Kong subsidiaries of Chinese financial institutions only.

In March 2013, the RQFII rules were revised to, inter alia, (1) remove investment restrictions, giving asset managers more robust discretion to build investment portfolios, (2) permit index futures, and (3) open up the scheme to Hong Kong subsidiaries of Chinese banks (e.g., Chinese insurance companies; Hong Kong-registered financial institutions that have major businesses in the territory; and non-Chinese fund managers with no Chinese shareholders (so long as they operated in Hong Kong)).

In September 2016, the State Administration of Foreign Exchange (“SAFE”) further relaxed the RQFII rules to simplify quota application and control, including simplifying the quota application process, easing the inward and outward remittance, and shortening the lock-up period. Later in the same month, the China Securities Regulatory Commission (“CSRC”) removed asset allocation restrictions on RQFIIs (and QFIIs), providing both with more discretion to determine asset allocation so long as a substantial percentage of those assets were not allocated to cash and cash equivalents.

Throughout the scheme’s existence, the People’s Bank of China (“PBOC”) has expanded the scope of the scheme carefully with the ultimate purpose of enabling foreign institutional investors to apply for RQFII quota and licenses in a measured and controllable manner.

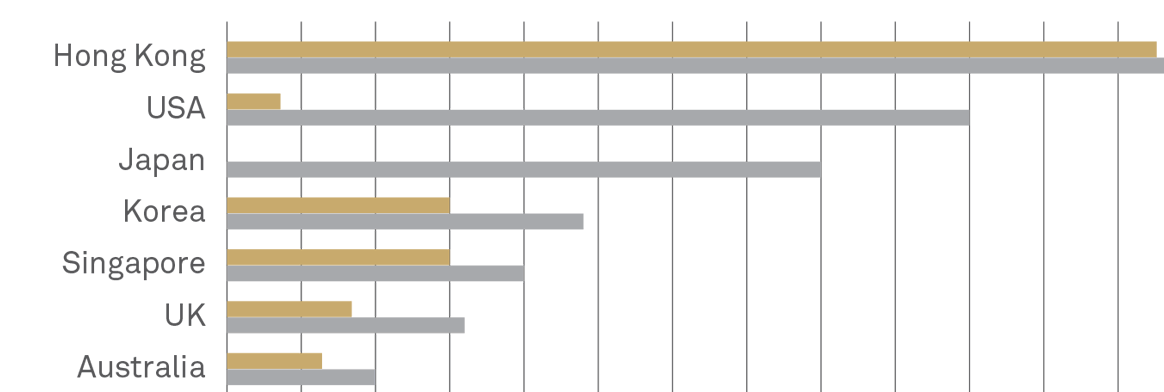

As of June 2018, there are 19 eligible RQFII jurisdictions with RMB1,940 billion (approximately US$286 billion) RQFII quota granted (see Figures 2 and 3).

Figure 2: A Glimpse at the RQFII Landscape

“The RQFII scheme has evolved significantly from market accessibility, regulatory reforms and capital mobility. This may indicate that the Chinese government welcomes foreign direct investment into the domestic market.”

— Magdalene Tay – Custody Product Manager, Asset Servicing, APAC, BNY Mellon

Figure 3: Timeline of Key RQFII Scheme Developments

Prior to the introduction of the Stock Connects, when only the QFII and the RQFII schemes existed, choosing the appropriate scheme was fairly straightforward – you merely had to assess whether you were an institutional investor and whether or not you had available offshore RMB. However, the introduction of the Shanghai-Hong Kong Stock Connect in 2014 and the Shenzhen-Hong Kong Stock Connect in 2016 dramatically changed the investment landscape, as both allowed foreign retail investors, for the first time, to access Chinese stocks listed on the Shanghai and Shenzhen stock exchanges via Hong Kong and trade them on The Stock Exchange of Hong Kong Limited ("HKEX"). Both eliminated the need to deal with specialized service providers, such as custodians, or to ensure sufficiency of offshore RMB, amongst other things.

The next dramatic changes came in 2016 and 2017, when the CIBM Direct Access Scheme and the Bond Connect were opened, which allow foreign investors to access the CIBM directly and via Hong Kong.

While each new development has created much ado, each investment channel has its advantages and limitations.

Is the RQFII Scheme Right For You?

A consideration of whether or not the RQFII scheme works best for you requires an analysis of the limitations of the other PRC direct access schemes, as each has its own quirks which may work for one investor but not another.

Stock Connects

Take the Stock Connects which enable foreign investors to access certain eligible PRC A-shares on the Chinese equity market (“Eligible Stock Connect PRC A-shares”) without any long term commitment. Investing via the Stock Connects require little planning or set up. Assuming you are eligible to open an account to trade on HKEX, you may begin trading immediately once you open such account. However, as an investor under the Stock Connects, you are just one in the mass of the HKEX investors to whom a daily overall trading limit in respect of those limited Eligible Stock Connect PRC A-shares applies and you may buy only those Eligible Stock Connect PRC A-shares and no other A-shares. In the event that the maximum daily trading limit is reached, no further trading is permitted.

“Firms holding RQFII quota can structure products to invest in securities that are not permitted in the Connect schemes, and also to launch RMB-based products to capture the fast growing RMB pool held by investors.”

— John Sin – Head of Greater China, Asset Servicing, BNY Mellon

In comparison, as an RQFII holder, you will be treated, in all other respects, the same as a direct onshore PRC investor. You will only be subject to your individual quota granted by the PRC regulators, without being restricted to Eligible Stock Connect PRC A-shares only or to any daily trading limit, and you will have greater access and exposure to the PRC equity market.

In addition to the overall daily trading limits, also bear in mind that the Stock Connects are "indirect" investment schemes, which only enable investors to have access to Eligible Stock Connect PRC A-shares through the Hong Kong Securities Clearing Company Limited ("HKSCC") as the investor’s nominee to hold those securities.

In short:

- the RQFII scheme has a wider investment scope compared to the Stock Connects;

- investors are able to trade as long as it is a trading day in the PRC whereas under the Stock Connects, investors can only trade on Eligible Stock Connect PRC A-shares when both the Hong Kong and China markets are open for trading; and

- the RQFII scheme is not subject to the overall daily trading limit, which applies to all investors under the Stock Connects.

CIBM Direct Access Scheme/Bond Connect

If your interest is solely in trading bonds and not equities, it would appear that the CIMB Direct Access Scheme or the Bond Connect would be more ideal. However, while the CIBM Direct Access Scheme is wider than the scope of QFII/RQFII insofar as bonds only are concerned, the CIBM Direct Access Scheme only applies to PRC onshore bonds, but not equities. The RQFII scheme allows investments directly in both PRC equities and bonds and, therefore, for an investor that wants to have access to both equities and bonds, the CIBM Direct Access Scheme and Bond Connect would not give them the scope that the RQFII scheme would.

Practical Implications

If you plan to be in the PRC market on a long-term basis, as a QFII/RQFII investor (or direct investor), you may have greater access to PRC regulators than as a nameless, indirect investor through the other schemes, such as the Stock Connects and Bond Connect. The PRC regulators have demonstrated that they can be sensitive and responsive to issues affecting the market. Many revisions to the existing direct investment schemes came about as a result of frequent consultations with direct investors, such as clarifications on capital gains tax issues or even the introduction of the RQFII scheme itself.

With the extension of the RQFII scheme to 18 jurisdictions outside of Hong Kong, licensed entities in those jurisdictions are now eligible to be RQFIIs.¹ Global asset managers with locally-licensed entities in several RQFII jurisdictions can, in fact, hold individual, separate quotas through each jurisdiction, increasing the amount of quota that it can, on a consolidated basis, hold. This is useful if a particular jurisdiction reaches its RQFII quota, such as when Hong Kong ran out of its overall RQFII quota in 2014.

In terms of commercial practicalities, the RQFII scheme, together with its sister QFII scheme, allows maximum scope to invest directly in both PRC shares and bonds (whereas the Stock Connects only permit investment in PRC securities, and the CIBM Direct Access Scheme and Bond Connect only permit investment in PRC bonds). With the rise in ETFs and the impending launch of the ETF Connect later in 2018, there is a double, perhaps even triple, opportunity for an asset manager to take advantage of the PRC direct investment schemes: by being an RQFII holder, launching an ETF fund that utilizes its RQFII quota, listing that ETF on HKEX and then accessing PRC and Hong Kong investors through the ETF Connect.

Figure 4: China Access Schemes in Comparison

Developments on the Horizon

While it is difficult to predict the PRC regulators’ next moves, the industry’s general expectation is that there will be further relaxation in rules for both the RQFII and QFII schemes, bringing both the RQFII and QFII schemes in alignment. Industry participants would also hope for a consolidation of at least some of the PRC direct investment schemes, although this appears unlikely. Given the fact that some of the PRC direct investment schemes were launched well before the other schemes, "switching" from one scheme to another in an attempt to consolidate would require the sell-down of all of the PRC securities held in one scheme and then a completely new buy-in of such PRC securities in the remaining scheme as direct transfer is not possible. With the Shanghai-London Stock Connect expected to roll out this year, the existing Stock Connects and Bond Connect seem to be firmly entrenched while new sweeteners for the RQFII and QFII schemes indicate that the PRC regulators continue to have faith in them.

What Should I Do?

Perhaps the answer to the question of which PRC direct investment scheme to consider really boils down to what kind of investor you are and your purpose or strategy with respect to PRC assets.

If you are a fund manager and/or have access to offshore RMB with a long-term focus on the PRC and an investment strategy that is substantially based on PRC assets, then the RQFII may offer an opportunity for direct investment into PRC onshore securities. Moreover, firms holding RQFII quota can structure products to invest in securities that are not permitted in the Stock Connects or Bond Connect alone, and also to launch RMB-based products to capture the fast growing RMB pool held by investors.

Key Considerations before Applying

If you decide that the RQFII scheme is for you, there are additional strategic issues to consider before applying. The first issue concerns where you should apply for your RQFII license and quota. Sometimes, this may be straightforward, such as if you only have licensed entities in one RQFII jurisdiction. However, if you have several licensed entities in different RQFII jurisdictions, you should consider the total assets you have under management and how much quota you will require in each RQFII jurisdiction. It may also be advantageous to match your desired quota against the available quota in each RQFII jurisdiction of interest.

Other items to consider include the marketability of any funds launched using an RQFII quota, the availability of offshore RMB, the administrative support needed and required during the entry process, account structure and custody, and settlement flows. You may need to mix and match your preferences and the features of the RQFII jurisdictions as desired.

You may also want to consider when a particular jurisdiction was granted RQFII quota to gauge the spectrum of local support and experienced professionals that will likely be available to assist you with setting up and managing your investment. Arguably, Hong Kong, which has the longest history with the RQFII scheme, has the widest spectrum of support in terms of service providers, administrative support, investment advisers and managers, availability of offshore RMB and market demand. Singapore is not far behind. Additionally, London may also be worth considering, as the annual UK-China Economic and Financial Dialogue on Asset Management Sector reflects the PRC’s commitment in establishing London as an offshore RMB center and PRC regulators tend to use this opportunity to test the waters and announce sweeteners.

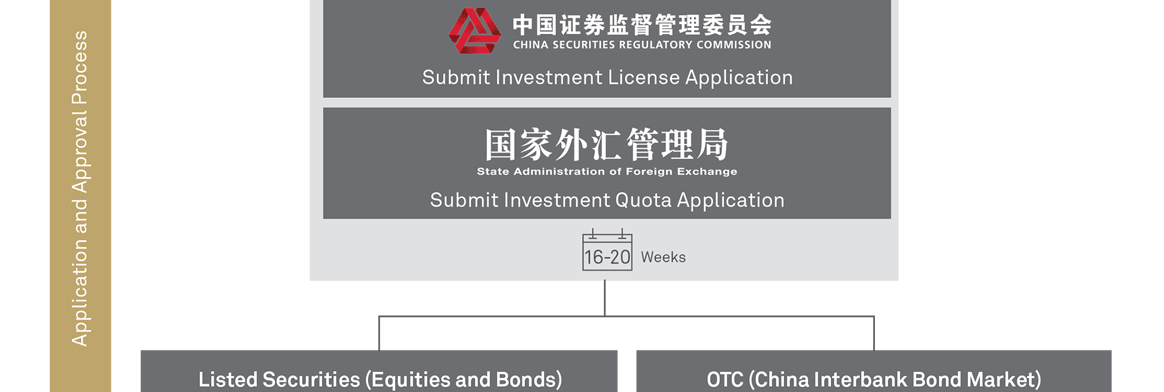

For an overview of the RQFII entry process, please see Figure 5.

Figure 5: RQFII Entry Process

Conclusion

Investors must carefully consider their short and long-term goals when devising PRC investment strategies – your strategy should be driven by your risk appetite and what you want to achieve. One should also be open to the idea of combining different PRC direct access schemes – it is not uncommon for investors to use RQFII as a complementary scheme in conjunction with other access schemes.

Looking at the timeline of how various Chinese government ministries have coordinated their efforts to foster and promote these investment schemes in various jurisdictions suggests that China is carefully creating a network of hubs within Asia and Europe that can prosper along with the spread of its currency. Carefully reviewing and revising your PRC investment portfolio to optimize your asset allocation on a regular basis should ensure you are utilizing the best scheme or combination of schemes. It should also enable you to remain nimble, adaptable and in an optimal position when the PRC regulators announce their next moves.

1 Apart from Hong Kong, the current jurisdictions include Singapore, the United Kingdom, France, South Korea, Germany, Australia, Switzerland, Canada, the United States, Luxembourg, Thailand, Malaysia, Qatar, United Arab Emirates, Hungary, Chile, Ireland and Japan.

BNY Mellon is the corporate brand of The Bank of New York Mellon Corporation and may be used as a generic term to reference the corporation as a whole and/ or its various subsidiaries generally. This material and any products and services may be issued or provided under various brand names in various countries by duly authorised and regulated subsidiaries, affiliates, and joint ventures of BNY Mellon, which may include any of the following. The Bank of New York Mellon, at 225 Liberty St, NY, NY 10286 USA, a banking corporation organised pursuant to the laws of the State of New York, and operating in England through its branch at One Canada Square, London E14 5AL, registered in England and Wales with numbers FC005522 and BR000818. The Bank of New York Mellon is supervised and regulated by the New York State Department of Financial Services and the US Federal Reserve and authorised by the Prudential Regulation Authority. The Bank of New York Mellon, London Branch is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request. The Bank of New York Mellon SA/NV, a Belgian public limited liability company, with company number 0806.743.159, whose registered office is at 46 Rue Montoyerstraat, B-1000 Brussels, authorised and regulated as a significant credit institution by the European Central Bank (ECB), under the prudential supervision of the National Bank of Belgium (NBB) and under the supervision of the Belgian Financial Services and Markets Authority (FSMA) for conduct of business rules, a subsidiary of The Bank of New York Mellon, and operating in England through its branch at 160 Queen Victoria Street, London EC4V 4LA, registered in England and Wales with numbers FC029379 and BR014361. The Bank of New York Mellon SA/NV (London Branch) is authorised by the ECB and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our regulation by the Financial Conduct Authority and Prudential Regulation Authority are available from us on request. The Bank of New York Mellon SA/NV, operating in Ireland through its branch at Riverside 2, Sir John Rogerson’s Quay, Grand Canal Dock, Dublin 2, D02 KV60, Ireland, trading as The Bank of New York Mellon SA/NV, Dublin Branch, which is authorized by the ECB, regulated by the Central Bank of Ireland for conduct of business rules and registered with the Companies Registration Office in Ireland No. 907126 & with VAT No. IE 9578054E. If this material is distributed in or from, the Dubai International Financial Centre (DIFC), it is communicated by The Bank of New York Mellon, DIFC Branch (the ‘DIFC Branch’) on behalf of BNY Mellon (as defined above). This material is intended for Professional Clients and Market Counterparties only and no other person should act upon it. The DIFC Branch is regulated by the DFSA and is located at DIFC, The Exchange Building 5 North, Level 6, Room 601, P.O. Box 506723, Dubai, U.A.E. BNY Mellon also includes The Bank of New York Mellon which has various subsidiaries, affiliates, branches and representative offices in the Asia-Pacific Region which are subject to regulation by the relevant local regulator in that jurisdiction. Details about the extent of our regulation and applicable regulators in the Asia-Pacific Region are available from us on request. Not all products and services are offered in all countries.

The material contained in this document, which may be considered advertising, is for general information and reference purposes only and is not intended to provide legal, tax, accounting, investment, financial or other professional advice on any matter, and is not to be used as such. The contents may not be comprehensive or up-to-date, and BNY Mellon will not be responsible for updating any information contained within this document. If distributed in the UK or EMEA, this document is a financial promotion. This document and the statements contained herein, are not an offer or solicitation to buy or sell any products (including financial products) or services or to participate in any particular strategy mentioned and should not be construed as such. This document is not intended for distribution to, or use by, any person or entity in any jurisdiction or country in which such distribution or use would be contrary to local law or regulation. Similarly, this document may not be distributed or used for the purpose of offers or solicitations in any jurisdiction or in any circumstances in which such offers or solicitations are unlawful or not authorised, or where there would be, by virtue of such distribution, new or additional registration requirements. Persons into whose possession this document comes are required to inform themselves about and to observe any restrictions that apply to the distribution of this document in their jurisdiction. The information contained in this document is for use by wholesale clients only and is not to be relied upon by retail clients. Trademarks, service marks and logos belong to their respective owners.

Pershing LLC, member FINRA, NYSE, SIPC, is a wholly owned subsidiary of The Bank of New York Mellon Corporation (BNY Mellon). Trademark(s) belong to their respective owners. For professional use only. Not intended for use by the general public.

© 2018 The Bank of New York Mellon Corporation. All rights reserved.