Help For Europe: A Bold New Funding Plan

Help for Europe: A Bold New Funding Plan

June 2021

By Jeremy Grant

The European Union’s unprecedented foray into the capital markets promises not only a green, digital transformation for the region but potentially a new era of supranational borrowing.

For much of the past nine months officials at the European Commission have been holed up in the Drosbach building, a sprawling office complex in the capital of Luxembourg, working on a plan to rescue Europe.

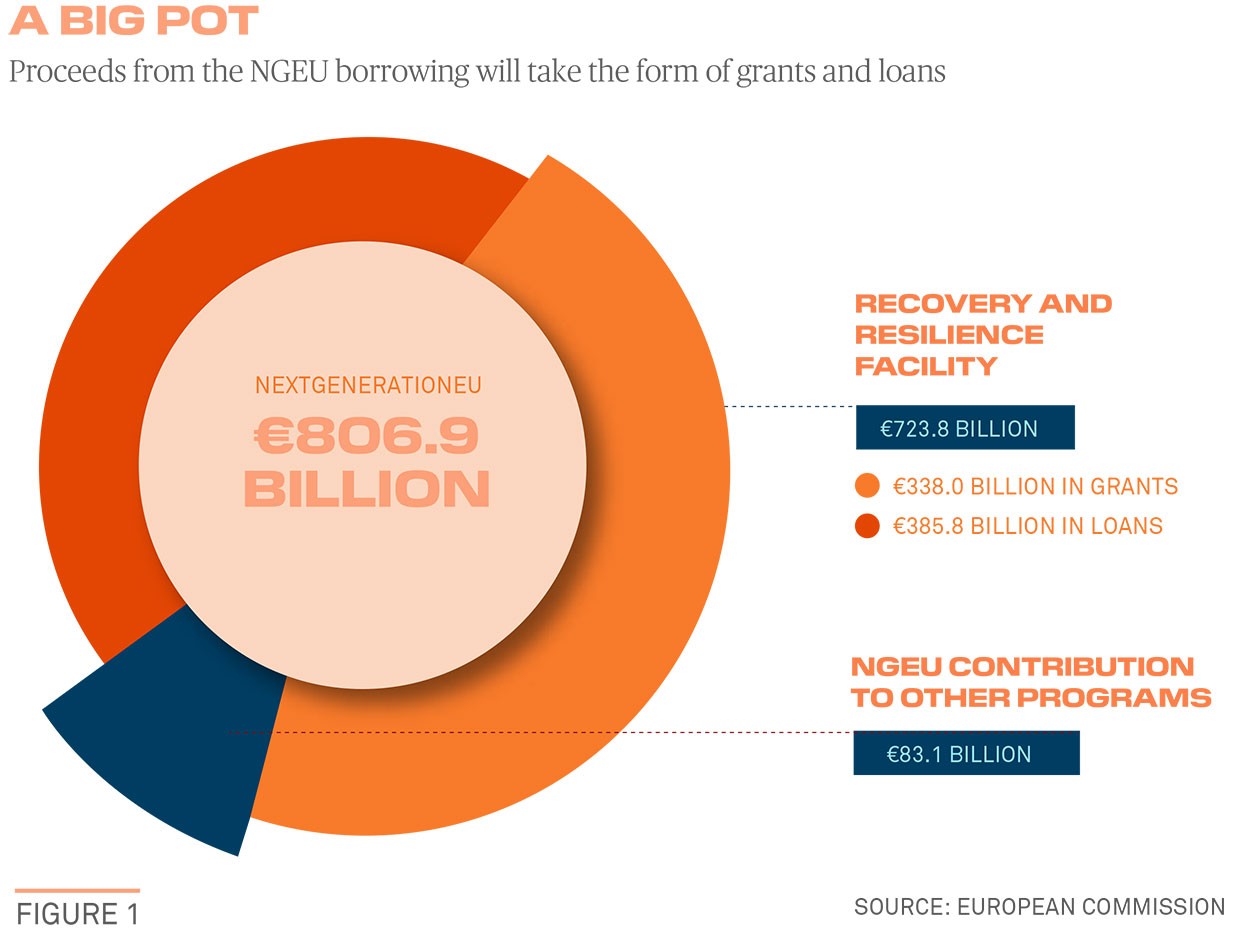

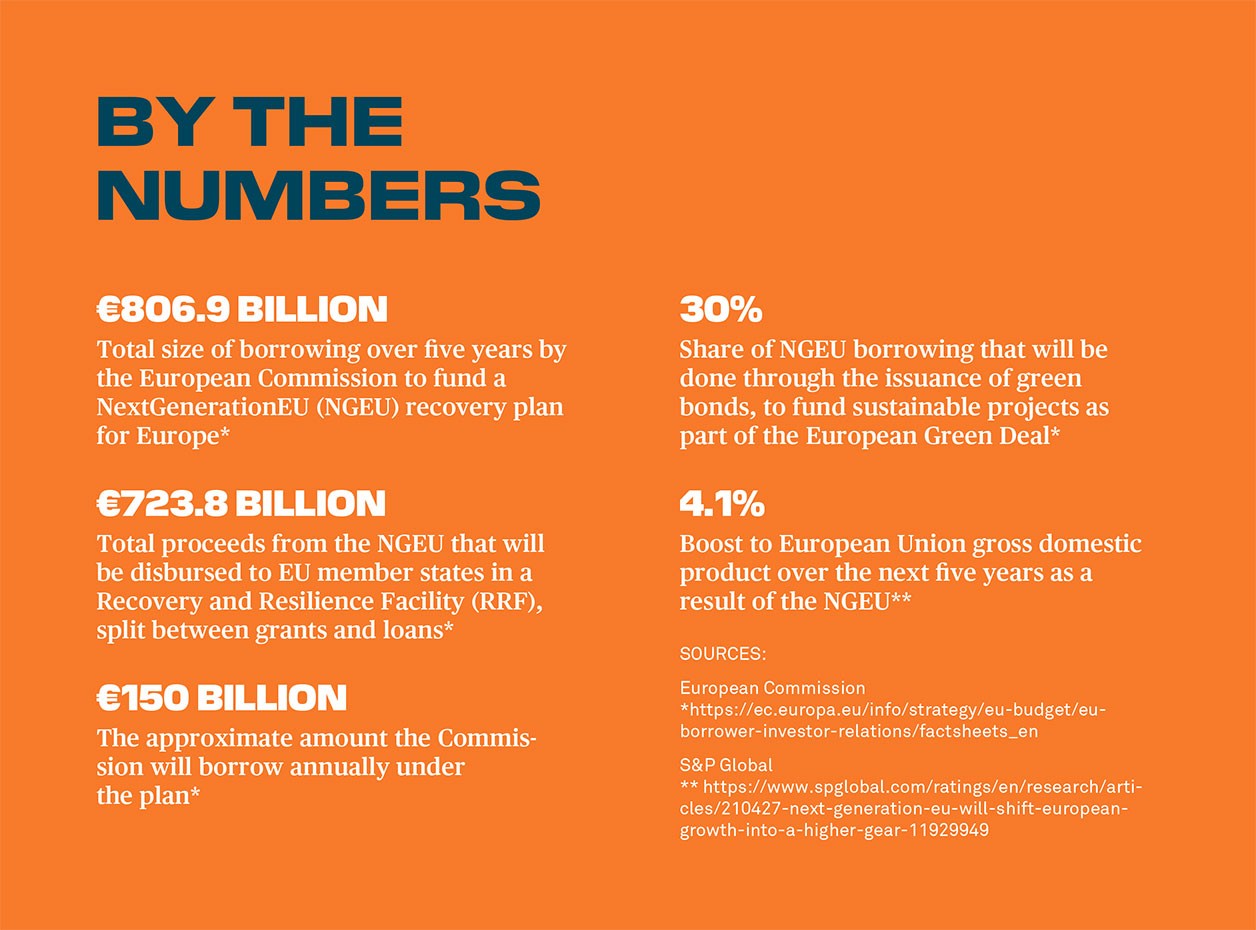

The team, which is part of the European Commission’s Directorate General for Budget, has been working on the design and launch of a massive €806.9 billion borrowing program (see Figure 1), funds from which are set to be dispersed to the EU’s 27 member states.

It marks by far the EU’s most significant foray into the capital markets to date, bringing a critical mass to its debt issuance and giving its bonds the potential to become a new benchmark for interest rates on financial assets across Europe.

The aim is not only to allow Europe to recover from the COVID-19 pandemic, but to emerge stronger by investing the bulk of the proceeds in a green and digital transition for the region.

Such a sizable borrowing plan would need to be carefully and clearly explained to prospective investors — including the nature and timing of the rollout and, crucially, how the money will be paid back. While the EU has borrowed before, this supranational program, known as NextGenerationEU (NGEU), is unlike anything it has attempted before.

“For the first time, the EU [will] finance national investment and reform programs of common interest through the issuance of common debt,” said Alessandra Perrazzelli, Deputy Governor for Banca d’Italia, on a recent video hosted by the Official Monetary and Financial Institutions Forum (OMFIF), a think tank.

Scheduled to kick off later this month, the program will be carried out in a series of annual tranches worth around €150 billion — equivalent to the annual borrowing of France.

Marion Amiot, senior economist for EMEA at S&P Global Ratings, estimates in a report that the NGEU program could add as much as 4.1 percent to the EU’s gross domestic product over the next five years.

The sheer size of the program means that, if successful, it would be almost as much as the total borrowing by Germany in the five years before the pandemic struck in early 2020. Johannes Hahn, EU Commissioner in charge of budget and administration, recently referred to the NGEU in a press statement as “a game-changer in EU capital markets.”

Some analysts and bankers go further, noting that while the EU would not technically be a sovereign issuer, the NGEU’s many similarities with sovereign borrowing programs would nonetheless make the EU one of the world’s largest supranational borrowers. Almost one third of the new debt issued will be in green bonds, used to fund sustainable projects and digitalize public administration across the EU.

“This is clearly a new chapter in the world of sovereign borrowing,” says David Marsh, chairman of OMFIF.

Success Factors

The project’s ambition inevitably raises questions over whether it can be rolled out and managed successfully in the way its architects hope. The Commission’s initial stumbles in managing another pan-European initiative, the rollout of COVID-19 vaccines, might lead some to be skeptical.

Here, the Commission is taking no chances. It has worked hard at planning and managing the project, starting immediately after EU leaders in July 2020 agreed to back a landmark pandemic recovery fund.

The team in Luxembourg is headed by Niall Bohan, an Irish national and Commission official with long experience in banking and capital markets. It ultimately reports to Gert Jan Koopman, a Dutch national who is head of the Directorate General for Budget, and who previously spent eight years as deputy director-general for EU state aid.

The Commission has said a key element of this is pursuing a diversified funding strategy. The Commission has pledged to publish its funding plans every six months in materials on its website; develop structured and transparent relationships with banks supporting the issuance program; manage its liquidity needs and maturity profile; and use a combination of auctions and syndications “to ensure cost-efficient access to the necessary funding on advantageous terms.”

“This is clearly a new chapter in the world of sovereign borrowing.”

— David Marsh, Official Monetary and Financial Institutions Forum

Finally, the Commission will set up a primary dealer network to facilitate an efficient auction and syndication process, support liquidity and ensure wide placement of the debt.

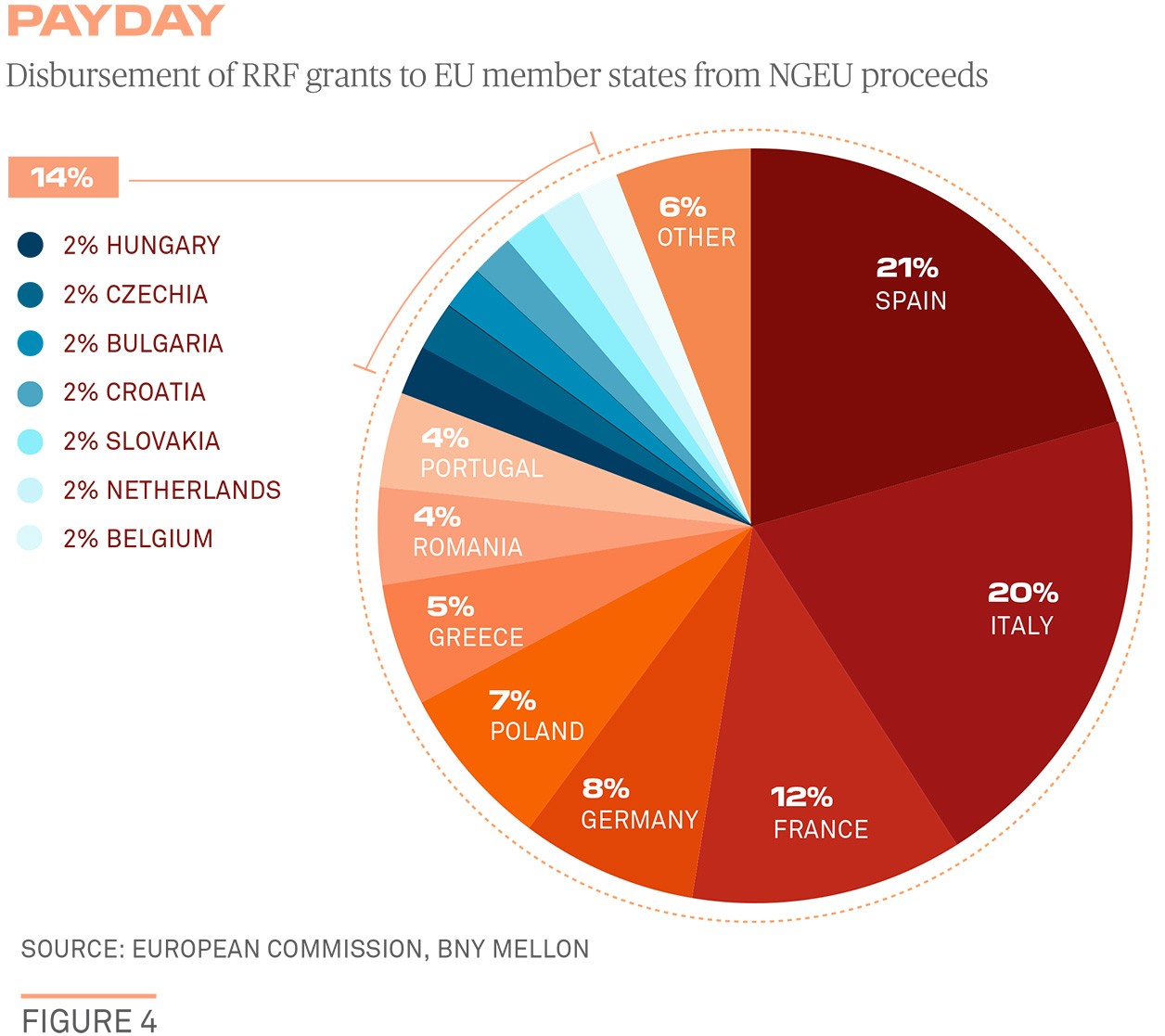

About 90 percent of the proceeds, €723.8 billion, will fund a “Recovery and Resilience Facility” (RRF), to be split between grants (€338 billion) and loans (€385.8 billion) for member states. The rest, €83.1 billion, will go toward six smaller projects.

Spain and Italy are by far the largest beneficiaries of those RRF grants, each set to receive about 20 percent of the proceeds, with France next at 11.6 percent, Germany at 7.6 percent and Poland receiving the fifth-largest amount at 7 percent.

“Given the volumes, frequency and complexity of the fund’s borrowing, the Commission is putting forward a debt management policy on a par with that of some of the most advanced EU sovereign borrowers,” Koopman told an OMFIF webinar in March.

Track Record

Building the NGEU program from scratch would be a daunting task, even for a sovereign. But bankers point out that the EU has a decent track record as a borrower, with an established yield curve, and is therefore something of a known quantity in the capital markets.

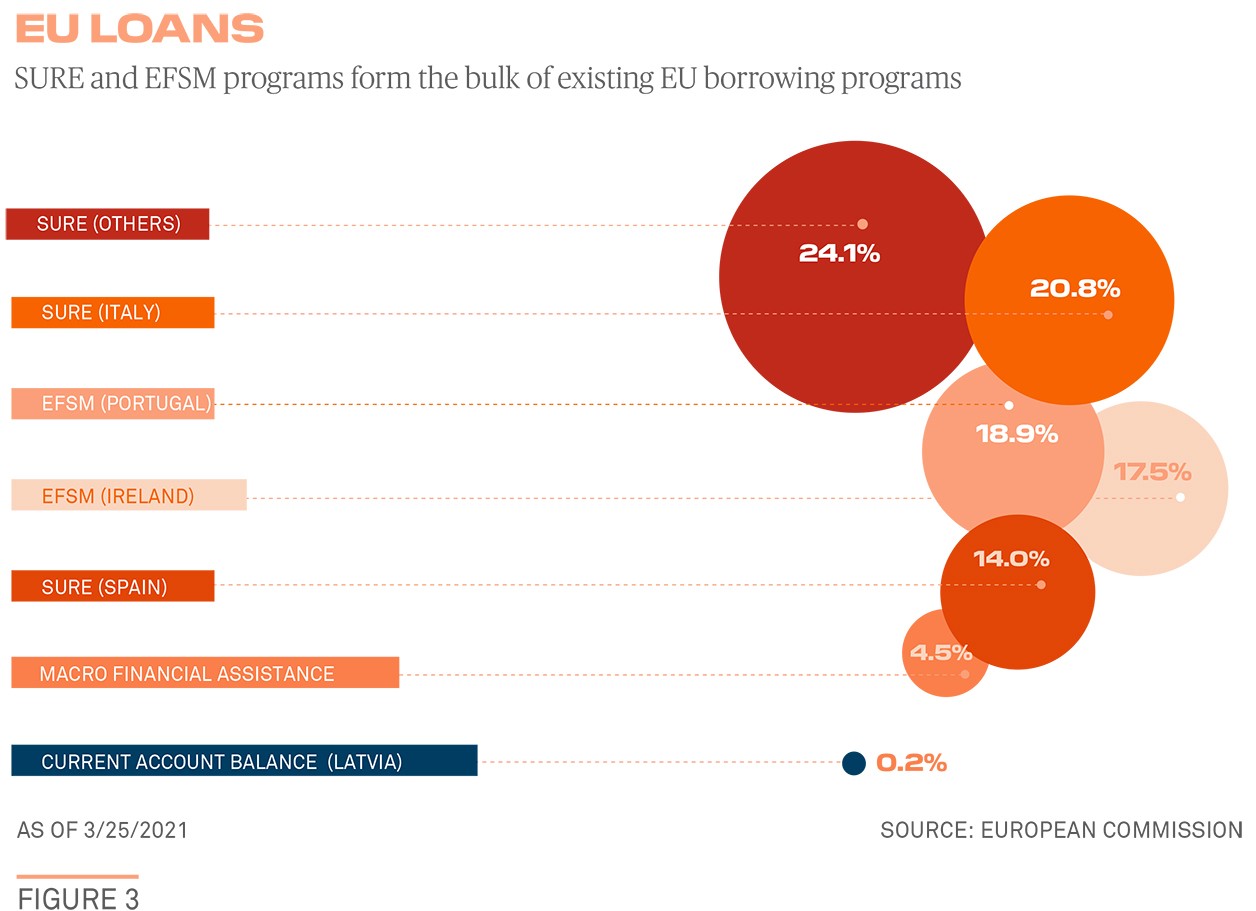

This can be traced back to the creation in 2010 of the European Financial Stabilisation Mechanism (EFSM), which raised emergency funds in response to the last eurozone crisis. The EFSM was succeeded by the European Stability Mechanism (ESM).

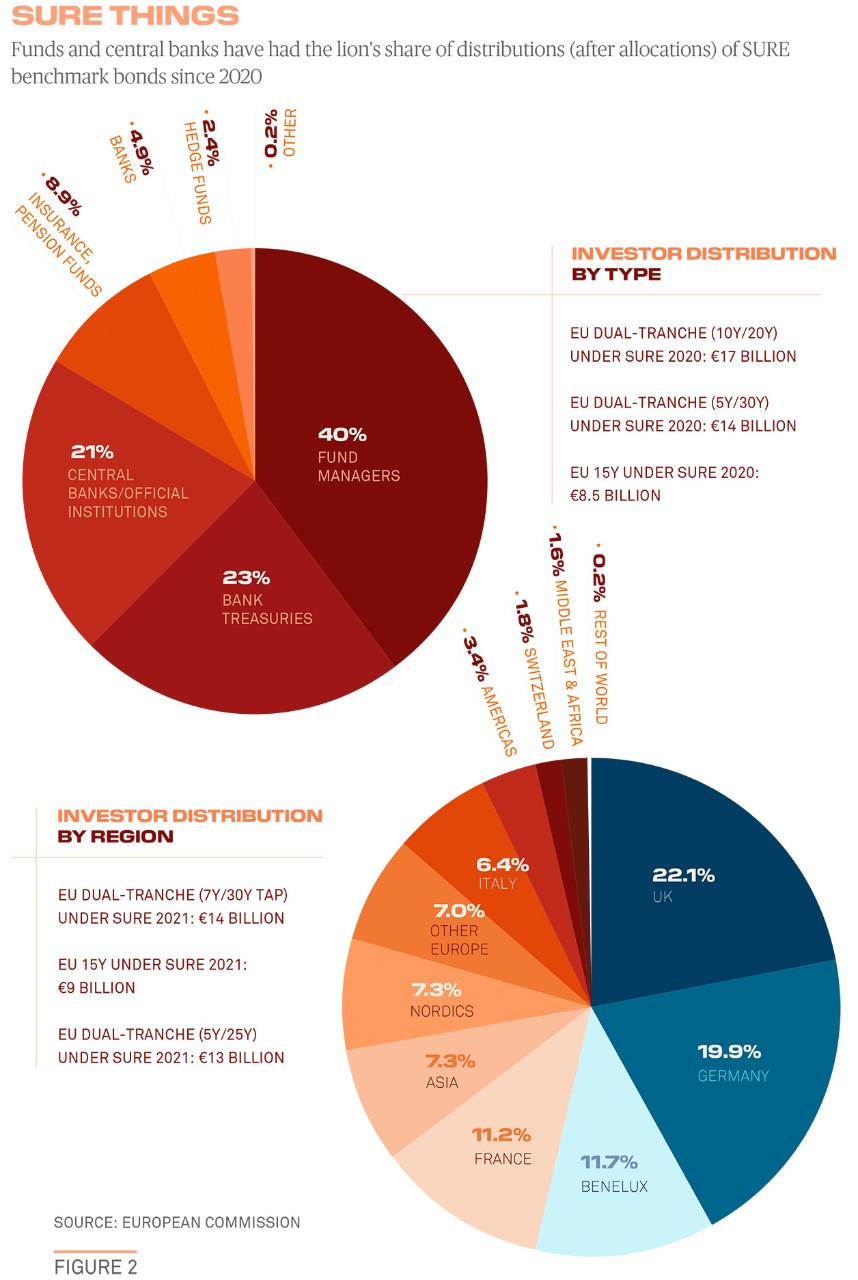

Another programs is called SURE (an acronym derived from “support to mitigate unemployment risks in an emergency”), created last year to provide loans to member states for protecting jobs affected by the pandemic. By May this year, 19 member states had received a total of nearly €90 billion under SURE (see Figure 2). Those bonds were not only oversubscribed but also carried a social label to demonstrate to investors that funds raised will be used for social objectives.

BNY Mellon already has some of those triple-A-rated EU bonds on its triparty collateral management platform, some of them used to finance loans under the SURE and EFSM programs. Eligibility of the new EU debt as collateral would depend on the specific characteristics of the issuance, the bonds’ liquidity characteristics, and how these matched up to clients’ collateral eligibility schedules.

Neal Ganatra, head of sovereign, supranational and agency debt syndicate at Deutsche Bank, says that the SURE program has been effectively “a test run” for the NGEU. Not only has it gone “extremely well” but it has attracted new investors — national treasuries, pension funds and sovereign wealth funds — because SURE’s deal sizes were comparable to those of the national sovereign issues that investors were already used to buying (see Figure 2).

“This track record puts them [the Commission] in a very good position to roll out the NGEU, given that they already have the experience of doing large transactions,” says Ganatra.

Much of that experience has been accrued by a key figure: Siegfried Ruhl, a German national seconded from the ESM in October 2020 to the NGEU as Counsellor to Koopman. He has a decade of experience, first at the EFSM and later at the ESM, managing around €300 billion of debt and correspondence with the program's 1,700 investors.

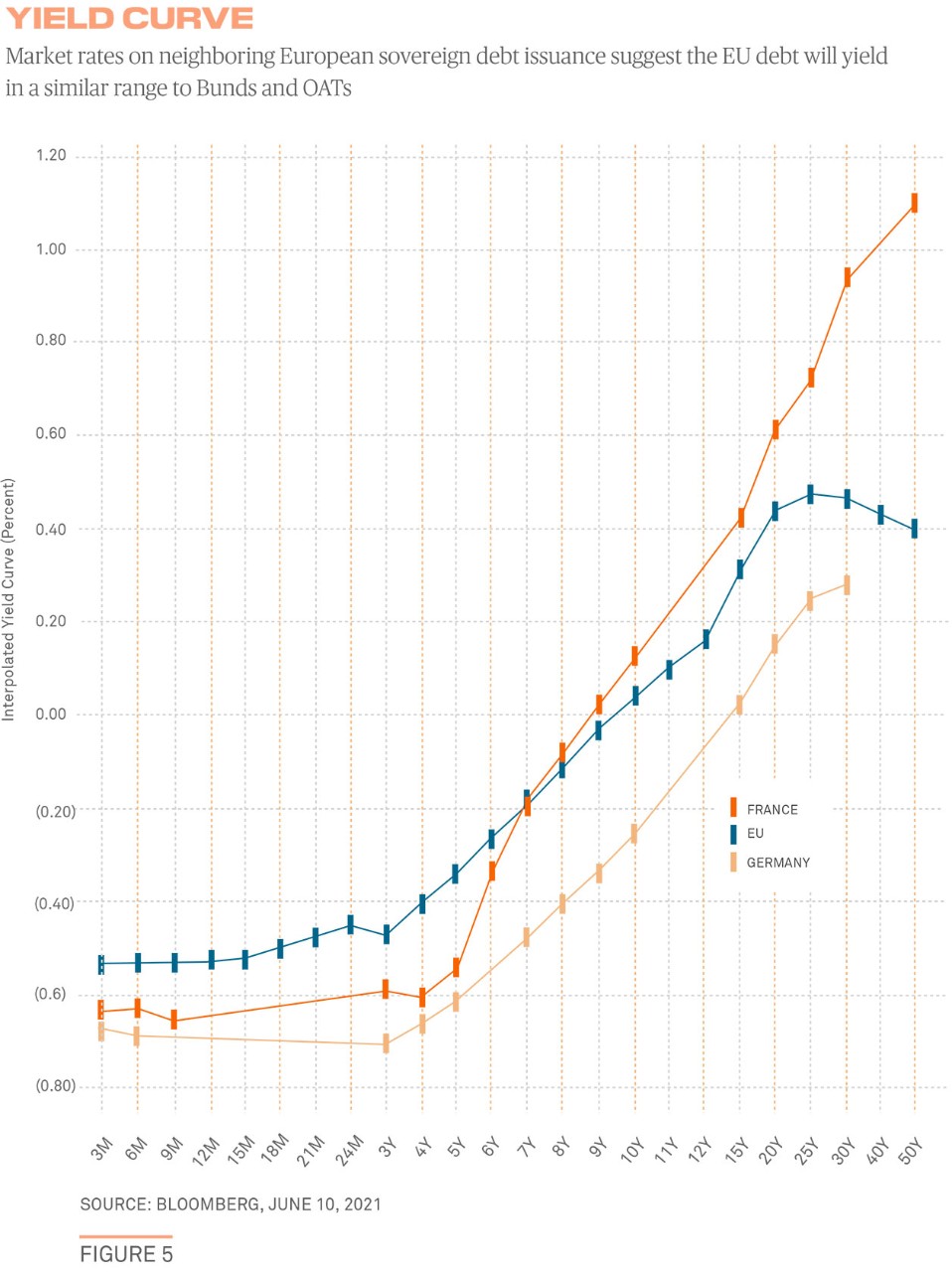

Crucially for investors, the EU has already established a yield curve through its borrowings to date (see Figure 3). Risk premiums on the SURE bonds have narrowed with each successive tranche, to the point where those yield spreads are now below that of France. In other words, it may be possible for the EU to raise funds more cheaply than the EU’s second largest economy.

Geoffrey Yu, senior EMEA Market Strategist at BNY Mellon, believes that investors who have historically been comfortable owning German Bunds will likely be comfortable owning bonds issued under the NGEU. “Given that the program should have a similar credit profile to previously issued and mutually guaranteed EU paper, such as ESM debt, spreads between NGEU bonds and Bunds should be similar,” he says (see Figure 5). For example, an ESM issue maturing in 2033 yields 21 basis points, a spread of 39 basis points over the 10-year German Bund.

Yu also believes that the sustainability element of the NGEU was deliberate. There is increasing pressure on investment managers to buy green bonds. “Reserve managers who want to diversify away from the U.S. dollar and also integrate environmental, social and governance strategies may welcome a large increase in the stock of jointly issued, and green, euro-denominated supranational assets,” he says.

The European Central Bank (ECB) also is widely expected to play a significant role as a participant. It will not itself buy NGEU bonds, but the national central banks of each member state that use the euro as their currency (the so-called euro area) will purchase them in the secondary market on behalf of the ECB.

Political Hurdles?

While the Commission has clearly done its homework with investors, politics may yet influence whether the NGEU can achieve long-term success.

The idea of the EU borrowing through a common debt instrument, with liabilities to be shared among member states as the NGEU envisages, has been around for decades. But it has always met resistance from wealthier member states that are net payers into the EU budget.

That’s because of domestic political resistance to the idea of backstopping an instrument with an implied mutualization of debt, regardless of the fiscal strength of participating member states. Germany has led opposition to the idea, with its economics minister as recently as March 2020 dismissing the idea as “a phantom debate.”

The economic and social crises sparked by the pandemic led to a stunning reversal in the German position last year, however. After lengthy talks between EU leaders, Germany’s Angela Merkel and France’s Emmanuel Macron threw their weight behind the idea of a rescue plan, funded by borrowing in the capital markets. Thus the €750 billion recovery fund, or NGEU, was born and has since been revised upwards to account for latest prices.

Kay Swinburne, vice chair of financial services at audit and consultancy firm KPMG, and a former Member of the European Parliament, says support for the NGEU grew with the pandemic. “People had been talking about this for decades and suddenly, European solidarity was more important than trying to protect your own national treasury. So the stars were aligned,” she explains.

Yet while this was a victory for advocates of an EU-wide borrowing exercise to fund the recovery, the initiative received a setback. In March 2021, a group of German eurosceptics — led by Bernd Lucke, an economics professor at the University of Hamburg and one of the founders of the right-wing Alternative für Deutschland (AfD) party — issued a lawsuit challenging the NGEU’s legality in a bid to stop the German parliament ratifying it. Member states ratified the NGEU in May, allowing the borrowing to move forward.

“Reserve managers...may welcome a large increase in the stock of jointly issued, and green, euro-denominated supranational assets.”

— Geoff Yu, BNY Mellon

A month later a constitutional court in Karlsruhe rejected a request for an injunction. But the court nevertheless conceded that the lawsuit was “not obviously without foundation,” a reminder of complications that could yet re-emerge.

Even though the Commission has made clear the NGEU is a “temporary instrument,” some richer EU member states remain skeptical of the idea of the bloc embarking on what they suspect might end up being an open-ended borrowing program.

An alliance of northern member states made up of Austria, Denmark, the Netherlands and Sweden — dubbed the “Frugal Four” — successfully negotiated a big reduction in the grant element of the NGEU.

“The Frugal Four will very much want to avoid this being seen as a ‘Hamiltonian moment’ that kicks off EU debt issuance forevermore,” says Ben Pott, Head of Public Policy and Government Affairs for EMEA at BNY Mellon, referring to the first U.S. Treasury secretary who helped to create the U.S. fiscal union. “There’s still this question: Is the genie out of the bottle on EU fiscal integration or is this [NGEU] borrowing just a sticking plaster for COVID-19?”

Much will depend on the outcome of elections in Germany in September. With Merkel set to retire, all eyes are on what political constellation will emerge. Her Christian Democratic Union (CDU) party faces a tough fight with the insurgent Green party, which some polling suggests could even take the chancellery.

Anna Rosenberg, Head of Europe and UK at Signum Global, a political risk consultancy, says that an emerging younger generation of politicians less wedded to the fiscal orthodoxy of Merkel and others is coming to the fore, meaning that there is likely to be continued support for the EU’s long-term borrowing program.

“The wind of change is sweeping through Germany. This new generation cares less about balanced budgets and debt, and the same applies to the public,” Rosenberg says. “I think there will be risks [to the NGEU] in the short term, but this will diminish over time.”

Repayment Risk

Arguably the biggest risk to the NGEU lies in ensuring that the billions raised are spent properly, that this is properly accounted for in a robust governance system. This is particularly important to investors who will be anxious to ensure that repayment risk — even outright fraud — does not jeopardize the NGEU in the decades up to the last scheduled repayment in 2058.

On the plus side, the Commission has received plaudits for engaging with with member states early on their plans for how the money will be spent. The team managing this, currently numbering about 100 staff members and located within the Commission’s Secretariat-General in Brussels, was set up in August right after the NGEU was approved.

“So far it seems to me they have handled it quite well,” says Eulalia Rubio, a Senior Research Fellow at the Jacques Delors Institute, a think tank based in Brussels. “They encouraged member states to discuss their plans with them very early. The result is that those being submitted are the product of long exchanges with the Commission, which has given it an enormous capacity to influence the plans.” Portugal in April became the first member state to submit a plan.

But Rubio also points out in a report she authored recently that with governments under pressure to spend the money quickly, there is a risk that money will not be allocated properly. The EU has set up a new body to deal with EU budget-related fraud, called the European Public Prosecutors Office (EPPO), which should help. There is some optimism that the green portion of the NGEU will also help. By tying a third of the funds to the EU’s wider green agenda — in particular a growth strategy unveiled in 2019 called The European Green Deal — a degree of accountability will be possible. “The Green Deal is undoubtedly one of the main tools they have to stamp conditionality on the funds,” says Signum’s Rosenberg.

“It strongly encourages governments to tackle key weaknesses that the crisis has exacerbated,” she says.

The ultimate test of NGEU may rest on whether investors will treat the EU as a borrower fully able to repay its obligations, as any equivalent sovereign borrower. EU borrowings are “direct and unconditional obligations” of the bloc, according to the Commission. The EU is legally bound by treaty to service EU debt.

Member states are required to repay NGEU loans to the EU, while grants will be repaid by the EU budget (see Figure 4). The Commission says that, “in the unlikely event of non-payment of a loan beneficiary, the EU budget guarantees that the EU timely honors its obligations.”

If any major country did default on the loan payments under the NGEU, that could “put a significant strain on the structure from a legal standpoint,” says Lee Buchheit, a veteran sovereign debt specialist. “But I think there will be buyers of these securities. In the end, it will be the investors’ decision, because they are the ones taking the credit risk.”

Jeremy Grant is a freelance writer based in London.

Questions or Comments?

Write to geoffrey.yu@bnymellon.com or reach out to your usual relationship manager.