The Inconvenient Truth About ESG

The ESG movement has matured, but still faces concerns about non-standardized data

The Inconvenient Truth About ESG

The ESG movement has matured, but still faces concerns about non-standardized data

May 2020

By Imogen Rose Smith

The ESG movement has grown, but so has anxiety about greenwashing. While the funds appear to be surviving COVID-19 and are here for the long haul, they need common standards to better demonstrate what they’re invested in.

Even before COVID-19 exposed the importance of public health policies to investments, there were reasons to think about environmental, social responsibility and corporate governance (ESG) issues when making investment decisions.

There were Australia’s wildfires, which have cost that country billions of dollars; calls for companies to include more women on their boards; and the WeWork IPO that wasn’t, an alleged governance failure that slashed the market capitalization of a much-hyped unicorn.

Investors are growing more attuned to these factors than ever before, and many funds consider them a strategic hook. Almost every major asset manager now offers an ESG strategy, and, until the pandemic shuttered the global economy in March, new financial products were launching by the month. The narrative is not just showing up in equity portfolios. It is also entering fixed-income markets and even money market funds.

At the same time, the broader adoption is bringing about new questions and challenges about analytics and reporting tools covering the now $30 trillion global sustainable investment industry. Matt Orsagh, Senior Director of Capital Markets Policy at the CFA Institute, says he has met with professional and institutional investors around the world about ESG integration as part of a collaboration with the Principles for Responsible Investment, a UK-based industry group. He says many investors were confused about what the ESG label really stands for.

“There was one concern we heard everywhere we went: that there is no agreed-upon definition of what ESG means, so funds may be marketing something that may not be in line with what a client wants,” Orsagh notes. “Investors have to do their own homework to know if something that is labeled ESG is really right for them.”

Anxiety is especially high about a practice known as “greenwashing,” where an investment or company claims to be environmentally friendly but may not be. The field of “impact investing” also is causing concern. While it involves investors changing the environmental and social impact that their capital is having, some worry good impacts may come at the cost of economic gains, or that managers will cherry-pick impacts to show only what is good.

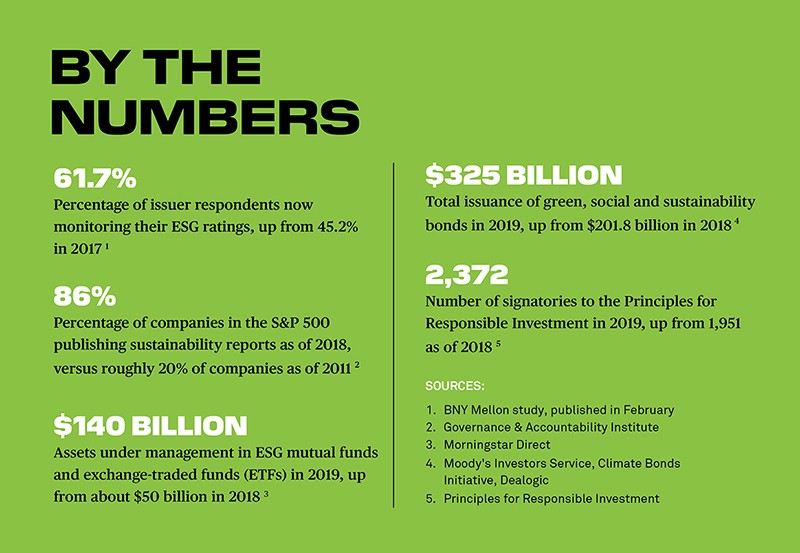

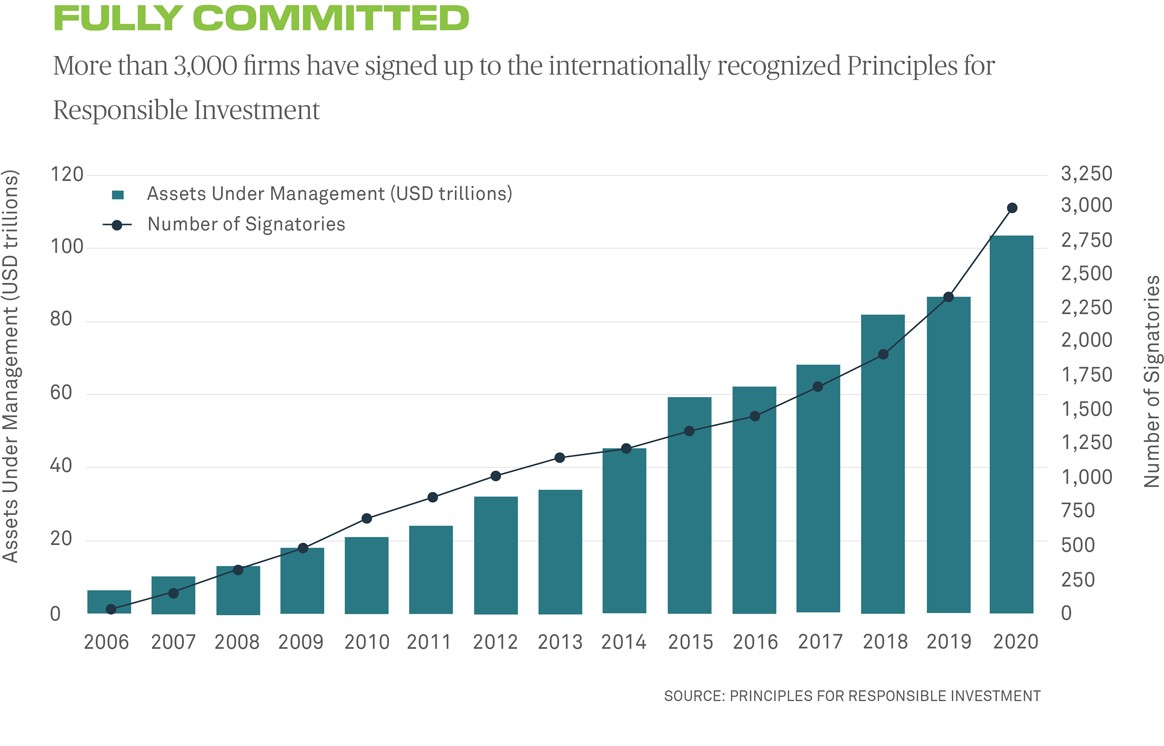

It is difficult for investors to understand how to value a company’s ESG standing, when opinions among data vendors and ratings firms can vary so widely. At BNY Mellon, which is helping the industry to develop common standards by mapping investor preferences to ESG fund holdings, a study published in February found 61.7% of issuer respondents now monitor their ESG ratings, up from 45.2% in 2017.

Without substantial improvements, better disclosure and higher quality information from the more than 250 data vendors in the space, the entire ESG movement runs the risk of returning to a momentary marketing fad, say some experts in the field. The US Securities and Exchange Commission is reportedly probing the validity of ESG funds and what investments are inside them.

“There is no agreed upon definition of what ESG means, so funds may be marketing something that may not be in line with what a client wants.”

— MATT ORSAGH, CFA INSTITUTE

In October, the European Union passed ESG disclosure regulation requiring funds to explain how they consider sustainability factors that materially affect their investments.

A new EU taxonomy for ESG finalized earlier in the year also aims to coordinate standardization across member states, and sets out a series of criteria to determine whether the activity being financed has a sustainability component.

Here to Stay

Another concern is whether investors will continue to pursue these strategies as the economy tries to recover from the current pandemic. Some early indications seem to suggest ESG funds may have outperformed non-ESG strategies during the crisis.

Natalie Westerbarkey, Head of EU Public Policy at Fidelity International, says one of her priorities is making sure the firm still continues its green agenda during and after the pandemic. Since 2019, “All [the firm’s] analysts must look at ESG aspects and have a view on them,” she says. “We already have data points that ESG seems to be outperforming other types of usual assets, especially in downturns.”

In their flight to safety, however, investors may go back to focusing on core tenets of their business for a while. Some who embraced ESG as a marketing gimmick during the decade-long bull market may lose their enthusiasm for the movement. But most experts agree ESG is here to stay.

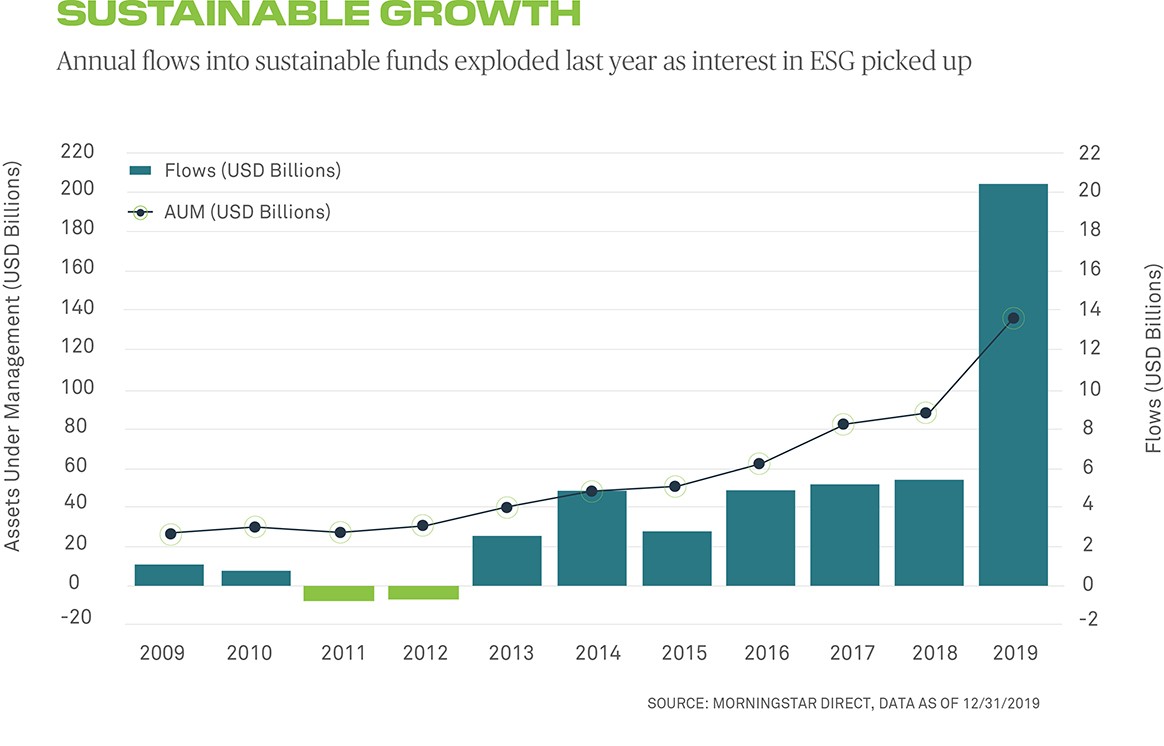

Before COVID-19, fund flows into ESG were nothing short of staggering. Last year, the industry added $21 billion to ESG mutual funds and exchangetraded funds (ETFs), according to fund tracker Morningstar, bringing the total assets under management to about $140 billion. In 2010, total net flows were less than $10 billion.

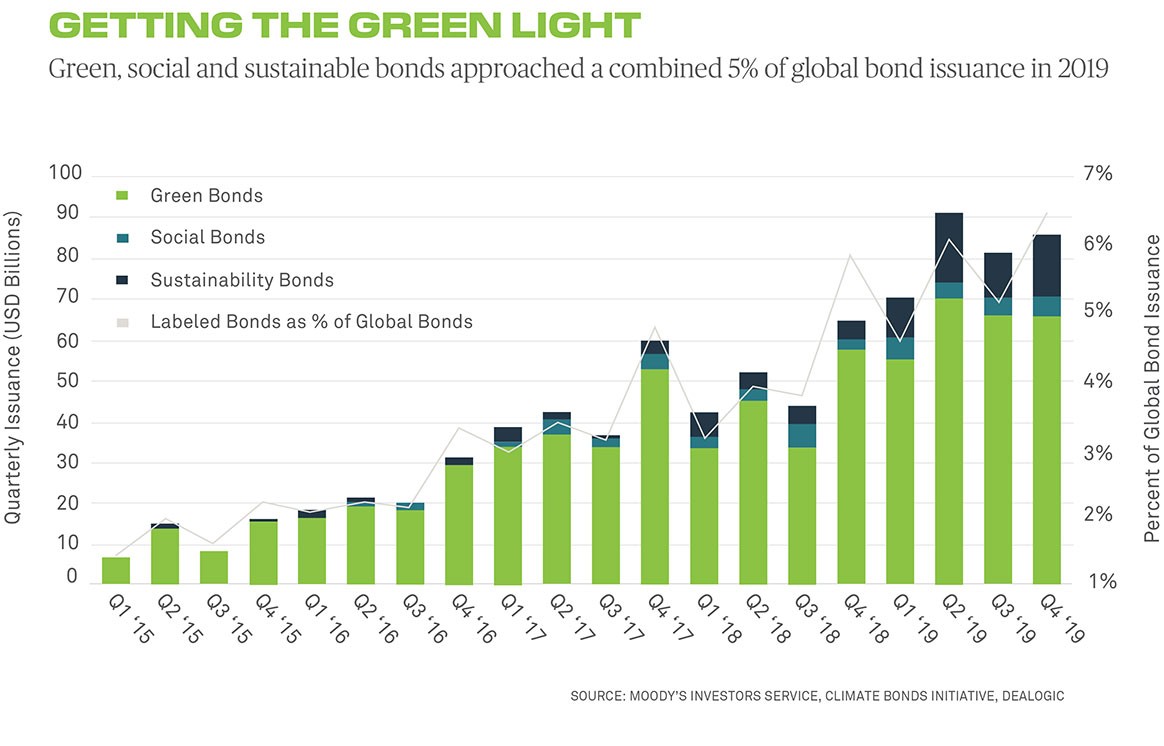

US-domiciled assets using sustainable investing strategies totaled $12 trillion as of 2018, up 38% from 2016 levels, according to the Global Sustainable Investment Alliance. Meanwhile, green, social and sustainability bond issuance reached around $325 billion in 2019, according to Moody’s Investors Service.

The inflows have lit a fire under an investment management industry that is already struggling to justify its fees at a time of increased passive investing. After US money manager Federated Investors acquired European ESG specialist Hermes Fund Managers in 2018, it changed its name to Federated Hermes out of a belief that responsible investing was the future.

Asset managers also see an opportunity to attract millennials — both as investors and employees. “The values of a new generation are beginning to influence how companies and investors think,” says Joshua Kendall, Senior ESG Analyst with BNY Mellon’s asset management subsid iary. “This change empowers millennials.”

Public pension plans, sovereign wealth funds and other institutional asset owners are increasingly including ESG in their investment processes. The US investment industry does have a long, sustainable investment history. But it was the European institutional investors, particularly the Scandinavian funds, along with some pension funds in Australia and New Zealand, who in the 2000s began loudly voicing their sustainable investment concerns.

Over time, ESG investment evolved. It started with the exclusion of companies perceived to have questionable ethics, such as tobacco stocks or firearms. Today, the idea is to identify companies perceived to have positive, sustainable business practices, which investors believe will outperform.

As ESG entered the investment office, however, the challenge of identifying a high-scoring and potentially economically successful company became exponentially greater. How to value a company’s ESG standing, when opinions could vary so widely and reliable data were often hard to come by, was a dilemma facing every investor.

“We already have data points that ESG seems to be outperforming other types of usual assets, especially in downturns. ”

— NATALIE WESTERBARKEY, FIDELITY INTERNATIONAL

Marcelo Jordan, Senior Portfolio Manager for ESG at the $25 billion World Bank Pension Plan, says some of his fund’s best performing stocks have been companies where an activist manager has built a large shareholding and driven change from within. Whereas an ESG policy used to be about ethical rather than financial decisions, he said nowadays people have started “talking about sus tainable investment and long-termism in the context of financial objectives and fiduciary responsibilities.”

Views on ESG also have matured, although opinions about climate change vary dramatically by region. While climate change has long been a focus for investors in Europe, many developing market countries prioritize social issues when it comes to ESG. Institutional investors in Japan have recently begun to prioritize climate change. But in the US, many investors still view climate change as a political issue and subject to debate.

Too Big to Fail

One of the biggest questions for ESG investing pioneers right now is, will the pandemic help or hinder the ESG movement?

On the one hand, COVID-19 has strengthened the case for ESG investment. It has exposed societal divergence, such as how case numbers of the virus exploded in lower-income areas across New York City. The economic slowdown has also drawn attention to climate change and the impact of the industrial economy on the environment.

Some practitioners are expecting a greater demand for ESG products, so much so that some think there may be genuine risk of ESG becoming a bubble, if the supply of investment products cannot rise to meet potential demand.

On the other hand, investors have to focus on their core strategies to make up for losses that hit their portfolios in February and March. The global financial crisis was also a game-changer for ESG. In the four years after 2008, net fund flows into US ESG mutual funds and ETFs averaged just $136 million, according to Morningstar, and fund flows were negative in 2011 and 2012.

What preceded COVID-19 was a clear desire among industry participants to innovate within the ESG field. Over the last couple of years, more and more strategies that represent the “plumbing” underneath markets — from money market funds to securities lending — have embraced ESG. Some money market funds are being re- versioned into impact investing funds, allowing companies to stash cash in overnight investments that fulfill their ESG mandates.

In November, Dreyfus transformed its Dreyfus Government Securities Cash Management Fund into an impact investment fund. As of April 30, about 58% of the fund’s trading was conducted with broker dealers run or owned by women, minorities, LGBTQ or service-disabled veterans.

Similarly, Goldman Sachs Asset Management (GSAM) recently repositioned one of its government money market funds to include a focus on diversity and inclusion, and through March 31, about 70.9% of the fund’s purchases were conducted with women, minority or veteran-owned broker dealers.

“We integrate ESG considerations into our investment process because we believe it contributes to improved performance,” said Michael Kashani, GSAM Fixed Income’s Global Head of ESG Portfolio Management.

Even the market for collateralized loan obligations (CLOs) has seen a recent influx of ESG strategies. Quantitative hedge fund firms are expressing interest in ESG strategies and the number of ESG index products has proliferated, with everything from start-ups to the largest asset management firms getting in on the act.

There is an “inconsistent understanding of the opportunity and risk, but the tipping point has come, so there is more focus on active investment and positive search for ESG analysis,” says Frances Barney, Head of Global Risk Solutions for BNY Mellon Asset Servicing.

Data Challenges

Even so, if ESG is to be a long-lasting consideration, it needs to address the problems of its early success, namely the variety and unreliability of its data and definitions.

Jason Mitchell , Co-Head of Responsible Investment at alterative investment manager Man Group in London, overseeing $104.2 billion, says his team has been using data from numerous providers and reworking it in order to produce the firm’s own ESG factors for its in-house algorithms.

He says there are lots of reasons to be skeptical. Given the relatively short track record for much of the information (less than a decade) and the fact that many data issues still persist, Mitchell cannot definitively say that the ESG factors are a source of alpha, but the firm has seen some positive signals. “It’s only pervasive for the time we have confidence in the data, which is about seven and a half years,” he said.

Gert-Jan Sikking, Senior Advisor for Responsible Investing at the $283 billion Dutch pension fund PGGM, says his firm also does its own analysis of data vendors to determine which offer the most valuable information. For now, PGGM is doing a lot of its own work on the impact of companies and their investments, encouraging companies and vendors to provide more accurate and detailed reports.

More improvements can also be made by corporations. Many large publicly traded companies produce a glossy corporate sustainability report, and many voluntarily disclose information such as their carbon footprint. But with exceptions — such as a regulatory requirement — ESG disclosure is mostly voluntary, so there can be little to no consequence to providing inaccurate information.

“Given the spectrum of ESG issues investors care about, and the diversity of data sources available, the ability to look through them with crowd-sourced feedback — that is unique. ”

— CORINNE NEALE, BNY MELLON

“The data could be more focused on material issues, measured with greater accuracy to make the proper investment decisions,” notes Dr. Jeroen Derwall, Assistant Professor of Finance at Maastricht University and Co-Founder of the European Center for Sustainable Finance.

In response to these data challenges, BNY Mellon is launching a business application in June, with input from clients, which helps clients to customize investments to their individual ESG preferences. Side benefits of the tool include: helping to prove to regulators and end investors that their portfolios meet their desired criteria, and crowd-sourced feedback loops, which may help inform broad standards around what investors consider to be green or sustainable.

“Given the spectrum of ESG issues investors care about, and the diversity of data sources available, the ability to look through them with crowd-sourced feedback — that is unique,” said Corinne Neale, Global Head of Data and Analytics Business Applications for BNY Mellon.

Recently, regulators have been expressing more interest in ESG. They may decide to narrowly define what an ESG fund is. But Andrew Parry, Head of Sustainable Investment at Newton Investment Management, argues that would be a mistake. Instead, he suggests, companies need to, and will, improve.

New attitudes are coming into the industry all the time. “We are probably going to be coming up to a generational shift in leadership on corporate boards,” says Parry. “If there was better and more standardized mandatory reporting of ESG issues at the corporate level, that would be a lot easier.”

Imogen Rose Smith is a freelance writer in New York.

Questions or Comments?

Write to Frances Barney in BNY Mellon Asset Servicing, Charles Goodwin in BNY Mellon Markets, or reach out to your usual relationship manager.