The Challenges of Losing Libor

Benchmark Reform

The Challenges of Losing Libor

Benchmark Reform

July 2019

By Oliver Bader

Within three years’ time, an interest-rate benchmark that became infamous in the aftermath of the global financial crisis could disappear from the markets for good.

Replacing the London Interbank Offered Rate or “LIBOR” has become a Wall Street priority and global regulators are keen to consign it to the dustbin of history, after a host of banks were accused of manipulating the rate.

But moving over won’t be easy, even with what appears to be a lengthy runway. LIBOR is the basis for pricing hundreds of trillions of dollars of financial instruments, including everything from complex derivatives and commercial loans to home mortgages. As such, it is about as intrinsic to financial markets as train tracks are to railway transportation.

Industry working groups in conjunction with regulators at the Bank of England and the Federal Reserve have been busy determining some alternatives. These vary by structure and region, bringing nuances to the transition. Further complicating the matter is the fact that it appears the switch will happen at different times for different financial instruments in different ways.

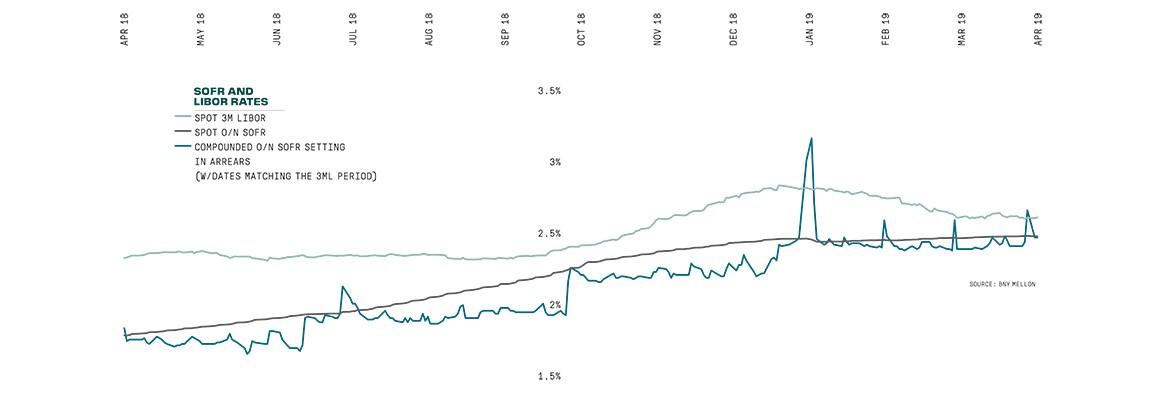

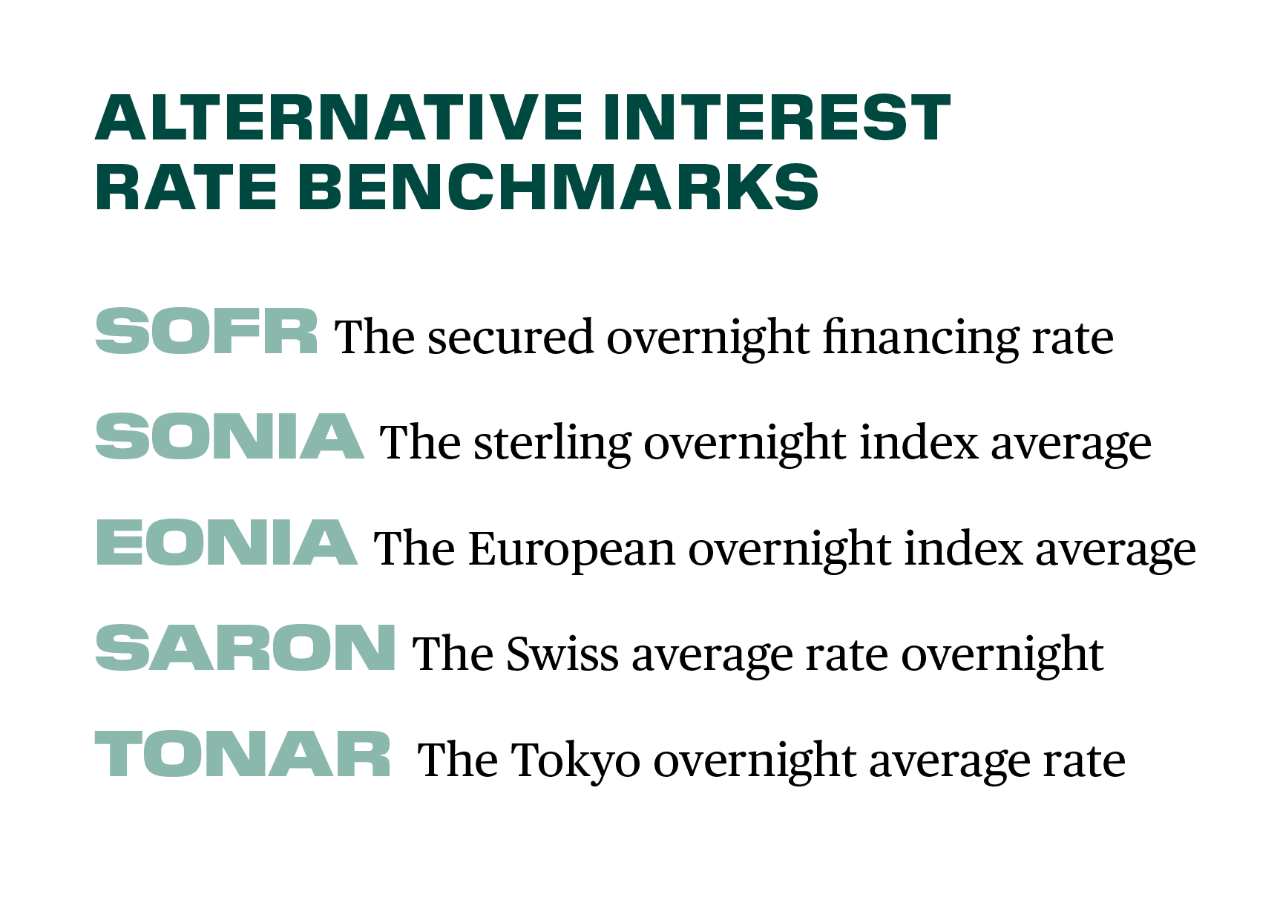

The suggested US dollar replacement, called the Secured Overnight Financing Rate or “SOFR,” was recommended in 2017 by the Fed-sponsored Alternative Reference Rates Committee (ARRC) and introduced in April 2018. Unlike LIBOR, which has a ‘term’ component for setting interest rates one, three, six or 12 months out, the new SOFR rate is an overnight rate.

Historically, USD LIBOR has been based on uncollateralized transactions and taken from a diminishing number of observable transactions. By contrast, SOFR is expected to behave differently because it is based on a larger volume of underlying, secured trades.

Regulators are now pushing the industry to move away from LIBOR, feeling it lacks robustness because expert judgement is too often required in the absence of underlying transactions. There is a risk it becomes unstable if it lingers on after the alternatives are in place and some believe banks may decide to stop quoting LIBOR, once they are no longer required to help set the benchmark after 2021 by the UK’s Financial Conduct Authority.

Trading and issuance are “already happening and building momentum, and given the regulatory stance, we think those things will come together,” says Adam Gilbert, regulatory leader at PwC financial services advisory. “Will there be vestiges of LIBOR that stick around? That’s quite possible but we think it’s the exception.”

Act Now

While SOFR is based on more than $800 billion of underlying short-term loans every day, trading volumes in products like derivatives, loans and securities indexed to the new SOFR rate are still in their relative infancy. Conversely, LIBOR is the other way around. It’s based on only about $500 million of daily trades but there are an estimated $350 trillion in loans and derivatives linked to it - $150 trillion in Europe and Japan and $200 trillion in the US.

Industry experts say that, with the clock ticking and the transition likely to accelerate soon, market participants with exposure to LIBOR need to get ready. In the US, the Fed-sponsored ARRC group set out a “paced transition plan” to sequence the adoption of SOFR. This contemplates derivatives—both on and off exchange—and the creation of a forward-looking rate for loans, bonds and mortgages.

The Securities and Exchange Commission said in a July 11 statement that it would monitor which risks and exposures companies might need to disclose in relation to the transition and “whether the adoption of a variety of replacement rates for USD LIBOR instead of a dominant successor could limit the effectiveness of all replacement benchmarks.”

In the near term, a key focus will be analyzing areas of exposure to LIBOR not just across trading, but across risk, finance, operations, legal and technology groups. That review involves not just collecting all the physical documentation supporting financial contracts, but also looking across the different types of clients using them.

“Will there be vestiges of LIBOR that stick around? That’s quite possible but we think it’s the exception. ”

— ADAM GILBERT, PWC

Depending on the institution and the resources available, this is where the pinch points will likely occur.

“This is likely to be a series of massive corporate actions,” says John Nixon, director of derivatives operations at BNY Mellon. “You have to be able to support it on billions of dollars of varying types of instruments and evidence that transition internally and to clients or counterparties.”

Like every other bank, BNY Mellon set up a program to analyze the potential impact, appointing an enterprise-wide LIBOR “czar” overseeing a taskforce to identify every affected legal contract. The bank has already executed SOFR swaps and futures as well as both underwritten and made markets in SOFR floating-rate notes for clients.

“The change will be seismic but the good news is we have already quantified our market exposure and we’re ready to trade,” says Robert Lynch, head of interest rates trading at BNY Mellon Capital Markets, LLC.

The biggest burden will inevitably fall on the smallest accounts and thousands of wealth managers and asset managers that do not have the bandwidth or quants available to help them make the switch to the new overnight rates, say industry experts.

The changes could ripple far and wide, and not only in bond and derivatives contracts. The mortgage market, with millions of commercial borrowers whose interest rates set off LIBOR, will suddenly find itself operating under a new paradigm.

Fallback Language

In case LIBOR stops being quoted and falls away, regulators have been helping to coordinate the construction of recommended new legal language, known as ‘fallback’ provisions,” as a sort of insurance policy to be written into future and legacy products.

Current fallbacks govern what might happen if there were a temporary cessation in existing benchmarks. The goal of the new language is to create contract certainty in case of any permanent cessation in any new or existing benchmarks and to keep any change in contract values to a minimum. The ARRC in April released recommended fallback language for U.S. dollar Libor floating-rate notes and syndicated loans, and more in May for business loans and securitizations.

A good portion of the work to transition derivatives pricing will be done at utilities called clearinghouses that process many of the trades, such as LCH – a large clearinghouse for interest-rate swaps and other instruments that rely on LIBOR and other benchmarks.

The London Stock Exchange Group, the majority owner of LCH, has already done some of the preparation work. That includes listing SOFR swaps as eligible for clearing; helping the benchmark reform process in the U.K. with its Sterling Overnight Index Average or “SONIA” rate; and assisting in the switch to the Swiss Average Rate Overnight, or “SARON.”

LCH says it will focus on bringing a Euro Short-Term Rate, known as “ESTER,” to the clearinghouse later this year, and encourage participants to start speaking with utility providers to help ease the transition process away from LIBOR.

“Many clients are well advanced with their planning, but we would encourage them to engage now with the system providers and infrastructures they rely on so as to ensure they understand what’s changing and when, and remain able to manage their business activity through the program of change that lies ahead,” says Phil Whitehurst, head of service development for rates at LCH in London.

The International Swaps and Derivatives Association (ISDA) is amending standardized swap contracts to fit the new benchmarks and LCH has said it is working on a mechanism to switch any transactions still referencing LIBOR once that work is complete, starting in 2020.

“The change will be seismic but the good news is we have already quantified our market exposure and we’re ready to trade.”

— ROBERT LYNCH, BNY MELLON

When ISDA canvassed the marketplace about suggested fallback language in July, 2018, a majority of derivatives market participants opted for backward-looking term rates in the theory it would reduce the risk of rate rigging.

Meanwhile, market participants want a forward-looking interest-rate term benchmark for non-cleared swaps, loans, bonds and mortgages. So far, there is no such thing and any forward-looking rate would have to be assembled out of derivatives tracking the new overnight benchmarks. It isn’t clear when sufficient volumes will allow for this to happen.

Treasurers would like the replacements for different instruments to align so that a hedging mismatch is not created between assets and liabilities should a cash product, like a bond, fall back to one rate and the derivative used to hedge it fall back on another. This would create a headache for participants called “basis risk,” where trades are no longer paired.

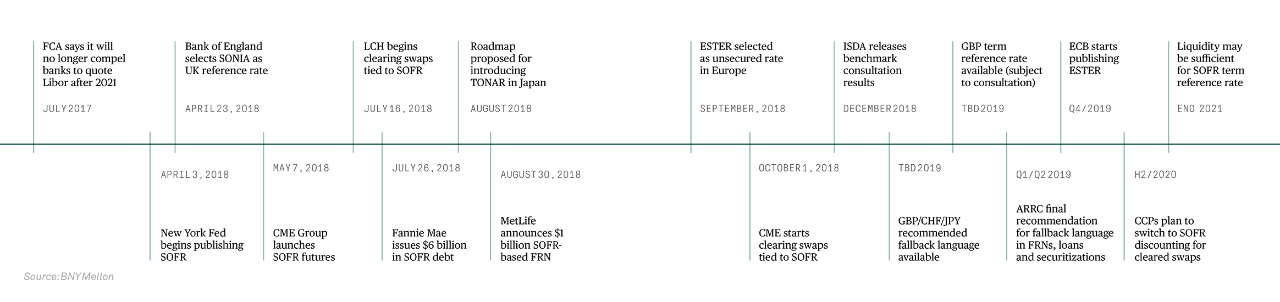

Key Transition Dates

“The key is how the cash market synchronizes with the derivatives market,” says Rob Wilson, head of change at BNY Mellon Markets. The risks will not just be across different products but will also be a problem across different currencies.

Minimizing Mismatches

Since SOFR rates started to be quoted in April last year, exchanges have joined the fray. CME Group launched one- and three-month futures based on SOFR the following month. CME says from a slow start, average daily volumes had swelled to 38,533 futures contracts by March 2019.

The more futures are traded, the more liquid the off-exchange derivatives like swaps should become. “It is expected that this market will continue to develop and gain increasing acceptance,” says Jeffrey Pearsall, managing director at Philadelphia-based financial consultancy PFM Swap Advisors.

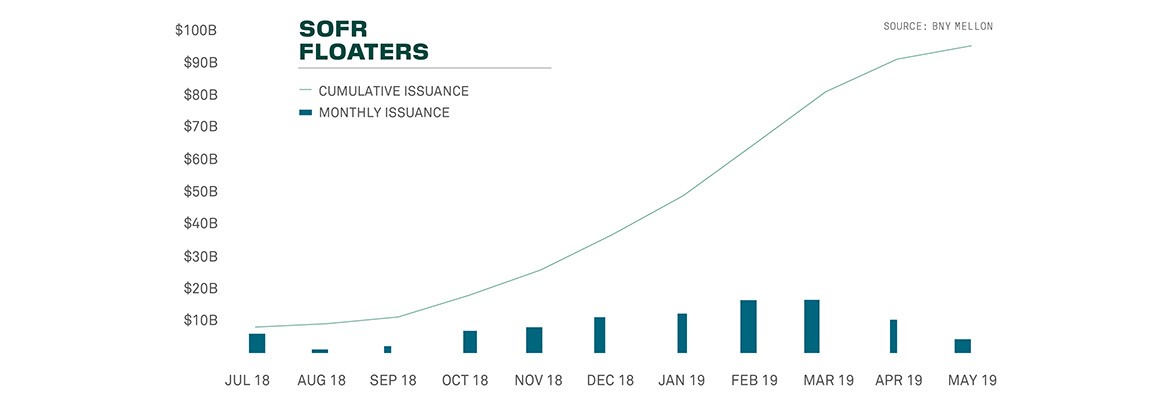

This year through July 12, $140.1 billion in swaps tied to SOFR have traded and were reported to US data repositories, according to ISDA. Only three issues to date have used the compounded SOFR calculation methodology that is being used for derivatives and is expected to become the market norm: a $1 billion floating-rate note in November from the European Investment Bank, a $1 billion one from Goldman Sachs Group Inc. in May, which reportedly received $2.25 billion in orders, and a $750 million one from Morgan Stanley in June.

“Many clients are well advanced with their planning, but we would encourage them to engage now with the system providers and infrastructures they rely on.”

— PHIL WHITEHURST, LCH

Today, many participants are used to knowing their borrowing costs in advance. To approximate this for the new benchmarks, the market compounds SOFR futures pricing over three months to deduce a term rate. Practically speaking, this means the exact interest rate that firms will receive or pay will not be known until after market events, such as Fed interest rate moves.

Many became concerned when SOFR spiked at year end, as overnight rates tend to do.

Some say those uncertainties and the month-end swings in SOFR rates aren’t much more challenging than the LIBOR rate that was open to manipulation in the first place. In April, the ARRC weighed in on the appropriateness of overnight SOFR and laid out options which can be used to alleviate concerns for a variety of market participants.

“It’s not clear to me that the status quo volatility with SOFR is any worse than what we had with LIBOR,” says Gilbert at PwC. “People can understand SOFR and relate it to the underlying market a lot easier than the estimates that came with Libor.”

BNY Mellon’s Lynch says developing a term rate for SOFR rate involves “some major challenges” and market participants cannot afford to wait for it to be available before pricing contracts. Instead, traders should adapt to backward-looking rates in the near term since liquidity may not support a term rate for some time.

Operationally, having contracts with two different benchmarks may also be difficult to manage. Alan Ganucheau, treasurer at Hancock Whitney Bank, a bank in Gulfport, Miss., says matching up assets and liabilities that may be benchmarked against different rates is tricky. If some rates suddenly switch away from LIBOR and some don’t, that creates an unwanted “basis” mismatch.

“Managing that basis risk between the two sides of the balance sheet is a challenge.”

— ALAN GANUCHEAU, HANCOCK WHITNEY BANK

Another concern is that during another financial crisis, the overnight SOFR rate will likely decline as institutions rush into the safety of US Treasuries. At the same time the cost of unsecured borrowing could rise sharply. “Suddenly I will be borrowing at a higher rate but receiving a lower rate for my assets, so managing that basis risk between the two sides of the balance sheet is a challenge,” says Ganucheau.

Still, while the series of unknowns could tempt firms to hold back on beginning their preparation and analysis, there are enough certainties to act on now. SOFR is trading, so new products can be approved; compounding methodologies have been established for new debt issues so system changes can be made; and new fallback language has been issued for contracts.

“If you hold out hope of a term rate, you risk falling behind on execution and planning,” says Lynch

Questions or Comments?

For interest-rate derivatives contact Timothy Comerford; for FX forwards contact

Paul Matherne or for other questions, reach out to your usual BNY Mellon relationship manager.