Stock Lending: Dispelling the Myths

Recent industry efforts to improve transparency in stock lending and bolster shareholder engagement

Stock Lending: Dispelling the Myths

Recent industry efforts to improve transparency in stock lending and bolster shareholder engagement

January 2020

By Peter Madigan

One of the world’s largest pension funds sent shockwaves through markets by suspending its equity lending program. The decision has brought the subject of corporate governance to the forefront of securities finance.

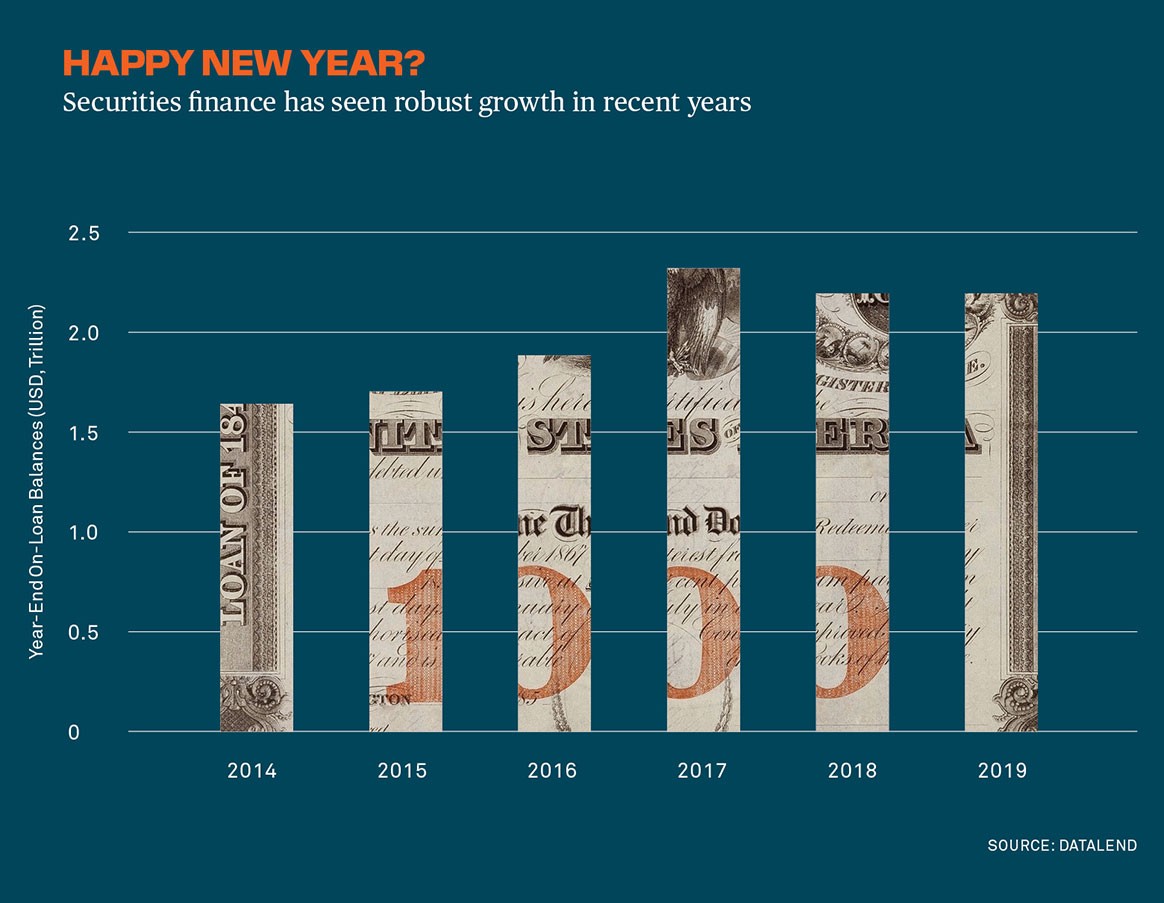

Last year was one of the stronger periods for securities finance since the global financial crisis. Coming off a stellar 2018, which saw beneficial owners collect $9.69 billion in lending revenues — a post-crisis record — gross full-year income for 2019 came in at a still-respectable $8.66 billion, according to statistics from DataLend.

An otherwise generally positive year for securities finance was capped off, however, by the December 3, 2019 announcement by the Government Pension Investment Fund (GPIF) of Japan that it had “decided to suspend stock lending until further notice.” The suspension does not include the fund’s portfolio of fixed-income securities, which it continues to lend.

GPIF explained its decision on two grounds. The first was that the transfer of stock ownership rights during the course of a securities loan is “inconsistent with the fulfillment of the stewardship responsibilities of a long-term investor.”

The second reason was just as succinct: “the current stock lending scheme lacks transparency in terms of who is the ultimate borrower and for what purpose they are borrowing the stock.”

Given GPIF’s status as one of the world’s largest public pension funds, the suspension attracted extensive media coverage. The fund held a $383 billion portfolio of foreign equities at the end of the first quarter of 2019, but it has not disclosed securities lending income since 2017, collecting $81 million in revenue from lending activities during that year. Calls to the fund were not returned.

GPIF is not the only fund reviewing equity lending within a corporate governance context. In October 2018, Korea’s National Pension Service (NPS) announced it would halt domestic equity lending while it analyzed the “correlation between local share lending and short selling.” NPS continues to lend its global equities portfolio, however, while it evaluates its position regarding onshore stocks.

In spite of the reviews underway by the two investment giants, a broad community of market participants insists that short sellers do provide a range of benefits to the market, not least in acting as a countervailing force against overvalued securities.

Certain regulatory bodies have agreed. In December 2019, the European Securities and Markets Authority (ESMA) issued a report analyzing short-term pressures facing corporations. The body considered arguments concerning the impact of short selling and securities lending practices and their potential link with short-termism.

“The current stock lending scheme lacks transparency in terms of who is the ultimate borrower and for what purpose they are borrowing the stock.”

— GOVERNMENT PENSION INVESTMENT FUND OF JAPAN

“ESMA points out that short selling and securities lending are key for price discovery and market liquidity,” the report states. It went on to say that “ESMA is not aware of concrete evidence pointing to a cause-effect connection between these practices and the existence of undue short-term market pressures” and that “securities lending, if done in a controlled way, is an opportunity to add value for fund investors and [is] compatible with long-term investment strategies.”

Substantial work has also been undertaken in recent years by nongovernment standard-setting organizations and industry bodies, such as the International Securities Lending Association (ISLA), to address some of the concerns outlined by GPIF.

On December 16, 2019, ISLA announced the formation of a new Council for Sustainable Finance, which will introduce a series of Principles for Sustainable Securities Lending in the first quarter of this year aimed to promote and embed environmental, social and governance (ESG) values into securities lending.

These are just the latest developments in a long sequence of industry improvements to enhance market transparency and provide reassurance that strong corporate governance frameworks support responsible securities lending programs.

“ESMA points out that short selling and securities lending are key for price discovery and market liquidity,” the report states. It went on to say that “ESMA is not aware of concrete evidence pointing to a cause-effect connection between these practices and the existence of undue short-term market pressures” and that “securities lending, if done in a controlled way, is an opportunity to add value for fund investors and [is] compatible with long-term investment strategies.”

Substantial work has also been undertaken in recent years by nongovernment standard-setting organizations and industry bodies, such as the International Securities Lending Association (ISLA), to address some of the concerns outlined by GPIF.

On December 16, 2019, ISLA announced the formation of a new Council for Sustainable Finance, which will introduce a series of Principles for Sustainable Securities Lending in the first quarter of this year aimed to promote and embed environmental, social and governance (ESG) values into securities lending.

These are just the latest developments in a long sequence of industry improvements to enhance market transparency and provide reassurance that strong corporate governance frameworks support responsible securities lending programs.

“The rules represent a giant leap forward in terms of transparency for the industry. ”

— BILL KELLY, BNY MELLON

Improving Transparency

That’s because the contractual relationship between two counterparties involves only the borrower and lender. This means that beneficial owners have no legal nexus with any third parties that may buy or sell securities from the original borrower, nor any visibility into what a borrower intends to do with the loaned stock — whether to meet regulatory requirements or to sell the securities to pursue a short strategy.

While naked short selling (that is, selling equities prior to borrowing the shares) is banned in numerous jurisdictions, securities lending is utilized to legitimately enable covered short selling in line with regulatory guidance, as the ESMA December 2019 report reaffirmed.

For beneficial owners like GPIF that may be concerned about the motivation of borrowers, agent lenders have for some time offered capabilities to lenders that enable them to precisely customize what assets they lend out, under what terms and to whom.

These tools allow beneficial owners to specify cohorts of borrowers they are unwilling to lend to — hedge funds, for example, place thresholds on the amount of securities they’re willing to lend to a specific entity, or direct that particular equities in their portfolio are restricted from being lent to particular borrowers.

Loan Recall

GPIF’s other concern over stock lending — the ability to recall a loan in order to exercise shareholder voting rights — has made beneficial owners cautious about lending out securities. Understandably, many are anxious that following the legal transfer of ownership, the ability of shareholders to engage in voting may be impeded.

While this may indeed be the outcome in a “hard” term loan, which contractually removes the standard right of the lender to recall securities, “soft” term loans and overnight rolling lending arrangements can easily address this issue through a simple loan recall. This includes calling in a loan over the record date when a coupon or dividend payment is made.

“Agent lenders can recall securities ahead of a corporate action and effectively replace the loan with the borrower for the required period,” explains Ina Budh-Raja, Director of Securities Finance Product & Strategy at BNY Mellon, who is also an ISLA board member and Bank of England Money Market Committee member. “In fact, that capability has been a staple of the market for years and is generally a seamless process for clients utilizing larger agency programs, due to the size of available stock inventory and the varying appetites of a diverse pool of lender types.”

Such recalls are a well-established element of larger agency programs and are supported by boilerplate securities finance agreements like the Global Master Securities Lending Agreement (GMSLA). Although the issue of voting rights may seem more opaque, the GMSLA is nevertheless clear that any lender may indeed exercise its voting rights by recalling lent securities.

“Lenders can recall their securities whenever they want, for whatever reason they want, and they do not have to provide an explanation. All they need to do is ensure the request is made in good time so that we do not interrupt their investment lifecycle,” clarifies Paul Solway, Head of Securities Finance, APAC, at BNY Mellon and communications officer for the Pan Asia Securities Lending Association (PASLA).

In addition to recalls of loaned securities, collateral securities may be substituted by a borrower at any time, provided they deliver equivalent acceptable collateral to the lender.

The recent emergence of collateral pledge arrangements as an alternative to the traditional transfer of title within a securities loan transaction has also introduced a partial solution to the issue of the exercise of voting rights in collateral securities — at least for the borrower. Under a pledge, legal title transfer of securities ownership does not take place on the collateral, meaning that the borrower retains all proxy rights and dividend distributions of its non-cash collateral. In addition, the body of literature providing corporate governance guidance around how securities lending can coexist with shareholder responsibilities is extensive and growing.

“Lenders can recall their securities whenever they want, for whatever reason they want, and they do not have to provide an explanation. All they need to do is ensure the request is made in good time so that we do not interrupt their investment lifecycle ”

— PAUL SOLWAY, BNY MELLON

The Bank of England’s UK Money Markets Code, for example, sets out regulatory best practice standards for UK market participants and states that borrowers should not borrow securities for the purpose of accruing voting rights.

Other resources on the importance of robust corporate governance in stock loans include the International Corporate Governance Network’s Securities Lending Code of Best Practice and the European Fund and Asset Management Association’s Stewardship Code.

An EU directive called the Shareholder Rights Directive II adds additional clarity on how a thoughtful and well-managed securities lending program can be entirely in accordance with a thorough ESG program.

Suitable Candidates

There is one final but significant point in the GPIF statement that has been largely overlooked in the coverage so far. That is the fund’s wish to continue to engage in constructive dialogue with investee companies “not only during the annual shareholder meeting season, but throughout the year.” This intention raises a deeper question: are such proactive investors that wish to be intimately involved in the direction of the companies they invest in suitable candidates for securities lending in the first instance? If investors wish to take an active role in the exercise of proxy rights and directly influence corporate governance, arguably lending out their portfolio may run counter to that goal.

The debate following the GPIF announcement has focused largely on securities finance and whether the practice is compatible with responsible governance, to the exclusion of a wider discussion about the suitability of activist investors to participate in stock lending.

“Every beneficial owner needs to develop a thoughtful and defined policy on securities lending ”

— PAUL WILSON, IHS MARKIT

While GPIF has concluded that stock lending may be inconsistent with what it views to be its stewardship responsibilities, the fund’s decision should not be interpreted — as it has by some — as a repudiation of securities finance generally.

That is borne out by another line of the GPIF statement: “The stock lending scheme may be reconsidered in the future if improvements are made to enhance transparency.”

Whether the GPIF stock lending suspension is a one-off or the beginning of a wider reexamination of securities lending, market statistics reveal that the number of asset owners making their portfolios available for lending is actually increasing.

Analysis by DataLend shows that the supply of lendable assets being made available by beneficial owners climbed to $20 trillion in 2019 from $19.5 trillion the previous year.

To put in perspective how swiftly lendable volumes are climbing: inventories only crossed the $17 trillion threshold in May 2017, with equities representing the lion’s share of the recent increase, according to data from IHS Markit.

If nothing else, this suggests that as the fee war among the world’s largest investment firms continues to intensify, ever larger numbers of asset owners are coming to recognize the value securities lending can deliver in generating incremental alpha.

Perhaps the most important consideration for governance-minded beneficial owners is the need to establish a structured and detailed securities lending policy. The United Nations Principles for Responsible Investment (UNPRI) Practical Guide to Active Ownership in Listed Equity highlights eight real-world instances of companies with notable corporate governance- focused securities lending policies.

For example, UniSuper, an Australian asset owner, recalls all domestic stock for voting and determines whether to recall international stocks on the basis of cost/benefit.

BNP Paribas Asset Management, meanwhile, monitors the number of shares on loan prior to a vote. If the firm determines too many securities are on loan or the vote is an important one, it will recall stock or restrict equities lending in order to vote on its position.

“Every beneficial owner needs to develop a thoughtful and defined policy on securities lending,” concludes Paul Wilson, managing director and head of Securities Finance at IHS Markit. “Those that have a well-considered, balanced policy in place will be able to reconcile strong corporate governance and appropriate levels of shareholder engagement with the incremental economic returns from securities lending. Such a framework will allow beneficial owners to fulfill their fiduciary duties to investors and beneficiaries.”

Questions or Comments?

Write to John T. Fox in BNY Mellon Markets US, Stephen Kiely in BNY Mellon Markets EMEA, Paul Solway in BNY Mellon Markets APAC, or reach out to your usual relationship manager.