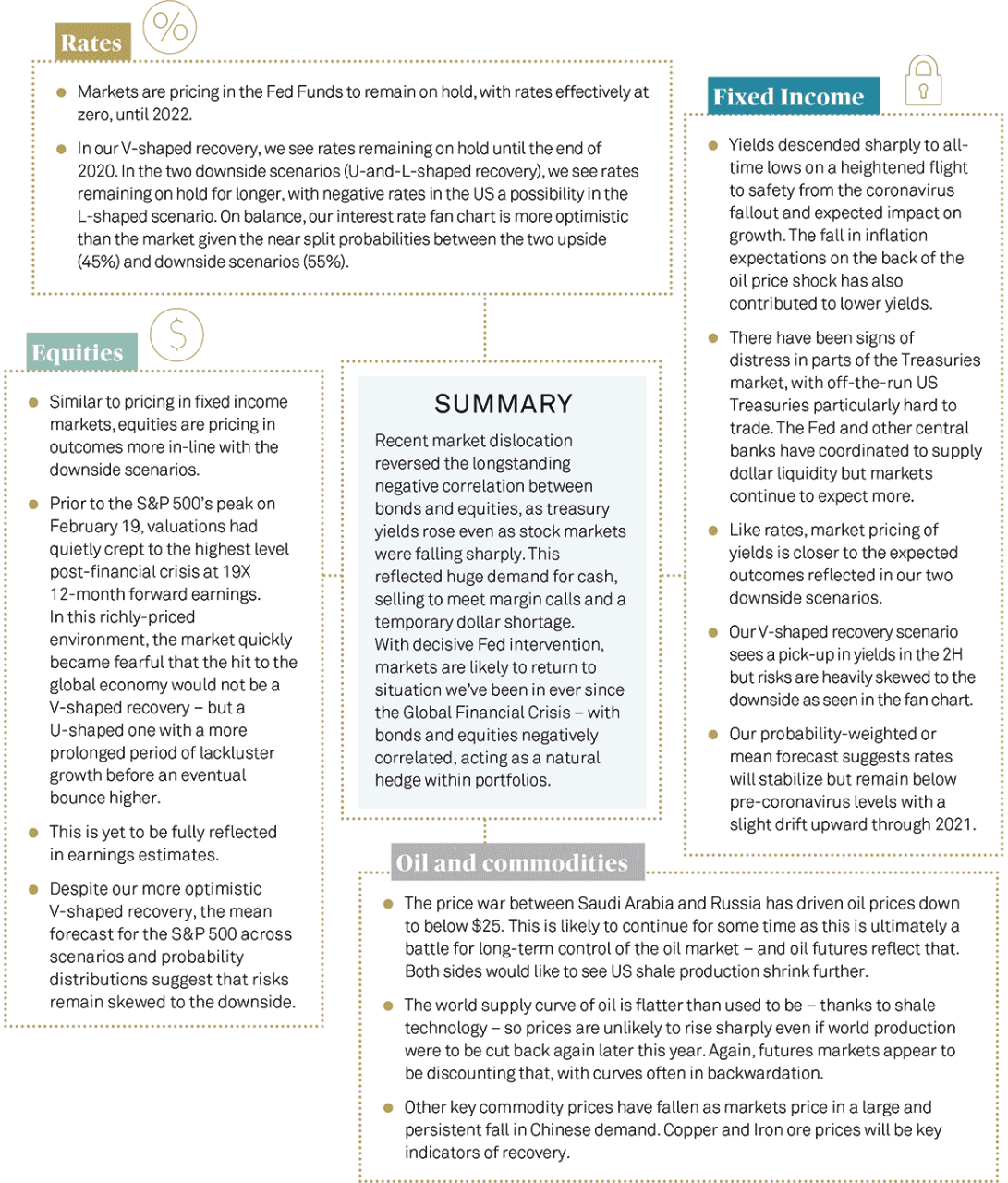

Vantage Point: Pandemic

Quarterly Outlook Q2.2020

Vantage Point: Pandemic

Quarterly Outlook Q2.2020

March 31, 2020

By Shamik Dhar, Alicia Levine, Liz Young, Lale Akoner, Bryan Besecker, Sebastian Vismara

Since our last publication, the world has seen the emergence of a novel coronavirus that has infected large numbers of people in China and the rest of the world.

Of course, this is first and foremost a human tragedy and, at the time of writing, it’s very difficult to judge how widely the disease will spread. That said, it is having and will continue to have a large economic impact and much of this edition is devoted to trying to work out what that might be. As regular readers will know, we don’t deal in point forecasts – and a shock like the emergence of the coronavirus highlights the strength of the scenario-based, probabilistic approach we take. By mapping plausible scenarios, probability-weighting them and generating summary fan charts for key asset prices, we can draw broad investment conclusions that we think take account of the full distribution of likely outcomes.

The coronavirus appears to be more infectious but less deadly than some other diseases, such as SARS or MERS. That means the main economic impact is likely to be felt through the measures taken to contain it – for instance, travel restrictions, reduced working time and, in extremis, quarantine. A number of countries have already gone into effective lockdown, including the US and much of Europe and this will have a dramatic impact on GDP in the first half of the year and possibly beyond. Already, a global recession in 2020 looks more likely than not.

In economic terms it is both a supply shock and a demand shock. It cuts supply because working hours fall and supply chains are disrupted; and it hits demand because people can’t go out shopping, buy services face-to-face, or go on holiday. Markets have reacted with shock – as of March 23 the S&P 500 is down 34% from peak – already the 5th largest post-war recessionary drop, in a fraction of the time it took the others to get there. Central banks fear the demand shock more and the Fed has led the way with rate cuts and a relaunch of QE. Financial market stresses have appeared and central banks have coordinated to supply the overwhelming demand for cash and dollars. Longer term, the situation could get more complicated should the substantial hit to global supply push up global costs and prices, especially if that impact endures because the spread of the disease causes de-globalization to accelerate.

Our scenarios explore these and other issues in depth. There are a couple of ‘upside’ V-shaped scenarios, but there are also two downside ‘U’ and ‘L’-shaped ones. In each case we go through the economic mechanisms in some detail and end up with some very distinctive economic and market outcomes. In the end though, this is a hugely uncertain situation and I encourage readers to use the scenarios to test their own assumptions, whether that’s ‘time to buy’ or ‘it’s Armageddon out there’, or anything in between. Our own broad investment conclusion, based on the return and risk expectations embodied in our fan charts, is that a more risk-averse stance may be prudent until we have more clarity. The potential for a strong bounce back exists no doubt but, it’s not clear from our analysis that the expected gain in the best scenario outweighs the expected losses in the worst.

As ever, we hope you enjoy reading the document and look forward to your feedback.

Shamik Dhar

Chief Economist

BNY Mellon Investment Management

Executive Summary

What We Think - Economic Scenarios

SCENARIO: V-shaped recovery; coronavirus spreads but economic impact contained

35% PROBABILITY

Disease peaks during the summer. Central bank liquidity provision is large enough to prevent severe dislocation in financial markets and the Fed in particular supplies enough dollars to overcome the dollar shortage and satisfy the global demand for cash. Large fall in Chinese GDP in China in H1 (-10% or so), followed by a strong recovery during H2 2020 as inventories are rebuilt and services production/ consumption resumes. The impact on Europe and the US lasts longer, with similarly large hit to GDP, but global growth picks up gradually during H2 2020. Output recovers everywhere so that, by the first half of 2021, it is more or less where it would have been had the disease never emerged, so there is no permanent loss to output (hence the V-shape recovery). Global monetary and fiscal policy remains loose. Other central banks may revert to unorthodox policy measures and closer coordination with fiscal authorities. Global inflation remains subdued and interest rates remain low. Risk assets bounce back in Q2, ahead of the economic recovery as investors learn that the long-term macro consequences of the disease will be limited.

SCENARIO: U-shaped recovery; financial market shake-out

35% PROBABILITY

Coronavirus spread more persistent and widespread than V-shaped recovery but not as severe as the L-shaped recovery. Nevertheless, this is the trigger for widespread risk-off sentiment in the face of heightened uncertainty. Risk premia rise sharply, equity and credit prices fall – particularly in highly leveraged corporates. Sell-off exacerbated by a huge tightening of financial conditions as credit vulnerabilities are exposed in the US. Non-China EMs suffer from China exposure and a withdrawal of liquidity and are limited in their policy tool-kit to stem the outflows. A further dramatic flight to safety ultimately brings government bond yields to previously unthinkable lows and even further into negative territory for certain regions. But preceding that, huge demand for cash causes some yields to rise temporarily leading to severe market dislocation as liquidity squeeze and dollar shortage worsens. Unlike the L-shaped recovery, this is primarily a hit to global aggregate demand (rather than supply). Spill-over effects, such as in energy prices, surface making the situation worse. Global policy makers unable to put a floor on deteriorating sentiment in the short-term. Sell-off triggers a slowdown not unlike that seen after the tech bust of 2000-1 followed by a U-shaped recovery.

SCENARIO: L-shaped recovery; globalization flatlines

20% PROBABILITY

As contagion spreads outside China, developed countries are overwhelmed by the epidemic and economic activity in affected regions falls to a trickle. With hits to demand and supply, the impact on Chinese GDP is massive--close to 18%--over the course of 2020, mostly in the first half of the year. Europe and the US see similar-sized GDP losses during the rest of 2020. Ultimately, this adds pressure on firms to diversify supply chains over the longer term, accelerating underlying de-globalization trends. The impact on global GDP is large, mostly felt through the supply side. Global costs rise as businesses struggle to find alternatives to Chinese production. US, EU and China respond with protectionist moves, especially if China attempts to devalue the Yuan, further exacerbating the supply shock. Central banks can accommodate to some degree, but there is only so much monetary policy can do in the face of a negative supply shock. Fiscal policy is loosened globally, but insufficiently to offset global retrenchment and many businesses go bust. Asset prices fall despite loose monetary policy stance, since policy is still tighter than previously expected and confidence is hit hard by duration and spread of disease. In the longer term, the liberal international trading/investment order is truly dead and a new narrative takes hold: the virus has accelerated an underlying trend in which re-shoring and nationalism means higher costs and lower growth for years (whether true or not). Risk markets sell off big time, equities enter a prolonged bear market, and global yields dive further into negative territory.

SCENARIO: US-led inflation returns

10% PROBABILITY

Growth fears are overdone in the US as the coronavirus is contained. The economy remains resilient, resumes its upward trajectory prior to the coronavirus, and activity rebounds sharply in 2H as rest of world weakness lingers. Ultimately, the US economy is more resource constrained than anticipated. Inflation rises more than expected and breaches the Fed’s 2% target in early 2021. Inflation expectations quickly and sharply adjust higher, forcing the Fed to tighten as China/others are weakening. Higher rates and dollar prompt capital flight from risky assets, particularly in emerging markets. Financial instability and dollar shortage ensues yet the main transmission mechanism is international financial markets. Replay of 2015-2016 but bigger.

Capital Market Pricing - What the Markets Think

Investment Conclusions

Equities

We expect uncertainty surrounding the duration and magnitude of the coronavirus to continue to generate volatility in global equity markets until the spread of the virus slows.

With the hit to earnings well underway, proper modeling remains ephemeral. We suggest sitting tight until some evidence of earnings stability is established. We urge investors to remain cautious before looking to take advantage of lower prices as we believe further negative news is likely and do not expect an imminent and decisive recovery in prices.

International and EM equity markets are increasingly fragile due to shocks from the virus and oil prices, and selective exposure is suggested. Although we continue to view them as attractive long-term investments, price fragility remains high until some degree of positive news is received.

Fixed Income

Emergency actions by the Federal Reserve should help stabilize liquidity in the Treasury market and allow yields to find firmer footing. Expect a steepening of the yield curve as a result of policy movement and for the correlation between stocks/bonds to return to a low or negative level.

Even in the case of a V-shaped recovery beginning in the 2H, volatility is likely to remain elevated and high-quality fixed income offers a much-needed buffer.

There is concern over the liquidity and resilience of high yield and leveraged loans and we view them as vulnerable asset classes in this environment. As such, we suggest reduced exposure to liquid instruments in these areas to minimize daily price swings that can induce further fear.

US Dollar

We expect the USD to appreciate as uncertainty regarding the depth and length of the shock, and the associated financial market volatility, drives flows into US safe assets.

The increase in demand for US Dollar cash from international investors, as seen by the widening in the USD cross currency basis, also provides support to the currency.

As US rates converge closer to rate levels in the rest of the world, the appreciation may be somewhat limited. However we do not believe the narrowing of interest rate differentials to be sufficient to drive broad USD weakness.

Alternatives

Risk mitigation via liquid alternative strategies such as absolute return, market neutral and other hedging approaches can provide investors with enhanced bear market protection in these extreme environments.

Investors holding private or locked-up alternative investments are shielded from daily market swings and panic selling by the sheer nature of illiquid investments.

IMPORTANT INFORMATION

This material should not be considered as investment advice or a recommendation of any investment manager or account arrangement. Any statements and opinions expressed are those of the authors stated, as at the date of publication, are subject to change as economic and market conditions dictate, and do not necessarily represent the views of BNY Mellon or any of its affiliates. The information has been provided as a general market commentary only and does not constitute legal, tax, accounting, other professional counsel or investment advice, is not predictive of future performance and should not be construed as an offer to sell or a solicitation to buy any security or make an offer where otherwise unlawful.

The information has been provided without taking into account the investment objective, financial situation or needs of any particular person. Please consult a legal, tax or investment advisor in order to determine whether an investment product or service is appropriate for a particular situation. BNY Mellon and its affiliates are not responsible for any subsequent investment advice given based on the information supplied. This is not investment research or a research recommendation for regulatory purposes as it does not constitute substantive research or analysis. To the extent that these materials contain statements about future performance, such statements are forward looking and are subject to a number of risks and uncertainties. Information and opinions presented have been obtained or derived from sources which BNY Mellon believed to be reliable, but BNY Mellon makes no representation to its accuracy and completeness. BNY Mellon accepts no liability for loss arising from use of this material.

BNY Mellon Investment Management is one of the world’s leading investment management organizations and one of the top US wealth managers, encompassing BNY Mellon’s affiliated investment management firms, wealth management organization and global distribution companies. BNY Mellon is the corporate brand of The Bank of New York Mellon Corporation and may also be used as a generic term to reference the Corporation as a whole or its various subsidiaries generally.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. All information contained herein is proprietary and is protected under copyright law.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE |

BNY Mellon Investment Adviser, Inc, and BNY Mellon Securities Corporation are subsidiaries of BNY Mellon. ©2020 BNY Mellon Securities Corporation, distributor, 240 Greenwich St., New York, NY 10286.