The Rise of Tokenization

How tokenization can revolutionize finance and its barriers to adoption

The Rise of Tokenization

How tokenization can revolutionize finance and its barriers to adoption

September 2022

By Kai Ren and Zakie Twainy

Tokenization has the power to revolutionize the financial landscape‒intrinsically changing how investments are managed, used and monetized. The process of tokenization facilitates the creation of a multitude of new financial products, allowing every person and organization in the world to diversify their portfolio of investments on a global scale, regardless of income or size.

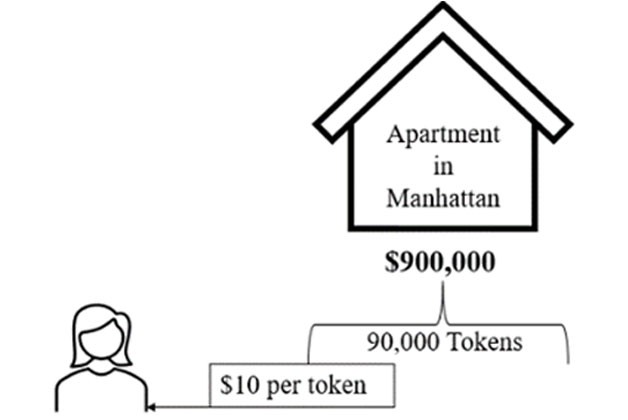

Let’s look at an example scenario that highlights the power of tokenization. A middle-class woman named Ms. Ganbold in Ulaanbaatar, Mongolia, makes the average income in the city, which is approximately $400 USD1 per month, and she would like to invest in Manhattan real estate, where prices nearly doubled in the 2010s.2

With traditional financial products, this would be extremely challenging considering the usual initial capital investment, if not a near impossibility. However, with tokenization, fractionalization—the division of an asset class into portions that are smaller than the whole3—opens the door of opportunity for Ms. Ganbold.

Tokenization of assets involves the process of digitally representing real, physical assets on distributed ledgers, or issuing traditional asset classes in tokenised form.4 Within the context of blockchain technology, tokenization is the process of converting something of value into a digital token that’s usable on a blockchain application and a token represents a share of ownership in the underlying asset. This process can work for tangible assets like gold, real estate, debt, bonds, and art, or certain forms of intangible assets such as ownership rights or content licensing.5 What is even more exciting is that tokenization allows for transforming ownerships such that traditionally indivisible assets can be fractionalized into token forms.6

The owner tokenizes his apartment at a value of $900,000, into a total of 90,000 tokens, with each token amounting to almost 0.001% of the apartment’s value. In addition, with a contract, he ensures selling the apartment within 10 years or when the market value is at least 50% higher, whichever comes first.7 With each token at $10 USD, investing in Manhattan real estate now becomes a possibility for Mrs. Ganbold, despite her level of income. Unlike traditional ownership rights, the apartment tokens would be just an investment, and she would not be able to use or live in the apartment.

Why It Matters

Tokenization’s importance stretches far beyond investment access; it could also facilitate new investing models. Currently, most investments leverage shareholder capitalism, striving to optimize profits and share price.8 For example, when you buy a company’s stock, you provide money in exchange for a share, but how the company is run and governed is largely outside of your direct control. Since tokenization leverages smart contracts, it could manage both the financial investment as well as facilitate the voting and/or ownership rights associated with the investment. There is a possibility of incorporating a stakeholder capitalism model,9 a popular management theory in the 1950s and ‘60s that promoted benefits provided to the wider community, not just shareholders.10

With tokenization, is it possible to invest in a company but insist that the CEO be paid no more than 100x the median employee compensation or you automatically reclaim your original investment? (Currently, in the United States, the average is 274x that of the median employee.11) Or could one invest in cutting-edge technology—computer vision, for example —and make the investment contingent on the fact that the owner could never sell the intellectual property to a company in the defense industry?

Beyond this, with tokenization, the transactions of digitally native assets are stored and listed on a digital ledger on a blockchain network giving one golden standard of truth across the globe. Further, the process of leveraging smart contracts permanently records transactions and makes them immutable and instantly executed.12 This not only provides speed in transactions, but also reduces administrative work as there are fewer intermediaries, lowering costs.13

Barriers to Adoption

While tokenization provides a wealth of opportunities to transform the marketplace, there are challenges.

First, there is an absence of consistent regulation across the spectrum of tokenization. In order to achieve wider adoption, there would need to be a global taxonomy (i.e., definition of token); stronger legal framework; regulatory framework (i.e., roles and procedures in digital asset value chain), and supervisory framework (i.e., developing consistent regulatory frameworks, as well as who should supervise and how.) These challenges combined with the borderless nature of blockchain, create challenges for the widescale adoption of tokenization.

Secondly, there are barriers to production grade solutions and scale. The value of tokenization is driven by a network effect—the utility of the technology increases for a user, the more it scales and is adopted. However, incentives do not currently exist to create a network effect.14 This creates a lack of synchronicity among large market players, resulting in fragmented markets that reduce liquidity. While consortia have attempted to solve this problem, they have run into execution challenges, such as IP ownership, and in some cases limited benefit for large players to give access to smaller fintechs and other emerging technology companies in the market.

Beyond this, there are issues with security; blockchain applications have encountered cyber security issues and attacks. Also, the technologies to create, manage and secure tokenization are relatively nascent. Hence there is a need for infrastructure to bridge tokenization easily with legacy systems to ensure a smooth onboarding and management of the assets.15

Burgeoning New Tokenization Projects

Despite all the challenges, several tokenization projects have been launching globally in different industries, advancing the wider ecosystem, such as:

- Commodities + Metals: The Spanish bank, Santander, recently launched loans in Argentina collateralized with tokenized commodities, called Agrotokens. They expect that over the next six months, 1,000 Argentine farmers will receive Santander credits collateralized with tokens based on soybeans (SOYA), corn (CORA) and wheat (WHEA) launched by Agrotoken.16 The tokens allow farmers to more efficiently use grain as collateral and makes the trading of grain more efficient.17

- Art + Collectibles: Tokenization could allow the average investor to invest in blue-chip art. For example, last year the Zurich-based crypto bank, Sygnum, moved the legal ownership rights of Picasso’s 1964 masterpiece Fillette au béret onto the blockchain. It distributed the digital asset into 4,000 tokens, which were sold to more than 50 investors at 1,000 Swiss francs ($1,040 USD) apiece. In doing so, Sygnum gave birth to a new genre of investments dubbed Art Security Tokens (ASTs)18 This allows new investors into high-end art investments.

- Intellectual Property: This past May, the Nigerian government signed a 3-year exclusive intellectual property right agreement with Developing Africa Group to launch a nation-wide wallet which will enable the international commercialization of intellectual property developed and registered within the country. IP that could be tokenized and included on the platform include trademarks, patents and all forms of copyrights such as songs, lyrics, videos, shows, lectures, podcasts and all forms of streamable content.19 The potential for commercialization of IP rights may further encourage Nigerians to discover and create new art, incentivized by economic advancement.20

- Sports teams and athlete contracts: Basketball point guard, Spencer Dinwiddie fought the National Basketball Association over his plan to tokenize his $34 million contract. NBA contracts ban players from transferring rights to their income, so he restructured the offering as a bond backed by business assets.21 In Brazil, Vasco da Gama, one of the leading teams in football, announced it will tokenize the solidarity mechanism. The FIFA Solidarity Mechanism is a part of the FIFA Transfer Regulation, which acts as a selling right for a player and encourages clubs to develop young players. Up to 5% of the total value of each international transfer of an athlete can be shared with all the clubs that an athlete went through during his career until he was 23 years old.

Spencer Dinwiddie (All-Pro Reels, CC BY-SA 2.0, via Wikimedia Commons)

Holders of the tokens will be entitled to a percentage of the sale value of any player to the athlete's forming club.22 These examples illustrate how tokenization could help financially support athletes throughout their career journeys.

- Carbon Credits: A carbon-credit start-up, Flowcarbon, co-founded by WeWork founder, Adam Neumann, recently raised $70 million from venture capitalists a16z, General Catalyst, Samsung Venture Investment and other backers. The company’s goal is to accelerate decarbonization through the tokenization of carbon credits and maintaining a record of the transactions on the blockchain.23

Benefits

In review, tokenization could provide:

- Greater accessibility from fractionalization, faster settlement which creates more liquidity and the ability to use collateral across different time zones.

- Faster settlements for quicker asset turnover and, as a result, higher liquidity. This could help financial institutions move from the current T+2 standard to a near real-time settlement. Assets can be traded, settled, and used as a collateral on the same day‒significantly increasing the velocity on money that leads to wide range of economic benefits.

- Higher efficiency due to simplification and replacement of traditional financial roles with smart contracts. This in turn could provide lower costs for investors and issuers.

- Mobility of assets; any asset can move almost instantly on the blockchain as compared to traditional financial infrastructure (e.g., think ACH rails for cash payments).

Conclusion

While tokenization offers a myriad of possibilities, there is still much work to be done in terms of consistent global regulation and development of the production grade solutions necessary to widen adoption. As investment in tokenization technologies continues to increase and the benefits of new assets becomes more evident, financial institutions should begin thinking about what infrastructure is needed to support tokenization, e.g., onboarding, management and integration with legacy systems, in order to be part of finance of the future.

- https://checkinprice.com/average-minimum-salary-in-ulaanbaatar-mongolia/

- Andrews, Jeff. “NYC Home Prices Nearly Doubled in the 2010s. What Do the 2020s Hold?” Curbed NY, Curbed NY, 13 Dec. 2019, https://ny.curbed.com/2019/12/13/21009872/nyc-home-value-2010s-manhattan-apartments.

- https://capbridge.sg/bond-fractionalization-what-is-it-and-how-we-did-it/

- OECD (2021), Regulatory Approaches to the Tokenisation of Assets, OECD Blockchain Policy Series,

- “What Is tokenization? Blockchain Token Types.” Gemini, Aug. 2021, https://www.gemini.com/cryptopedia/what-is-tokenization-definition-crypto-token#section-security-tokens-utility-tokens-and-cryptocurrencies

- Abrol, Ayushi. “What Is tokenization? A Complete Guide.” Web3.0 & Blockchain Certifications, Blockchain Council, 15 Mar. 2022, https://www.blockchain-council.org/blockchain/what-is-tokenization/

- Mkrtchyan, Christina. “tokenization of Real Estate: Revolutionizing Real Estate through Digitalization and Reduced Market Barriers.” Business Law Digest, USC Gould, 29 Dec. 2021, https://lawforbusiness.usc.edu/tokenization-of-real-estate-revolutionizing-real-estate-through-digitalization-

- https://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/putting-stakeholder-capitalism-into-practice#:~:text='Stakeholder%20capitalism'%20is%20the%20buzzword,and%20a%20high%20stock%20price.

- “Perspectives: The Intersection of Digital Assets and ESG.” BNY Mellon Perspectives, BNY Mellon, Sept. 2021, https://www.bnymellon.com/content/dam/bnymellon/documents/pdf/perspectives/the-intersection-of-digital-assets-and-esg.pdf

- Sundheim, Doug, and Kate Starr. “Making Stakeholder Capitalism a Reality.” Harvard Business Review, Harvard Business Review, 31 Aug. 2021, https://hbr.org/2020/01/making-stakeholder-capitalism-a-reality.

- Eavis, Peter. “Meager Rewards for Workers, Exceptionally Rich Pay for C.e.o.s.” The New York Times, The New York Times, 11 June 2021, https://www.nytimes.com/2021/06/11/business/ceo-pay-compensation-stock.html

- https://corpgov.law.harvard.edu/2018/05/26/an-introduction-to-smart-contracts-and-their-potential-and-inherent-limitations/

- https://lawforbusiness.usc.edu/tokenization-of-real-estate-revolutionizing-real-estate-through-digitalization-and-reduced-market-barriers/and-reduced-market-barriers/.

- https://online.hbs.edu/blog/post/what-are-network-effects

- https://www.blockchain-council.org/blockchain/asset-tokenization/

- Engler, Andrés. “Santander Launches Loans Backed by Tokenized Commodities Such as Soy and Corn.” CoinDesk Latest Headlines RSS, CoinDesk, 7 Mar. 2022, https://www.coindesk.com/business/2022/03/07/santander-launches-loans-backed-by-tokenized-commodities-such-as-soy-and-corn/.

- https://agrotoken.io/en/

- Rivers, Martin Leo. “The Art of tokenization: How a Picasso Painted Itself onto the Blockchain.” Forbes, Forbes Magazine, 30 Apr. 2022, https://www.forbes.com/sites/martinrivers/2022/04/27/the-art-of-tokenization-how-a-picasso-painted-itself-onto-the-blockchain/?sh=6891fb0d7729

- Algorand. “Nigeria to Launch Major Crypto Initiative, IP Exchange Marketplace and Wallet, on Algorand in Partnership with Developing Africa Group and Koibanx.” Nigeria to Launch Major Crypto Initiative, IP Exchange Marketplace and Wallet, on Algorand in Partnership with Developing Africa Group and Koibanx, 23 May 2022, https://www.prnewswire.com/in/news-releases/nigeria-to-launch-major-crypto-initiative-ip-exchange-marketplace-and-wallet-on-algorand-in-partnership-with-developing-africa-group-and-koibanx-884861060.html

- https://thenationonlineng.net/why-nigeria-urgently-needs-an-intellectual-property-ip-policy/

- Nelson, Danny. “NBA Player Spencer Dinwiddie's Token Sale Hits 10% of $13.5M Goal.” CoinDesk Latest Headlines RSS, CoinDesk, 22 July 2020, https://www.coindesk.com/markets/2020/07/22/nba-player-spencer-dinwiddies-token-sale-hits-10-of-135m-goal/.

- Gusson, Cassio. “Leading Brazilian Soccer Team to Tokenize FIFA Player Transfer Fees.” Cointelegraph, Cointelegraph, 5 Nov. 2020, https://cointelegraph.com/news/leading-brazilian-soccer-team-to-tokenize-fifa-player-transfer-fees.

- Ramaswamy, Anita. “Adam Neumann's Blockchain-Based Redemption Story Now Sponsored by A16Z.” TechCrunch, TechCrunch, 25 May 2022, https://techcrunch.com/2022/05/24/flowcarbon-wework-adam-neumann-blockchain-crypto-carbon-credit-startup-raises-funding-from-a16z/.

BNY Mellon is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally. This material does not constitute a recommendation by BNY Mellon of any kind. The information herein is not intended to provide tax, legal, investment, accounting, financial or other professional advice on any matter, and should not be used or relied upon as such. The views expressed within this material are those of the contributors and not necessarily those of BNY Mellon. BNY Mellon has not independently verified the information contained in this material and makes no representation as to the accuracy, completeness, timeliness, merchantability or fitness for a specific purpose of the information provided in this material. BNY Mellon assumes no direct or consequential liability for any errors in or reliance upon this material. BNY Mellon will not be responsible for updating any information contained within this material and opinions and information contained herein are subject to change without notice.

BNY Mellon assumes no direct or consequential liability for any errors in or reliance upon this material. This material may not be reproduced or disseminated in any form without the prior written permission of BNY Mellon. Trademarks, logos and other intellectual property marks belong to their respective owners.

© 2022 The Bank of New York Mellon Corporation. All rights reserved.