Green Shoots for Africa

Green Shoots for Africa

March 2023

By Deborah Lynn Blumberg

Africa is set to benefit from new financial infrastructure that is designed to boost liquidity in its sovereign debt and attract private investment into its climate-linked bonds. Can it work for Africa and beyond?

For more than a decade, pockets of the fixed-income markets have been susceptible to sudden lurches that can send bond prices into free-fall, with buyers seemingly absent. The problem is especially evident in aging bonds and sparsely traded debt from developing markets.

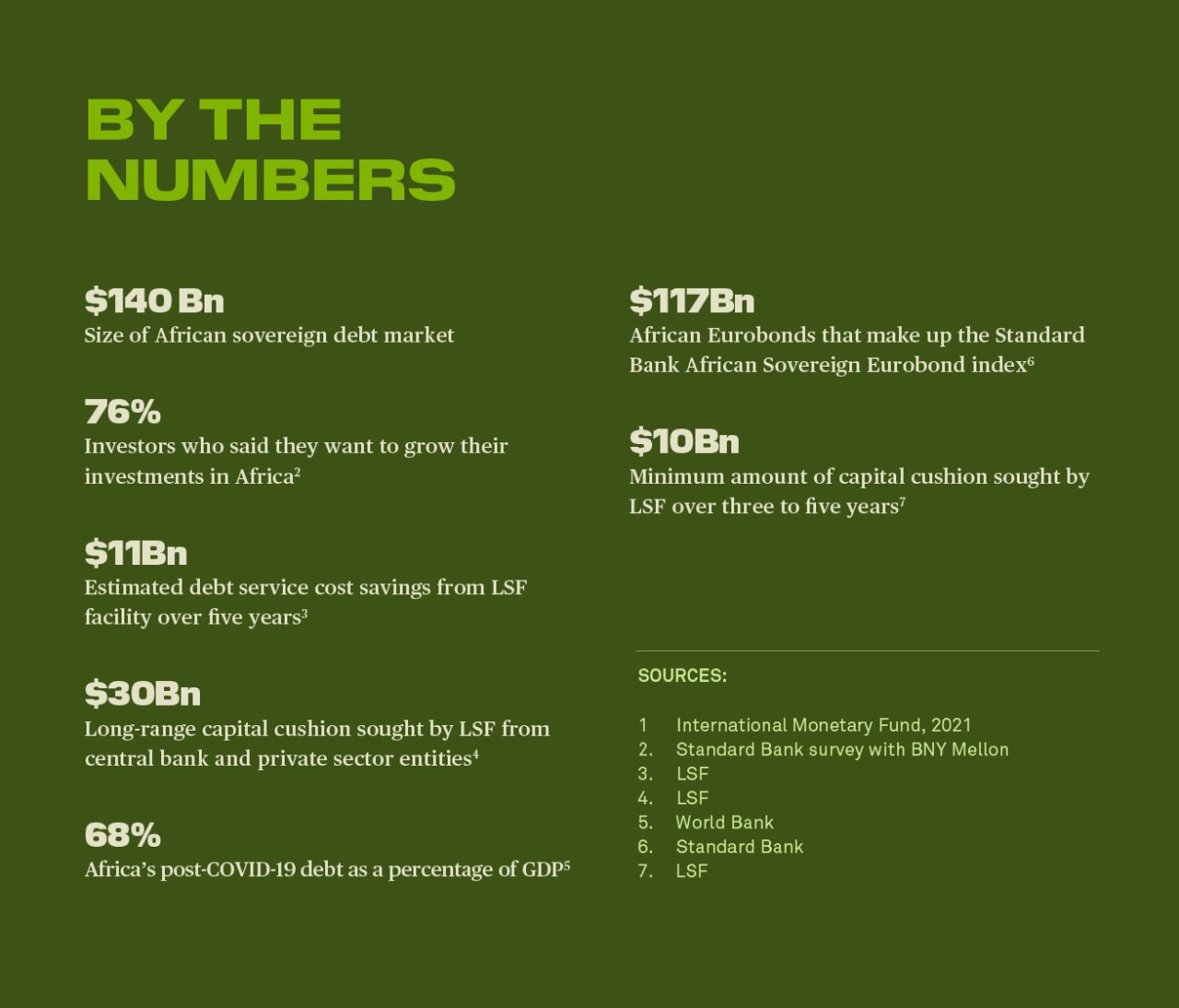

African sovereign nations—which together had originated more than $140 billion in international bonds as of 2021—now look set to become the inaugural beneficiary of a solution. The idea is essentially a recycling facility, which would enable the bonds to trade more frequently between asset owners, thereby reducing what the nations pay to carry the debt, at the same time as potentially financing Africa’s transition toward a net-zero future.

In early 2020 as the pandemic took hold, “We saw screens go blank and paper not trade and that had nothing to do with solvency,” recalls Jay Collins, vice chairman of banking, capital markets and advisory at Citigroup. “We realized we needed some new support structure or backstop for these markets.”

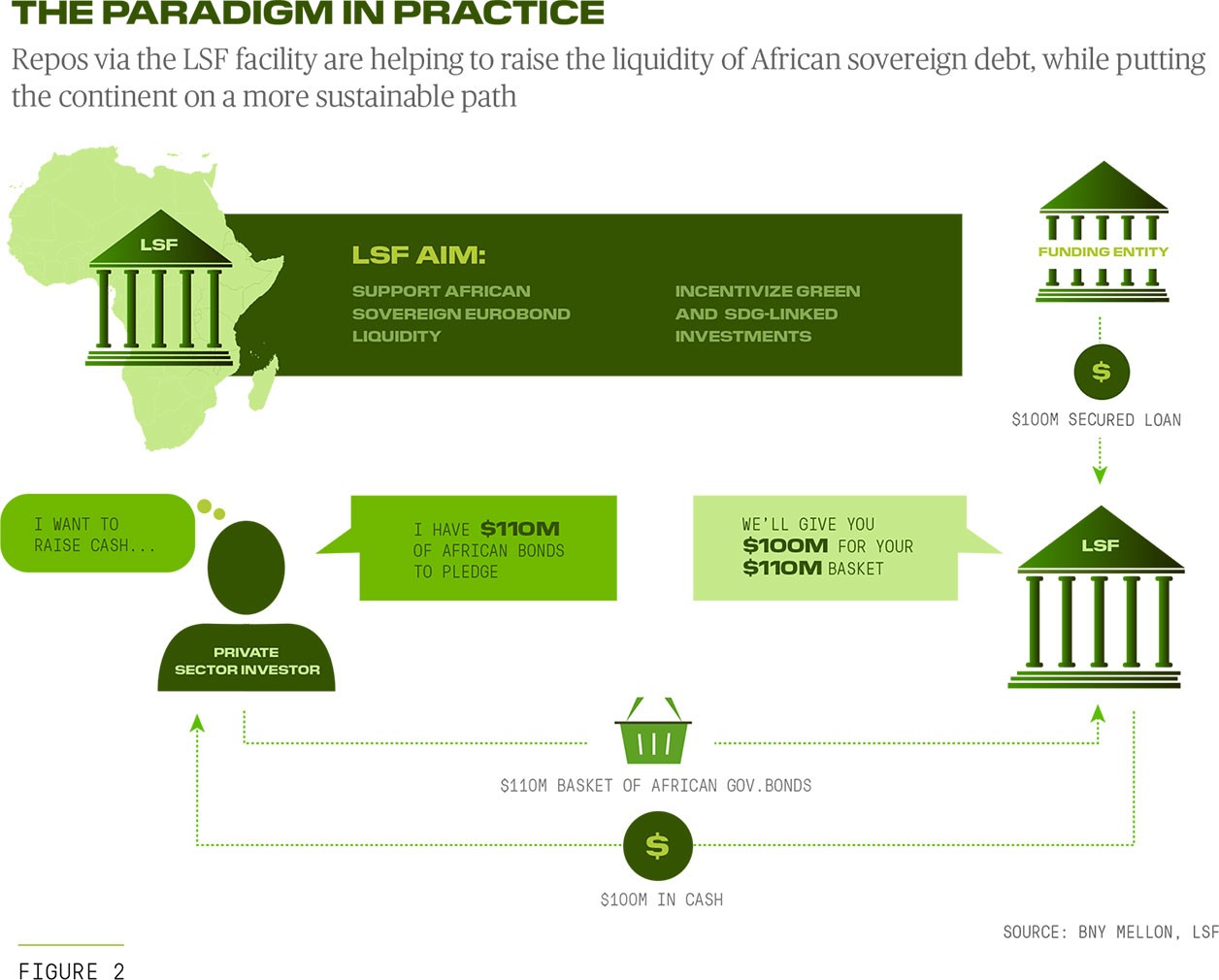

Several support mechanisms were proposed—both for Africa and other weakening emerging market economies. The so-called Liquidity and Sustainability Facility (LSF) for Africa was announced by the United Nations Economic Commission for Africa in November 2021 and saw its first test trade last year.

It is early days for the initiative, and official development finance institutions have not yet come to the table to help fund it. But central bankers around the world are watching with interest. Ultimately, the tool is seen as shining a light on Africa and heralding a more sophisticated financial marketplace there in the future.

Under Pressure

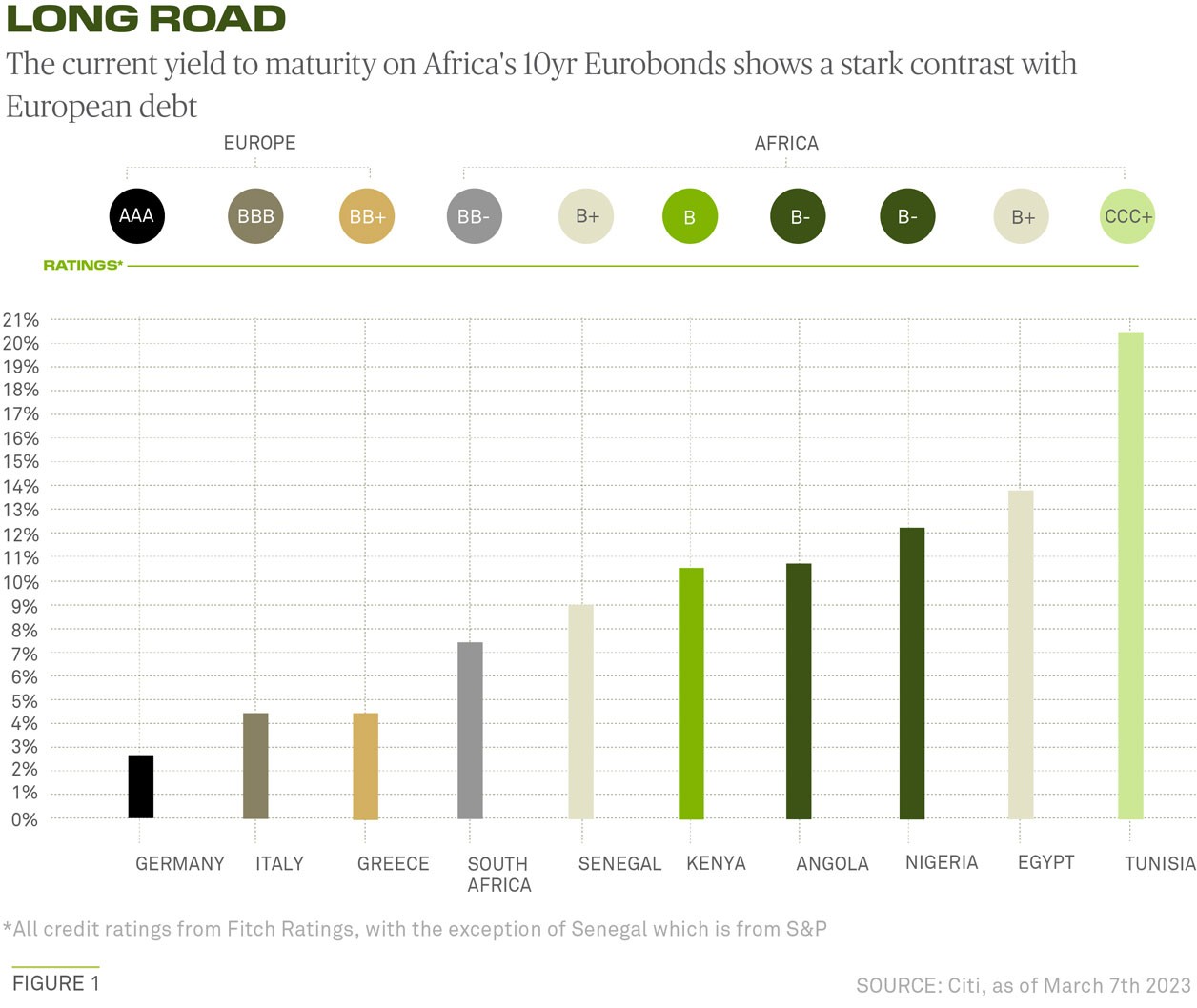

What preceded the facility was a perception problem. Long before Ghana suspended payments on its international “Eurobonds” and started restructuring its debt this past December, finance ministers were complaining that the country was paying unfair amounts to borrow.

“We see the problem every day and how it’s affecting the pricing of African bonds vis-a-vis other countries with near similar ratings,” says Dr. Benedict Okey Oramah, president of the export-import bank Afreximbank.

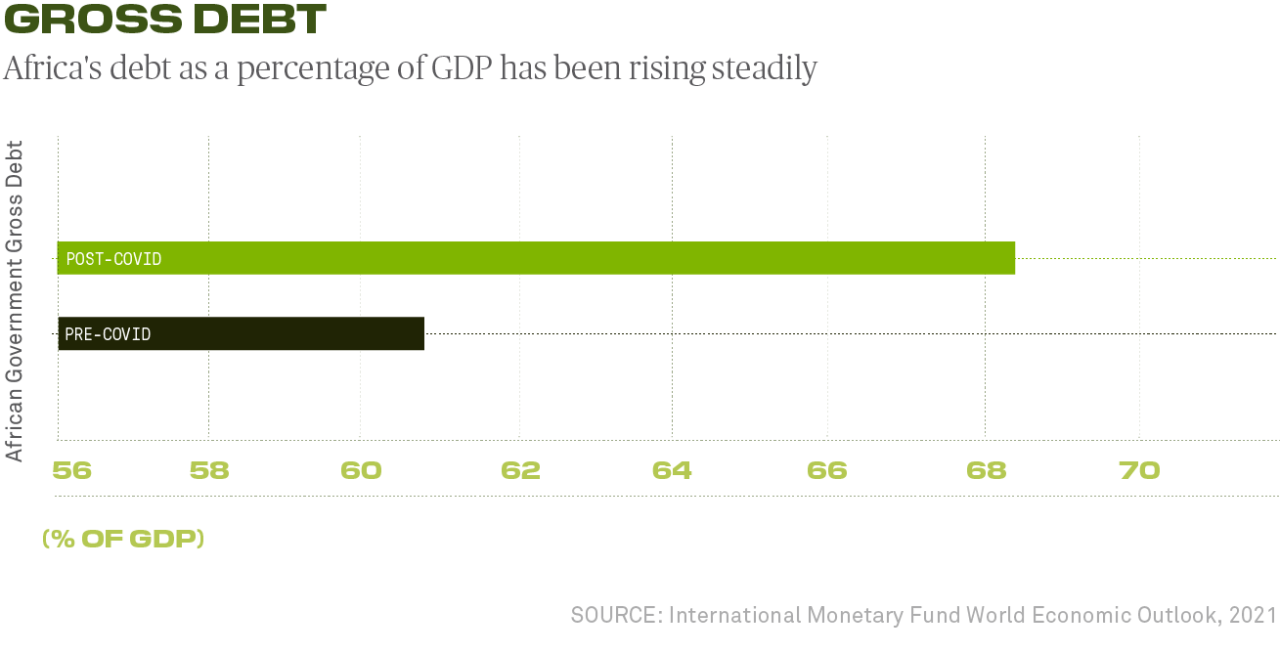

Despite improving macroeconomic fundamentals, the compounded effects of the pandemic, the global economic crisis and a steady drumbeat of negative rating agency reports have made for especially challenging financial conditions on the continent (see Figure 1).

Africa’s debt-to-GDP ratio rose to almost 70% from 2014 to 2021, according to the World Bank. This has heaped pressure on Africa’s bonds, including the $117 billion of Eurobonds that make up the Standard Bank African Sovereign Eurobond index.

The high cost of borrowing “makes us more vulnerable to exogenous shocks,” explains Ken Ofori-Atta, the finance minister of Ghana. “The result is a precipitation of macro instability, economic isolation and austerity without growth.”

On average, the 23 African nations that have access to the Eurobond market pay 170 to 290 basis points more to borrow on international markets than they should, relative to comparably rated sovereign issuers, according to estimates from Vera Songwe, a nonresident senior fellow in the Africa Growth Initiative at the Brookings Institution.

“This is one tool that can support systemic market functioning and reduce fragmentation in the liquidity of these African bonds.”

— BRIAN RUANE, BNY MELLON

For Africa, this is a major hurdle along the path to a post-COVID-19 recovery. It also presents a roadblock to continued, sustainable economic development in Africa and to the funding of large capital projects that can make progress toward tackling climate change on the continent.

Funding Gaps

In theory, demand for Africa-related investments is there. Some 76% of investors say they want to grow their investments on the continent, according to a recent survey by The Value Exchange, a market research firm, in partnership with BNY Mellon.

To step in, international investors need confidence. In the US and the European Union, for example, liquid bond markets mean private investors can post the bonds as collateral in exchange for cash in short-term trades called repurchase agreements or repos. Today, African bonds mostly sit idle in investor portfolios with only a small amount used as collateral in financing transactions, and only a tiny portion considered as eligible collateral, BNY Mellon data show.

Developed countries have cultivated stable repo markets for decades, and they serve as a crucial source of short-term funding for banks and broker dealers. The US repo market, for its part, provides in excess of $6 trillion of liquidity to the market, according to data from BNY Mellon, the Fed and Finadium.

While a modest over-the-counter repo market does already exist for some African nations, a mature repo market that could serve as the foundation for its financial systems and help open up new markets has been missing, until now, according to the head of the LSF, David Escoffier. “We’re trying to rebalance global markets by creating an infrastructure that will make investing by global investors easier,” he says. “This initiative is sustainable; it’s a long-term infrastructure platform that will really make a difference for African markets.”

Ultimately, the hopes for the LSF are both high and ambitious: deeper repo markets could help African countries to save up to an estimated $11 billion on their borrowing costs over five years, according to people who saw estimates from investment manager PIMCO. A spokeswoman for the asset manager declined to comment.

Building Blocks

The idea for the LSF took hold in the spring of 2020 when Songwe was serving as Executive Secretary of the United Nations Economic Commission for Africa (UNECA). Believing that Africa could benefit from first-world financial market infrastructure, she penned an article in the Financial Times about what she described as the “stubbornly sticky perceptions” about Africa.

The piece caught the eye of Escoffier, then a partner at the London-based consultancy Eighteen East Capital. He phoned Songwe and together they contacted a range of global central bankers, commercial banks and finance ministers to pitch in.

The LSF takes collateral in the form of African Eurobonds and then provides short-term financing against them, taking a “haircut” or discount ranging from 10% to 30% depending on the quality of the collateral in the basket.

“For the recovery of Africa to be successful it has to be green.”

— DAVID ESCOFFIER, LSF

Currently, the facility can cater to more than 120 African sovereign Eurobonds, supporting liquidity in those securities and incentivizing potential investments in green African bonds, too. In time, once the market has sufficiently matured, the LSF team's vision is to make it a form of contingency facility in times of financial stress, akin to the US and the guarantees the Fed offers with its repos.

Setting up the facility required collaboration with key industry partners. Songwe and Escoffier turned to BNY Mellon to facilitate the settlements and service the trades. The bank already services around $5 trillion in daily financing trades and runs the repo infrastructure for the Fed in the U.S.

“Our role is to be the platform, tech provider and industry expert on collateral,” says Brian Ruane, CEO of BNY Mellon’s Clearance & Collateral Management business. “This is one tool that can support systemic market functioning and reduce fragmentation in the liquidity of these African bonds.”

Law firm White & Case worked pro bono advising the LSF from 2021 and helping to standardize onboarding and transaction documentation for its participants. Nearly 50 of the firm’s lawyers across nine offices advised on the LSF’s inaugural trade.

Garnering Interest

Finally, two friendly institutions came together to make the first deal. Announced at the 2022 UN Climate Change conference, Citi extended a diversified basket of sovereign Eurobonds, including Egypt, Kenya and Angola bonds, to the LSF and the LSF borrowed $100 million from Afreximbank to pass cash back to Citi (see Figure 2). The trade was unwound at the end of last year and there are discussions about other institutions replicating the trade.

The LSF is now in the process of signing on additional users, including potentially two of the largest American and European fixed income investors, according to White & Case. “While the LSF will not necessarily have a direct influence on borrowing costs for African countries, we believe that the enhancement of liquidity in the market will act as an extra buffer to credit risk, which remains a key determinant of the borrowing costs,” says Vincent Mortier, CIO of Amundi, which was one of the first asset managers to begin onboarding. Escoffier also cites interest from other large global investors and African central bank governors.

For initial operational funding, the LSF is taking out a $1.5 million loan from Afreximbank. Afreximbank is also extending a $500,000 grant to the LSF. But to be successful going forward, the LSF needs a financial cushion or a surplus of cash to fund future transactions. Its leaders continue to engage with central bankers, both in Africa and outside, whose reserves could help.

A solid start would be a $10 billion cushion over the next three to five years, Songwe says. The LSF’s optimal funding capacity is estimated to be at $30 billion over the medium term (equivalent to 20% of Africa’s Eurobonds) with around 20 counterparties.

Seeing Green

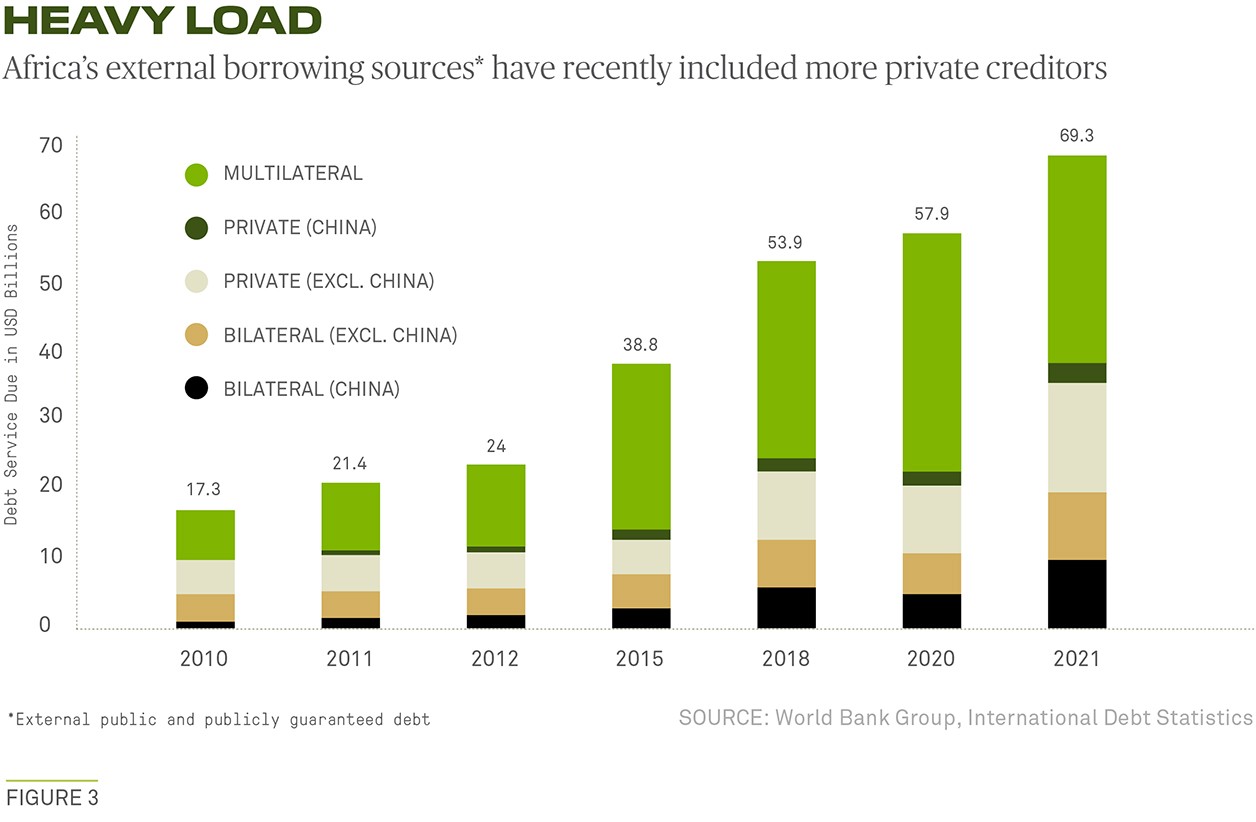

The LSF is seen as driving appetite for African green bonds, too, at a time when the continent’s external borrowing has become more dependent on private creditors (see Figure 3). While Africa is responsible for only 2-4% of global greenhouse gas emissions, it is among the most vulnerable to climate change and international aid is insufficient, says Jean-Paul Adam, Director for Technology, Climate Change and Natural Resources Management in the United Nations Economic Commission for Africa (UNECA).

The share of sustainability-linked bonds issued in Africa and the Middle East currently accounts for less than 1% of the total global amount, according to the LSF.

“Africa is really left behind,” says Adam. “We need to leverage private sector investment to solve climate change. The gaps are huge, but that also means the opportunities are huge.” Africa could potentially be the largest generator of photovoltaic power, according to Escoffier, who notes, “For the recovery of Africa to be successful, it has to be green.”

A related hope is that the LSF will open the flood gates to other financial markets on the continent, ultimately leading to robust exchange-traded fund (ETF) and retail financial markets as well as a wider range of investment products not before seen in Africa.

Citi says the LSF was originally envisaged as a solution not just for Africa, but for a range of struggling economies whose bonds need structural support in today’s fragmented global capital markets. Oramah cites interest in the facility eventually expanding to other developing countries, including in the Middle East, whose non-African sovereign bonds could benefit from the facility.

“This is as applicable outside of Africa as it is to Africa,” Collins says. “If there’s interest among the institutional community to talk about this outside Africa, I would say it’s an idea worth discussing.”

Deborah Lynn Blumberg is a former Wall Street Journal writer based in the Washington D.C.-area.

Questions or Comments?

Write to Alexander.Mount@bnymellon.com or reach out to your usual relationship manager.