What Comes Next for "Meme" Stocks

What Comes Next for “Meme” Stocks

April 2021

By Peter Madigan

Retail investors have been moving markets, thanks to pandemic-related day trading and commission-free execution. Despite a recent pullback, experts say there is no end in sight.

When millions of individual stock pickers took on Wall Street— leading transaction volumes to surge in January—some didn’t see it coming. Now that the new generation of traders is driving so much of today’s equity flows, established industry players are asking what their participation means over the long haul.

The galvanization of these “retail” investors has captured the market zeitgeist in recent months, as huge volumes of trades were effectively crowdsourced from social media chat rooms. Their activity has prompted eye-popping moves across dozens of low-priced stocks that were either thinly traded or virtually moribund.

Fueling the behavior are discount brokerages now offering commission-free trading; technology that is making it easier to transact from anywhere on a mobile phone; and a pandemic that has caused a spike in day-trading. Some have seen huge windfalls; others crushing losses. Several investors in both camps have been reluctant to cash out.

Moreover, the retail participation is much broader than initially reported, according to market participants. The activity has already targeted dozens of stocks across multiple sectors. It involves large numbers of retail investors who have opened zero-commission brokerage accounts. And the activity has been underway far longer than many might suspect.

First-quarter trading volumes would have been the most compelling story for stocks in a generation, had it not been for last spring, when U.S. equities plunged from all-time highs into bear market territory in just 15 trading sessions due to the panic surrounding the COVID-19 pandemic.

Instead, cult-like trading among an expanded set of retail investors is a sign that equity markets are changing rapidly, and that perhaps the shift will be permanent. At the same time, brokers, exchanges and regulators are trying to determine what to make of the phenomenon and how to tamp down on any concerning, speculative activity that might exacerbate the price swings.

Multi-Player Mode

Much of the heightened activity has been attributed to so-called “meme” stock trading, when retail investors surge into popular low-priced equities, in many cases after seeing fundamental analysis posted online.

The poster child for this trend is, of course, U.S. video game retailer GameStop (GME), which began to be promoted as an undervalued security in mid-2020 on Reddit’s WallStreetBets discussion board. GameStop’s price climbed steadily through late 2020 before exploding to $347 a share on January 27, an 8,575% increase on the stock’s $4 valuation six months earlier. By late March, it traded around $181 and remains volatile at the time of writing.

The noteworthy aspect of this is not GameStop, or AMC Entertainment, Nokia, BlackBerry or any other hyped-up name, however. It is what the phenomenon tells investing professionals and regulators about the changing makeup of equity markets, namely that retail investors can move markets.

These investors are a mix of first timers with new accounts, and individual “mom and pop” investors who have been trading more actively during the pandemic while working from home, in many cases armed with stimulus checks. Some 15% of retail investors trading today started only last year, according to a recent Charles Schwab survey.

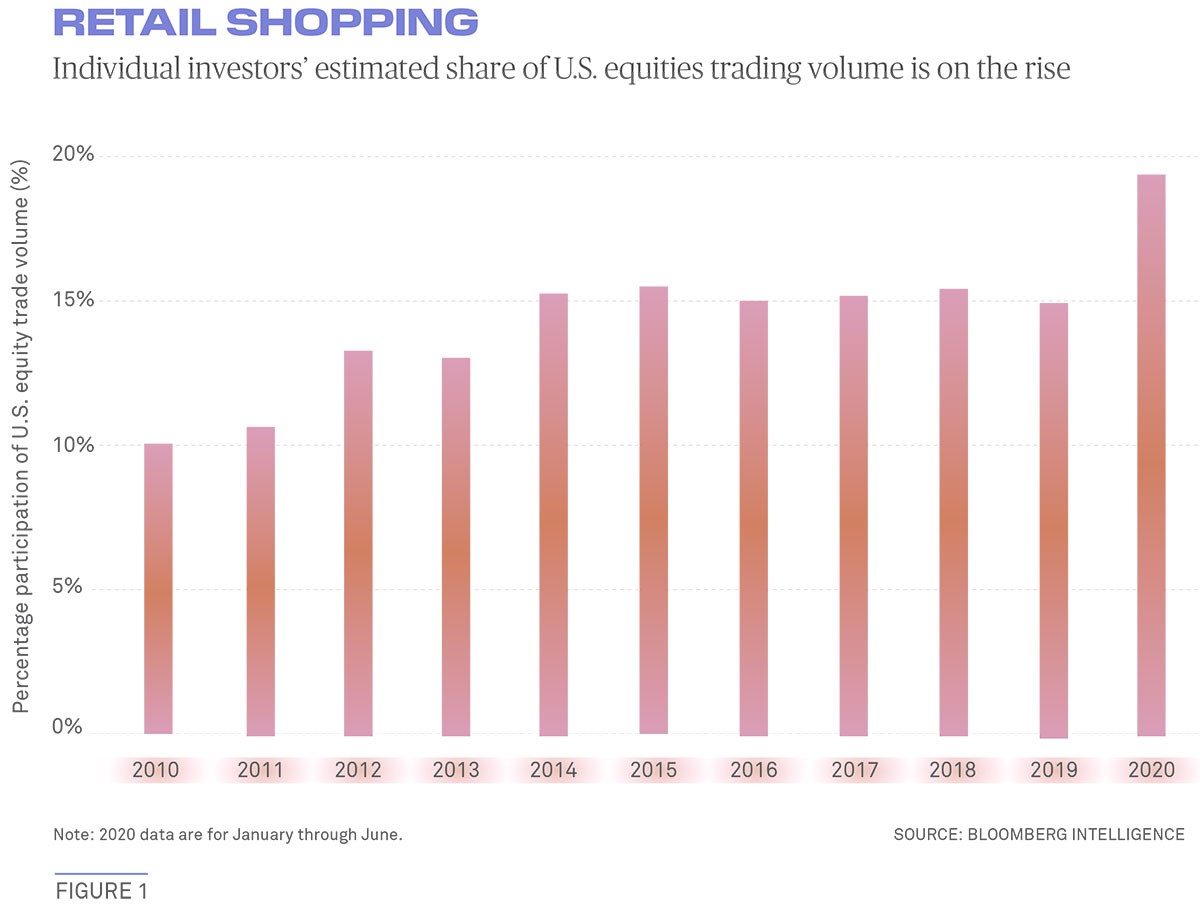

Individual trade flow at the start of the year neared record levels. On January 27, there were 24 billion shares traded, versus around 10 billion shares traded daily as of mid-April. Analysis from Bloomberg Intelligence estimates 23% of all U.S. equities off-exchange trading volume in the first quarter of this year came from retail investors, up from 20% in 2020 (see figure 1).

The proportion of retail flow on equities exchanges is thought to be higher still. Last July, Joseph Mecane, Head of Execution Services at broker dealer Citadel Securities, told Bloomberg that retail investors accounted for as much as 25% of U.S. equity trading on busy days, up from 10% in 2019. A spokesman for Citadel, which handles approximately 40% of U.S.-listed retail volume, declined to provide an updated figure, stating that recent trading “was too volatile [and] likely an aberration.”

The trend started last year, with the onset of COVID-19 creating a larger population of day traders, who could buy and sell from their mobile phones, trade algorithmically, or even use large amounts of borrowed money. Retail flow has played a large part in driving the price action in U.S. equities ever since, although participation has been outsized since the middle of 2020. Lately, it has spread even to cryptocurrencies, as evidenced by the interest surrounding Coinbase Global, a cryptocurrency exchange, which conducted a direct listing in April.

“The psychology and sociology of this relates to the pandemic and mom, pop and millennials having access to institutional technology,” Ron Hooey, Head of Institutional Equities Sales at BNY Mellon. “It was the perfect storm for all of this retail frenzy to occur, and it’s going to impact transparency.”

Much of the commentary on meme stocks has portrayed the group of retail investors as a relatively small group of activist millennials, using social media to successfully squeeze hedge funds out of their short positions. But data from Cboe show that retail trading is much broader.

Participation is not concentrated solely in the 15 or so headline-grabbing names that initially dominated the coverage. It has evolved to cover at least 50 names, based on the number of companies in which online brokerage Robinhood Markets restricted trading on January 29 at the height of the meme stock mania.

Many hedge funds were short GameStop — Melvin Capital Management, most transparently — but once the potential to execute a short squeeze in the position became widely known, institutional money flooded into GME too.

“Around August 2020, principal dealers began to receive a lot of order flow from retail investors looking to buy stocks trading below $5, whereas that kind of activity was in the low single digits pre-COVID.”

— ADAM INZIRILLO, CBOE GLOBAL MARKETS

The surge in meme stock investing has not been reflected in trading volumes for traditional retail passive investing vehicles such as exchange-traded funds (ETFs) and mutual funds. In the fourth quarter of 2019, ETFs accounted for about 12% of total U.S. equities volumes, but by the fourth quarter of 2020, they had fallen to about 6%, according to Cboe.

As the second quarter gets underway, retail investors appear to be taking a breather (see figure 2), perhaps because there are now more distractions with restaurants opening back up and COVID-19 vaccines being rolled out. Average daily volumes of shares transacted as of mid-April have fallen 38% from their 15.6 billion January average, according to Cboe. Despite this pullback, experts say the new set of traders are more educated on investing and will remain a force in markets.

Low Barriers to Entry

A number of obscure names that have drawn the attention of retail investors in the sub-$5 range have seen their valuations explode this year as a result of retail interest. Relatedly, they have sparked interest in stocks priced below $1 – the so-called “penny” stocks.

“Around August 2020, principal dealers began to receive a lot of order flow from retail investors looking to buy stocks trading below $5, whereas that kind of activity was in the low single digits pre-COVID,” says Adam Inzirillo, Head of North American Equities at Cboe.

The breadth and extent of the interest goes beyond U.S. equities, too, taking in stocks such as U.K.-based Critical Metals and Canada-based Sundial Growers. Stock analysts at Cboe observe that overseas retail flows have entered the U.S. market though international retail brokerages such as Interactive Brokers and Webull Financial.

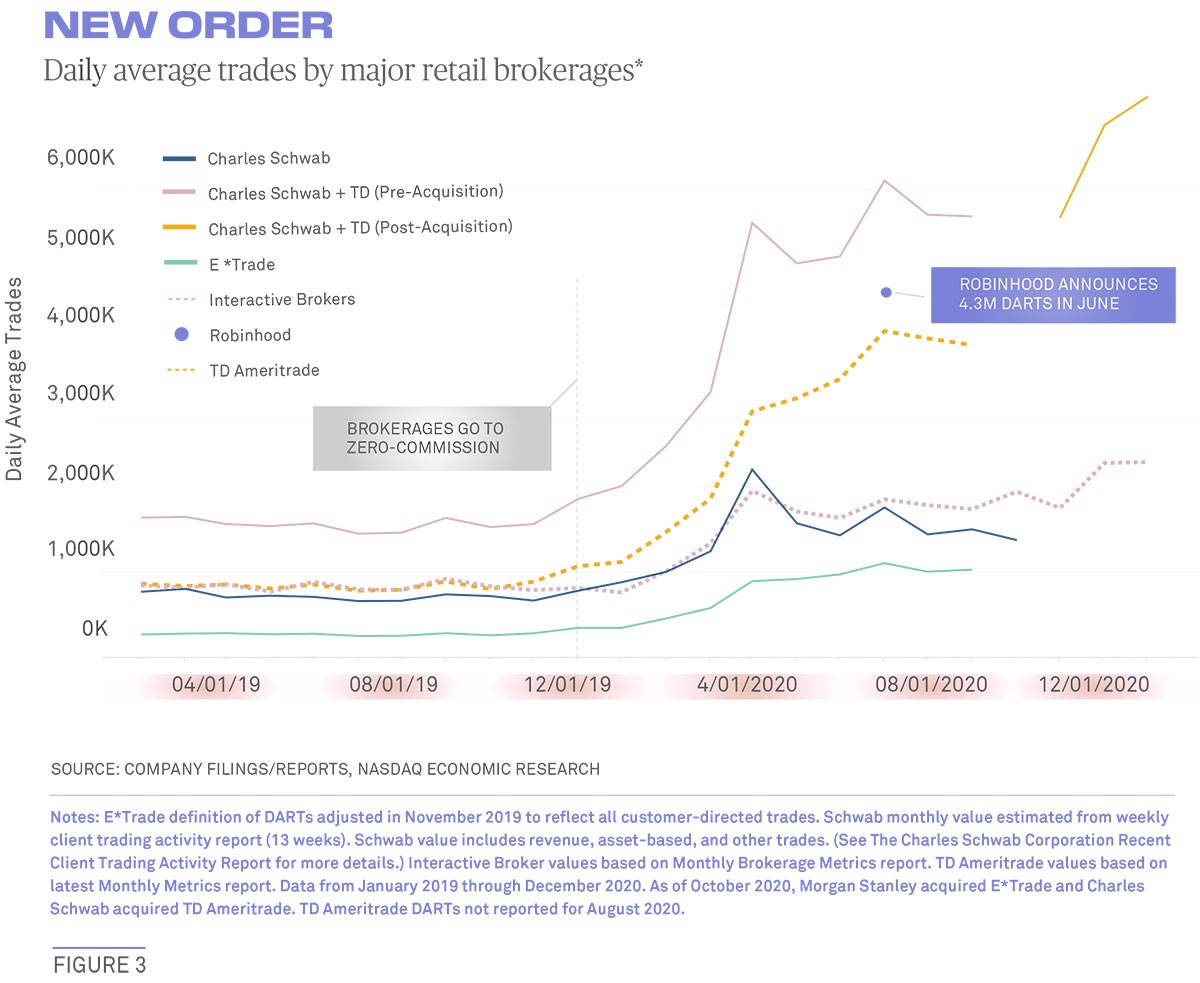

Analysts attest that the recent proliferation of zero-commission trading was the primary catalyst for the eruption in retail stock picking (see figure 3), along with a fear by day-traders of missing out on a quick win. While Robinhood introduced commission-free trading in 2015, Charles Schwab became the first of the large established retail brokerages to eliminate its commission fee in October 2019. Within weeks, TD Ameritrade, E*Trade and Fidelity Investments had done the same, and a few months later, Vanguard followed suit.

Previously, brokerages had typically offered only commission-free trading in their own families of passive investing products such as ETFs and mutual funds. But as 2020 dawned, retail investors stood on the precipice of a new decade in which, for the first time, even the most cursory hurdle to speculating in single stocks had been removed.

Marry that with the electronification of markets, proliferating chatter on social media sites and a global pandemic, and the result was crowdsourced trading ideas that could build quickly in different corners of the internet simultaneously.

Robinhood added 3 million new users in the first four months of 2020 alone, according to Co-Founder and Chief Executive Vladimir Tenev. By February 2021, the platform boasted 13 million users with as many as 600,000 new downloads of the Robinhood app on January 29, the height of the GameStop trading frenzy.

The impact that these millions of new retail participants were having in the U.S. equity market soon became apparent. In the first two pre-pandemic months of 2020, the total number of shares transacted across U.S. equities exchanges held steady at between 7.8 billion and 8.3 billion, according to Cboe. Then, in March 2020, both the number of shares transacted and the trade volume surged. But even as valuations began to sharply recover, activity was consistently north of 10 billion shares traded daily.

A significant part of this heightened activity was coming from retail investors and still is. “Our average daily orders were up 302% compared to 2019, and the majority of that increase was coming from retail accounts,” says one director on a retail equities brokerage desk in New York.

Options were another reflection of their participation. Single-contract options trades in December were more than double their levels from a year earlier, with retail constituting 8% of those volumes, says Cboe.

All Powered Up

As 2021 began and the meme stock trading mania kicked into high gear, the number of shares traded hovered close to the 15 billion mark on U.S. equities exchanges, while the total trade count bounced around 80 million. This was up from 8.4 billion and 43 million respectively, a year earlier. The lion’s share of these were driven by retail investors.

Not only was the flow notable because of its origins, but the composition of the order flow was markedly different from the names that had traditionally been the most active, such as Tesla or Facebook, Amazon, Apple, Netflix and Google (FAANG stocks).

“If you added a charge of 0.1% on to the cost of a transaction, that would be enough to discourage the zero-commission day-trading retail speculators.”

— TERESA GHILARDUCCI, NEW SCHOOL

“The orders for the FAANG-type names that have typified retail order flow in recent years were supplanted for days, running. On many days, GME was the number-one name that we were executing,” recalls the retail equities director.

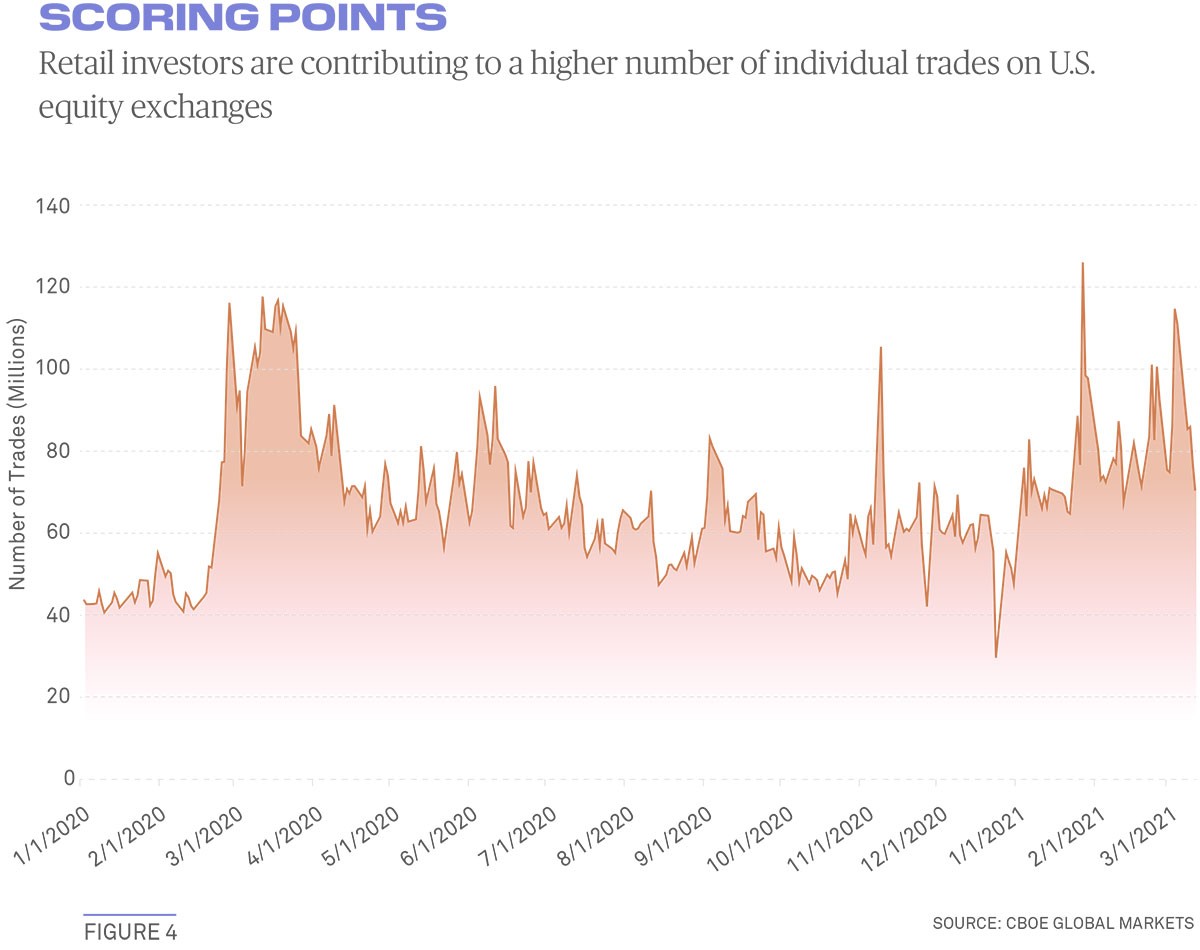

January 27 — the day of GME’s all-time high — was by far the busiest day for activity on U.S. equity markets, with 24.5 billion shares traded during that session across 126 million trades, according to Cboe (see figure 4).

As extraordinary as those numbers are, the continuation of elevated trading activity through February and into March was even more meaningful. Ten of the busiest days for electronic order flow into the retail equities desk occurred in January and February of this year, for example.

“Despite all the focus on the market action at the end of January, the story that the market data is telling us is clear: this retail investing surge is far from over,” says Cboe’s Inzirillo.

The meme stock phenomenon has already attracted the attention of leg-islators and regulatory authorities, who have expressed some interest in structural reform. In February, the House Financial Services Committee held hearings at which policymakers raised concerns about the “gamification” of investing and the potential risks to novice retail investors.

Many questions were focused on the “payment for order flow” business model used by retail brokerages, arrangements in which brokerages receive compensation for directing client order flow to a particular market maker. The theory is that there could be a conflict of interest there: If the broker is being paid for order flow, it might be more concerned with nurturing those relationships than maintaining high execution quality for retail customers.

At a hearing of the Senate Banking Committee on March 9, senators questioned whether commission-free trading is actively encouraging amateur investors to speculate on meme stocks, and whether regulation is required to protect them from themselves.

Testimony from witnesses was conflicting, with some advocating for restrictions to be imposed in this area, and one senator questioning whether the design features of retail trading apps should be regulated to combat the gamification appeal to young investors. “If you added a charge of 0.1% onto the cost of a transaction, that would be enough to discourage the zero-commission day-trading retail speculators, without negatively impacting long-term institutional investors like pension funds,” says Teresa Ghilarducci, Professor of Economics and Policy Analysis at the New School in New York, who testified before the Senate Banking Committee.

Other witnesses disagree with that assessment. Andrew Vollmer, Senior Affiliated Scholar with the Mercatus Center at George Mason University, argues that zero-commission trading is the result of a multi-year competition between brokerages to drive down execution costs for the customer. He suggests that if the payment for order flow model was prohibited, brokerages would compete to eliminate fees in other areas.

“Misleading market information, misconduct — yes, regulate against those behaviors. But you cannot regulate away the risk of losing money in financial markets,” says Vollmer.

Administrative Privileges

For now, payment for order flow has attracted the most serious political and regulatory scrutiny, because it potentially puts retail brokerages at odds with their customers if their revenue comes from wholesalers, not retail. At issue will be the question of whether or not it can be demonstrated that investors receive best execution — as demanded by U.S. law — and price improvement under the payment for order flow model.

Another likely area for scrutiny is the amount of time it takes to settle trades. Currently, U.S. stocks settle on the second day after the trade is agreed, a convention known as T+2. If instead the market moves to a single day, or T+1, it might reduce the trade settlement risk in the middle office to one day of exposure from two, and help discourage some of the more worrying speculation.

Even if Congress does not enact changes, it seems likely that incoming Securities and Exchange Commission Chairman Gary Gensler will address the issue. The SEC and the Financial Industry Regulatory Authority have longstanding mandates to protect retail investors.

Asked about the meme stock phenomenon during his Senate confirmation hearing in March, Gensler offered only rhetorical responses. “How do we protect investors using trading applications with behavioral prompts designed to incentivize customers to trade more?” he asked.

How does the meme stock episode end? With new $1,400 stimulus checks being deposited into the accounts of hundreds of millions of Americans, many analysts expect the trading craze to continue.

The Securities Industry and Financial Markets Association (SIFMA) is on its own fact-finding mission. The trade body issued a survey of its trading committee members and exchange contacts in mid-April, asking them for their thoughts on the “new normal” for volatility and volumes, as well as “risks to markets.” SIFMA said in the note that such responses would be of interest given the “difficulty in quantifying the levels of retail participation.”

Although retail volumes have fallen from their recent peak, what’s clear is that many of those investors are moving in tandem - and with some analysis guiding them, they can build momentum in the stocks they target. Whether their participation moving forward is frenzied or more muted, their rise has brought a lot of new traders to the marketplace who are now engaged in their finances in ways they never were before.

“When I was a finance professor during the dot.com bubble, I used to ask my undergrad students how many were trading stocks [online], and they would tell me how much they were making and how easy it all was,” says Michael Piwowar, executive director of the Milken Institute Center for Financial Markets and former a SEC Commissioner.

“That was in the days of having to pay $10 or $20 to make a trade. If it was easy then, how easy is it now when there are no commissions?” he asks.

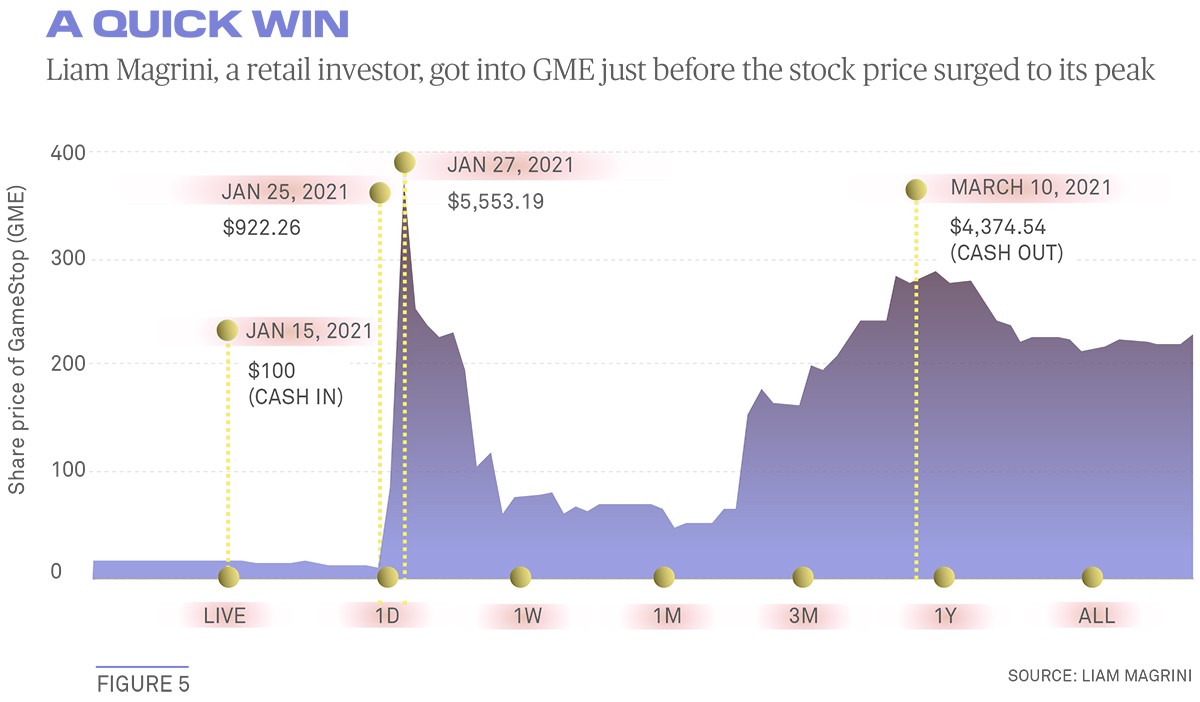

Liam Magrini, a 21-year-old music production student who lives with his mother in Brooklyn, saw the chatter about shares in GameStop (GME) “going to the moon” on the Reddit WallStreetBets discussion board in early January and — against the advice of friends — invested $100, when the stock was priced at $54.

Fellow Gen-Z investors were encouraging people to hold on to their positions, no matter how wild the ride. “GME was about to blow and Robinhood was on the front page of the App Store,” he recalls. “Diamond Hands was all you heard, all the time,” he adds, referring to a “meme” culture phrase to applaud personal fortitude in holding a stock amidst volatile trading.

“GME was about to blow…and ‘Diamond Hands’ was all you heard.”

— LIAM MAGRINI, RETAIL INVESTOR

Between Jan. 25 and Jan. 27, the peak price of GME, his then-$922.26 investment had risen to $5,553.19 (see figure 5). He decided not to borrow money from Robinhood on margin, although it was offered to him, and cashed out on March 10, when the stock was at $265 and the position was worth $4,374.54.

He says it gave him a taste for more sophisticated investing. In February, he started investing in a 2x leveraged oil and gas ETF offered by Direxion (GUSH), which delivers twice the daily gains or losses of the S&P Oil and Gas Exploration & Production Select Industry Index. “It just so happens came in at the right time,” says Magrini. “I don’t know too much, so I don’t want to push my limits.”

Peter Madigan is editor-at-large for BNY Mellon Markets.

Questions or Comments?

Contact Ron Hooey or reach out to your usual BNY Mellon relationship manager.

BNY MELLON CAPITAL MARKETS DOES NOT SERVICE RETAIL ACCOUNTS