Is Finance Finally Listening to Women?

What Women in Finance Want

Is Finance Finally Listening to Women?

What Women in Finance Want

March 2022

By Katy Burne

Are financial services firms finally listening to women? The escalation of diversity, equity and inclusion strategies suggests that they are. We spoke to the experts about what women want and why flexibility is only the beginning.

When Rachel Harris went back to work after having three children and two pauses, it was part of a returners’ program at Goldman Sachs. She trialed different departments, updated her skills and built her confidence back, while retaining the flexibility she needed to manage life complications at home. “They really put us on a pedestal,” she recalls. “There was nobody we couldn’t network with.”

Today, having recently joined Schroders after a stint at Aviva Investors, Harris is chair of the returners’ workstream at the Diversity Project, a cross-company initiative that aims to boost the number of returners in the U.K. investments and savings industry. She says the key to fixing the broken talent pipeline in financial services comes down to being agnostic about male and female leave.

Those beliefs echo a growing movement across Wall Street. As finance is changing, so are the day-to-day experiences of women working in finance. Banks, brokers and investment managers are embracing a host of progressive strategies and policies aimed at supporting and advancing women, putting family at the heart of workplace culture and back-to-office planning.

The policies are mostly in their infancy. Nevertheless, they are an unmistakable sign that financial services firms want to reflect the gender-balanced nature of society itself, after decades of criticism for having male-dominated, unbending cultures. They also amount to a recognition that it is not women who need fixing, but the environments in which they sit, and that the responsibility for shifting those cultural norms should fall on all genders equally.

The goal of equality is an ambitious one, particularly for an industry infamous for its boys’ club mentality. But as finance seeks to democratize access to its products and services and move away from its historical reputation, experts say more guarantees of work-life balance, and hard diversity targets, are needed to counter the perception that successful careers in finance demand long hours and too many personal sacrifices.

Slow Progress

Whether it is by offering equal and shared parental leave, hiring women returning from extended leave, allowing flexible working or offering subsidized childcare or eldercare, financial firms are offering a much larger array of family-friendly initiatives than they did just a few years ago.

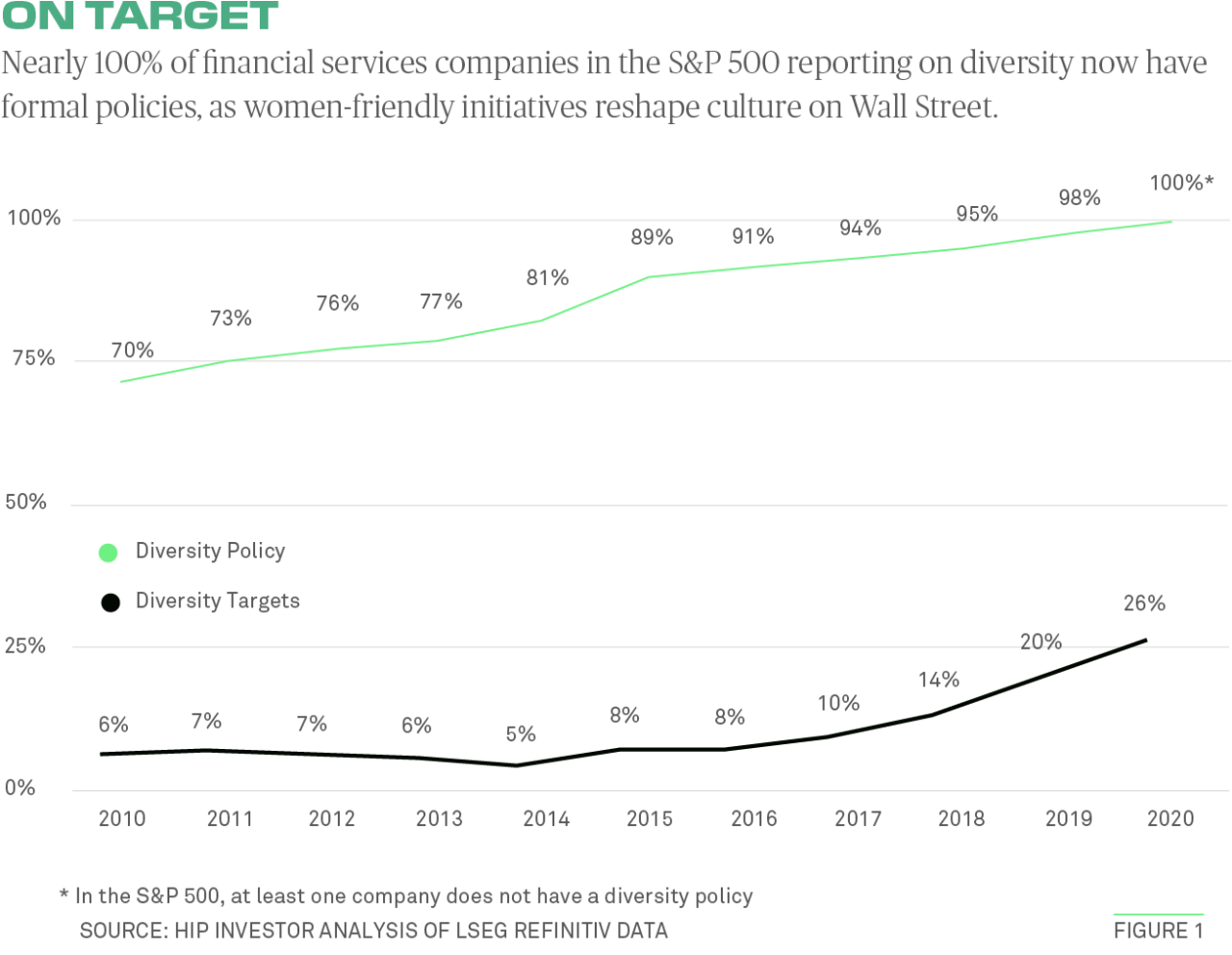

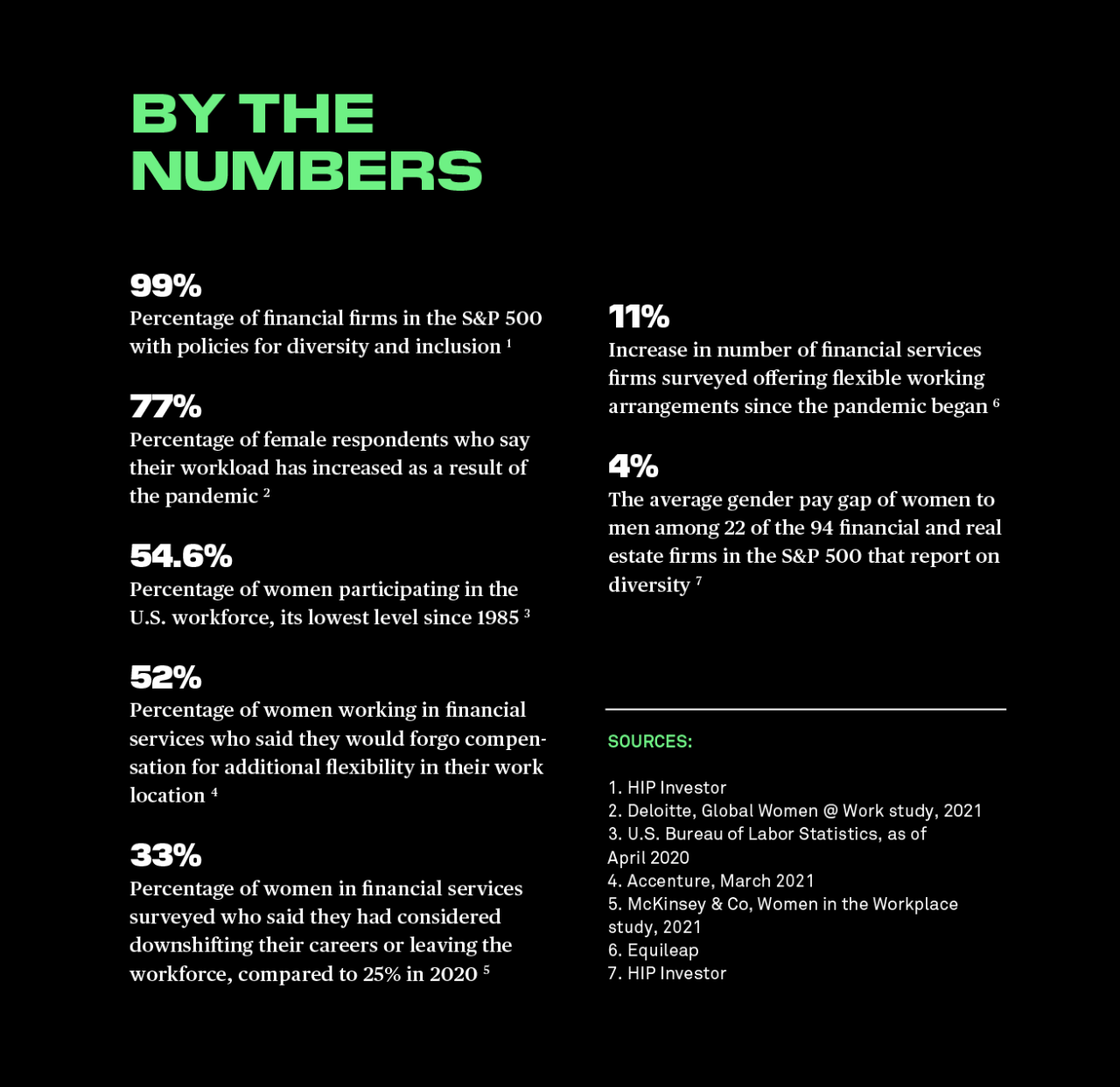

Some 99% of financial firms in the S&P 500 have policies for diversity and inclusion, according to independent researcher and ratings provider HIP Investor, with 26% having hard targets for advancing women into leadership (see Figure 1). In 2015, only 89% had diversity policies and 8% had diversity targets. In the Dow Jones Industrial Average, more than half of the companies have diversity targets.

So far, most of the action has been at the top. According to McKinsey & Co., over the past three years, the share of women at the senior vice president level has grown by 40% and in the C-suite it has increased by 50%, albeit off a low base. The heads of Citigroup, Fidelity Investments, Franklin Templeton, TIAA and the markets division of the Federal Reserve Bank of New York are all women—and mothers.

Still, despite some progression in the C-suite and some evidence of parity at the graduate level, the progression of mid-ranking women tends to stall. After the entry level, studies show women find it difficult to advance because the support structures do not generally exist that would allow them to contribute on their own terms without giving up on personal milestones. As a result, they are often forced to make hard choices that men can sometimes avoid.

Other age-old issues are lingering, too. Among 22 of the 94 financial and real estate firms in the S&P 500 who report on diversity, the average gender pay ratio is 96.3%, meaning women are making about 4% less than men, HIP data show. The gender pay gap in the U.K. between female and male financial managers and directors, by median gross hourly earnings, was 30% as of April 2021.

The dearth of women at all levels of finance has repercussions beyond the industry itself. For example, women are less likely to invest than men. According to a 2021 survey by BNY Mellon Investment Management (IM), if they invested at the same rate, there would be $3.2 trillion in additional capital invested in the financial services industry, with $1.87 trillion directed to areas that would benefit society and the environment.

Another unresolved problem is the lack of adequate funding going to women- and minority-owned start-ups. Deloitte says women were leading 1.3% of fundraising in fintech by 2019, up from 0.6% in 2015, but men are still writing most of the checks.

Some researchers say that the recently deployed diversity, equity and inclusion (DEI) policies are helping to tilt the field more in favor of women, but that the pendulum has a lot further to swing, especially for women of color.

More extensive deployment of the programs, and a greater clarity about what arrangements are working, could give women the support they need when they are facing challenging, family-centric choices at home and might otherwise consider leaving financial services.

Better Balance

What women want in finance is similar to what they seem to want in other sectors, only it may be perceived to be harder to achieve in finance because of the competitive culture and rigid market trading hours.

Flexibility is just the beginning. Women also want workplace cultures that encourage smart working; the ability to have children without being penalized; and to have equal opportunity to promotions, including into full front-office jobs even when they are working flexibly.

As it stands, a Cambridge 2021 study showed that women are more likely to depart the financial services sector than men. According to the survey last year that Hannah Younger, an investment banker and executive MBA at the U.K. university, conducted with 78 women in financial services, this attrition stems from two main factors: a single-event trigger like the decision to have a child or a lack of a support structure, such as a role model who can drive effective cultural change or mentorship.

The No.1 solution the respondents in Younger’s study suggested would make women happier was shared parental leave and a policy of enforcing men to take it. Other ideas included formalized sponsorship programs and more agile working structures such as job shares and smart working.

The COVID-19 pandemic became an inflection point for conversations about flexibility, as data showed that women grappled with the lion’s share of caregiving duties and responsibilities while working from home, whether related to children or elderly family members.

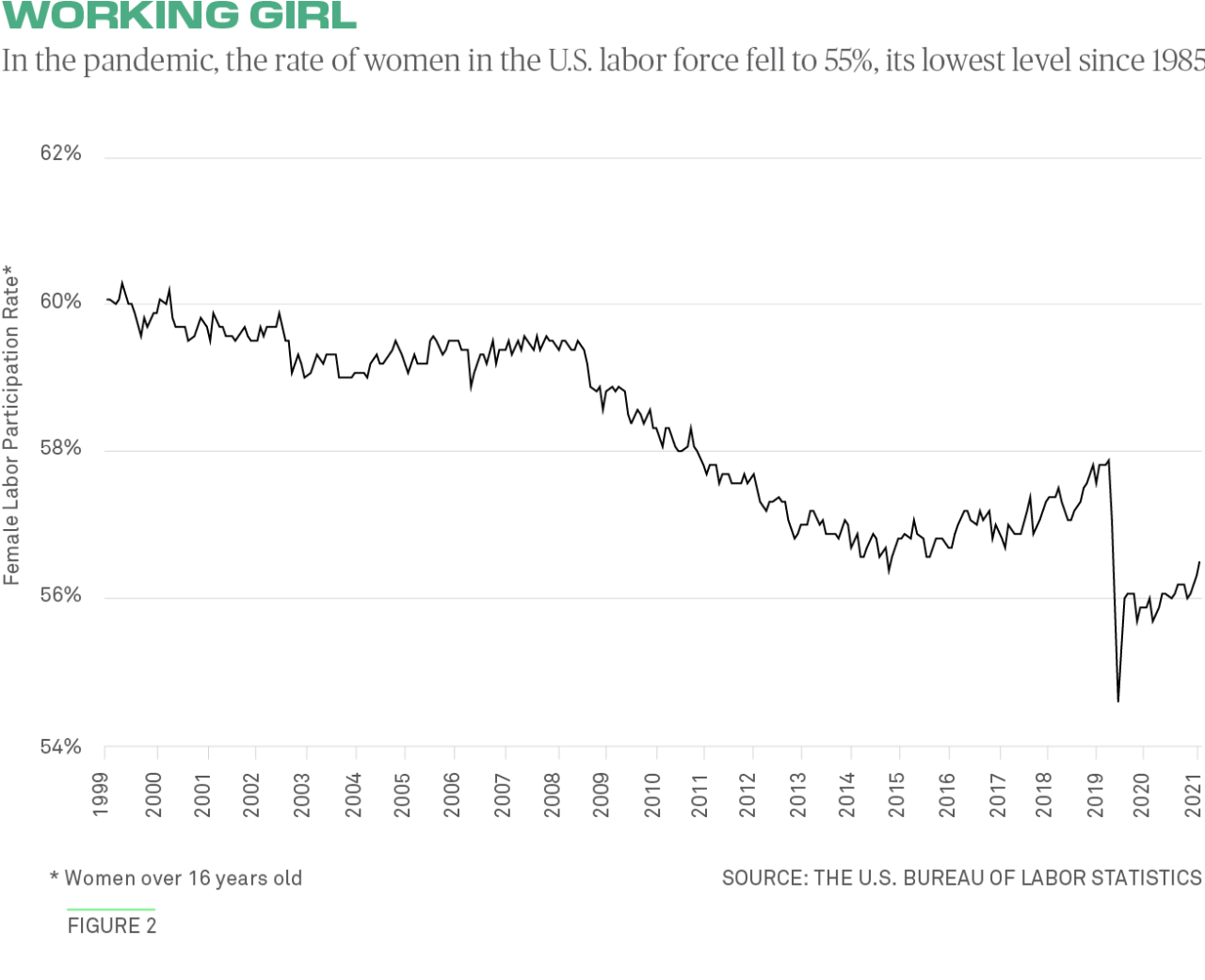

Seeing this, the White House last October launched a national strategy on achieving gender equity and equality, noting that the pandemic had sent female participation in the labor force plummeting. The U.S. Bureau of Labor Statistics put that rate at 54.6% as of April 2020, its lowest level since 1985 (see Figure 2).

Nearly 80% of women surveyed in 2021 by Deloitte in its Global Women @ Work study said their workloads had increased as a result of the pandemic, at the same time as the data suggested they were taking on a larger share of household and childcare duties. “If we could turn the needle toward outcome not hours, I think you’ll see more diversity and equity in finance,” says Monica O’Reilly, U.S. financial services leader at Deloitte.

For the first time in the history of the Women in the Workplace study, started by McKinsey & Co. and LeanIn.Org in 2015, women disproportionately described the need to leave their jobs or step back because of those uneven household experiences. One in three women surveyed said they had considered downshifting their careers or leaving the workforce in 2021, compared to one in four at the start of the pandemic in 2020. Mothers were two times as likely as fathers to worry about caregiving responsibilities affecting their careers and work performance. And two-thirds of women in senior roles had male partners who were also working full time, whereas the female partners of senior men were mostly not working full time or not working at all.

According to McKinsey’s study, women start out underrepresented in hiring, face steeper challenges than men on their first step to manager, and women of color are even less likely to overcome that “broken rung.”

One way to address the mismatch is to offer greater flexibility around remote working and the ability to define and adjust working hours for all employees, without any impact to an employee’s potential for progression. “It’s all wrapped up around this idea of rethinking flex time,” says Alexis Krivkovich, managing partner in McKinsey’s Bay Area office. “If we want creativity, a three-hour commute to an office just gets you supervision; it doesn’t get you creative combustion.”

More than half (52%) of women working in financial services, including six in 10 (62%) in senior management roles, said they would forgo compensation for additional flexibility in their work location, according to Accenture research conducted last year across 500 women in banking, capital markets and insurance in the U.S.

“Flexibility shouldn’t be a trade-off against pay,” notes Rob Dicks, the consultancy’s leader for North America talent and organization in capital markets.

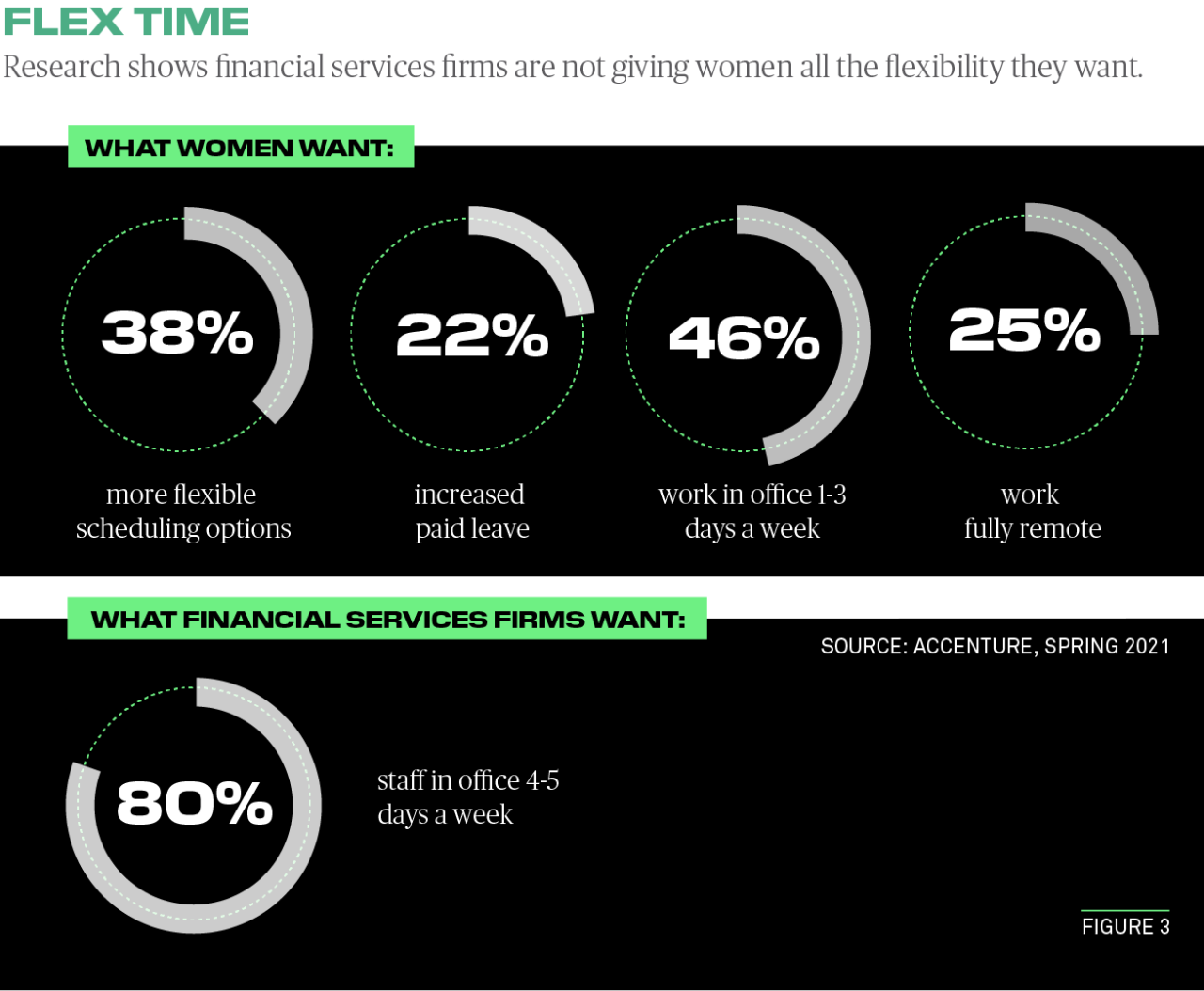

When evaluating employees, managers should be mindful about measuring individual contributions and avoiding any bias toward their work location, Dicks explains. This might help to forestall the risk of women who work from home more often losing career opportunities to staff who are present in the office more. Accenture’s 2021 research suggested 80% of financial firms wanted employees in the office four to five days a week, whereas 46% of women only wanted to be in one to three days (see Figure 3).

Technological advances are also allowing women more choice about how they execute their jobs, much like the BlackBerry put the desktop in the palm of the hand more than two decades ago. Digital tools like Microsoft Teams provide the ability to create, record and measure conversations over periods of time, so that instant availability is less of an issue for employees. “Chat messaging platforms are helping people to connect in asynchronous ways, normalizing work exchanges that can be stretched from minutes to hours or even a few days,” says Dicks.

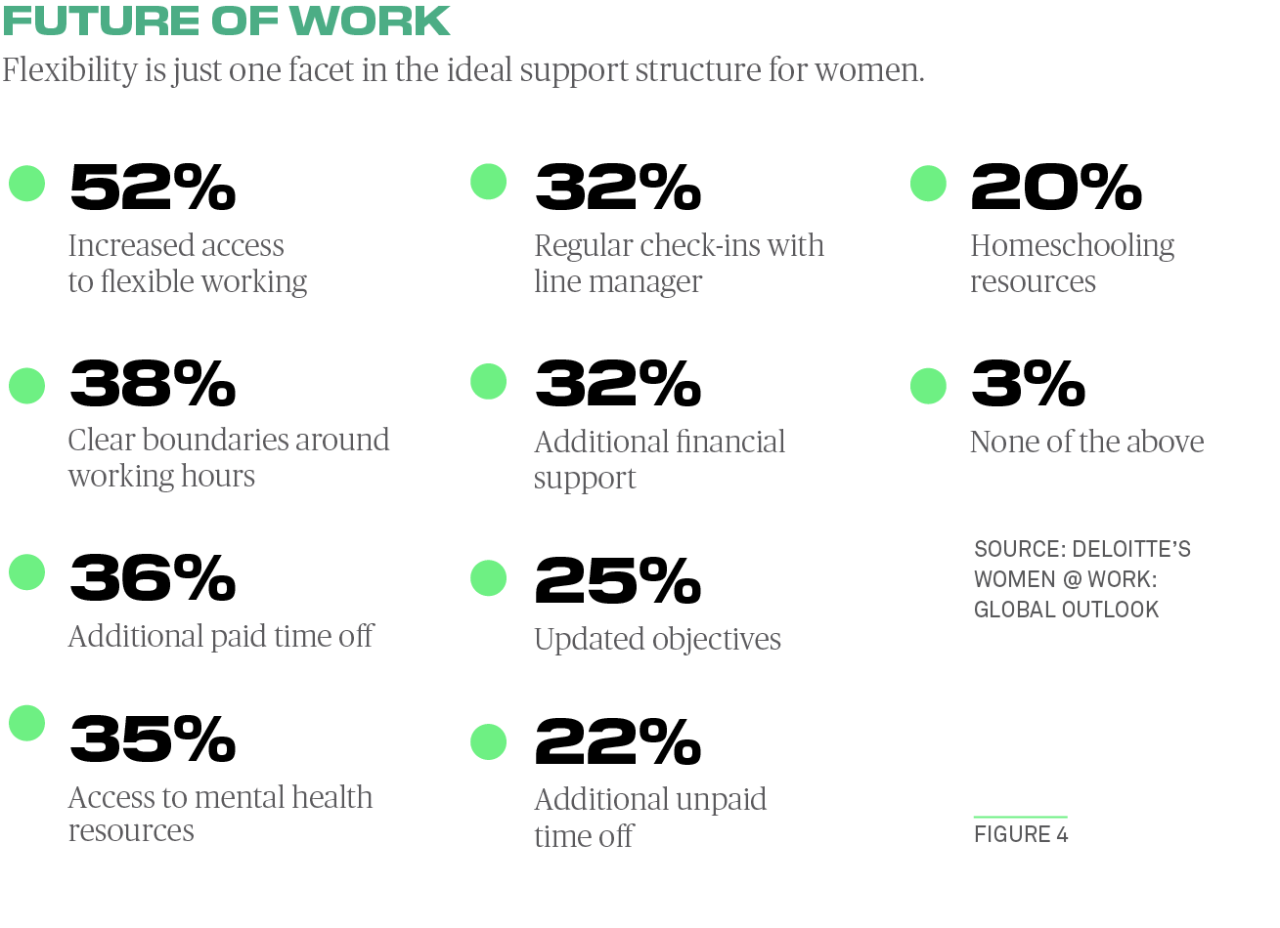

To level the playing field and make women happier, companies are introducing things like flexible working, job sharing, part-time hours and other schedules (see Figure 4). Since returning to work after her third child, Clare Kelliher, senior manager in program execution services at EY, has been able to work full time during the school term and take off when her children have school holidays, something known as a term-time working arrangement.

“I think if work is more life-shaped, people are more likely to be engaged, productive and committed to their employer, whether someone has caregiving responsibilities or not,” she explains.

Male Allies

A key question among diversity and inclusion practitioners is whether such strategies will be set back by the pandemic because it shifted employers’ immediate focus to more urgent concerns such as daily liquidity and remote working technology. Others see the global health crisis as having having accelerated the need for such policies.

“Previously we had not seen much willingness of firms to disclose and offer flexible working policies to employees, but we are now seeing major changes as we reach the two-year mark of the pandemic,” says Diana Van Maasdijk, co-founder and executive director at gender equality data provider Equileap.

Equileap data show 52% of financial services companies now offer at least 14 weeks of paid primary care leave, up from 41% in 2019, and that the number of firms offering flexible working arrangements has risen 11% since 2020.

Women have been responsible for some of that progress, championing other women and DEI policies during the pandemic. But men—sometimes known as “male allies”—have also been critical in supporting women as these programs have flourished, advocating for them as mentors and actively giving them opportunities to stretch.

When there are not enough women in leadership roles and on boards, evidence shows that male allies can shift legacy biases inside financial services organizations and help to elevate the contributions of women from diverse sets of backgrounds.

“ If we could turn the needle toward outcome not hours, I think you’ll see more diversity and equity in finance.”

— MONICA O’REILLY, DELOITTE

“Women cannot address gender imbalances in the workplace alone. Men have an important role to play as powerful stakeholders in most large companies, advocating and taking action to support a more equitable workplace,” says Andrea Pfenning, COO of BNY Mellon’s Government Securities Services Corp.

Diversity experts are quick to point out that flexible working arrangements should apply equally to all genders, irrespective of a person’s caregiving responsibilities. While more women in finance have been asking for the flexibility they need, and in many cases getting it, some men have been discouraged from doing so out of a fear that they might be seen as slacking off, some of those experts said.

Out of a hyperawareness of the challenges at the height of the pandemic, BNY Mellon introduced a global caregiver leave policy, which provides up to 10 days of leave for a parent needing to take care of a sick child if school is closed, or a family member contracts COVID-19. So far, more than 3,000 employees have used it. The bank is also looking into allowing employees to work from anywhere for two weeks each year, with restrictions on certain roles and locations.

Research by McKinsey suggests policies and services such as equal paid leave, emergency childcare and subsidized childcare should be considered standard, however. While the financial industry has made good strides at developing surface-level initiatives, the financial services workplace of the future needs to go even further. BNY Mellon’s own Women's Initiatives Network (WIN) community, for example, is part of the firm’s commitment to fostering an inclusive workplace culture with genuine development opportunities for women and specific targets for diversity.

“Without having senior women and male allies making flexible work a practical reality and modelling these behaviors in the day-to-day, regardless of how far we advance policy, working women may often feel like they need to ask permission—and by the time they have it, it might be too late,” says Maura Creekmore, co-head of Wealth Solutions at BNY Mellon’s Pershing.

No Cigar

Technology companies may have something to teach financial services firms as they look to correct cultural imbalances. Many tech companies have experimented with four-day work weeks, routines that are almost unheard of in regular full-time financial services jobs. They broadcast these benefits internally and aggressively when recruiting.

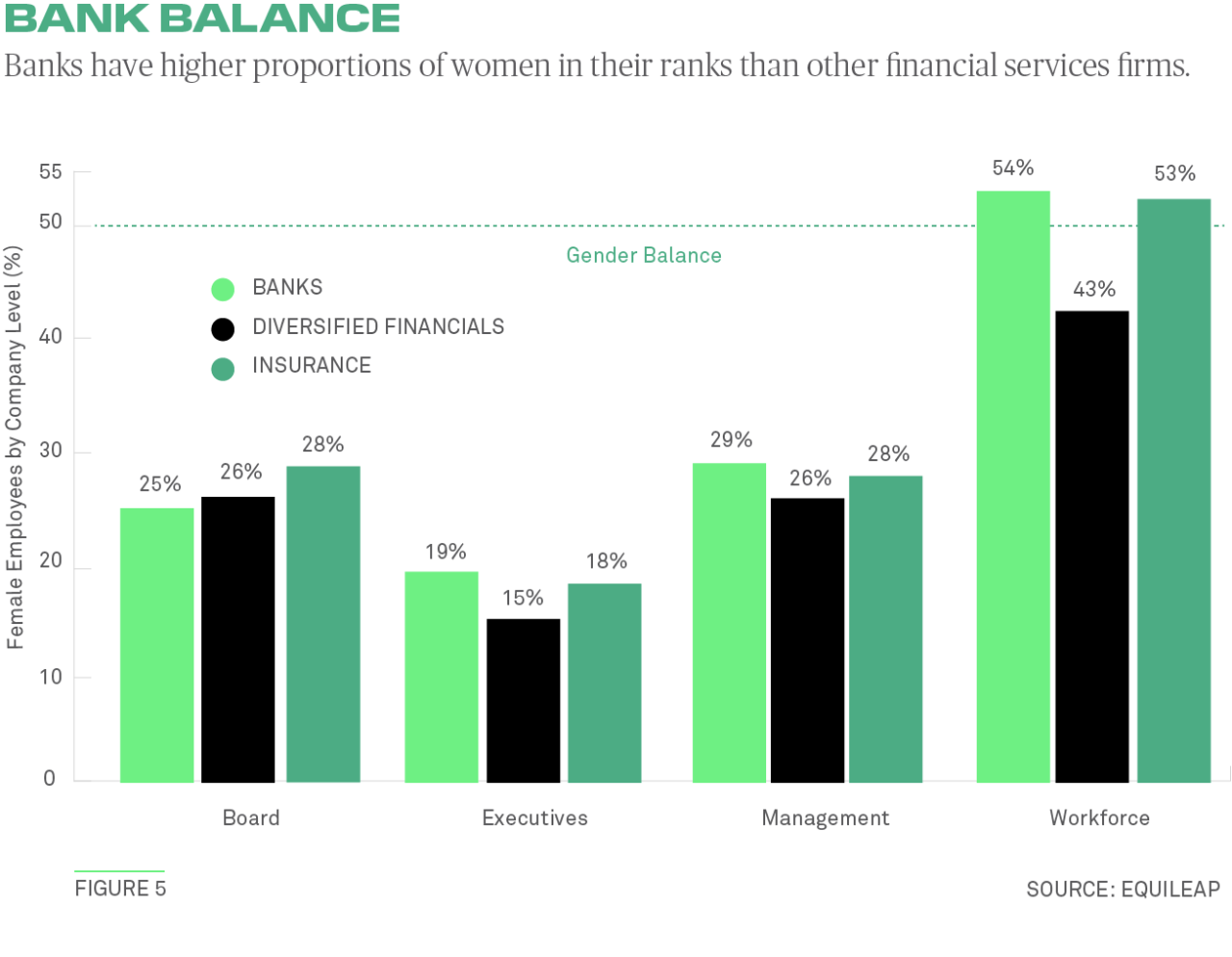

Financial firms are making their own overtures, with banks seemingly attracting more women in their ranks than other financial firms (see Figure 5). But the research shows the industry needs to do even more to put women into revenue-generating positions and give women other female senior role models for advancement. Putting women into sales- and relationship-based positions can be particularly impactful because women are often controlling the larger share of wealth at the client end, whether it was earned or inherited. By one McKinsey estimate, women will inherit enough money to control $30 trillion of U.S. wealth by 2030.

The issue today is that the image problem suffered by big banks, and finance in general, is contributing to a lack of entry-level candidates for female financial advisor roles, says Heather Goodman, COO of TRUE Capital Management, a wealth manager specializing in athletes. “The perception is that finance is cut-throat but women are [sometimes] better at it than men,” she says. “Wealth management is a sales- and relationship-based business, so the opportunities for growth and flexibility should be the appeal.”

Having lower earnings during their careers also impacts women, and women of color’s, ability and confidence to invest like their male counterparts, and their ability to use investing to build generational wealth.

Closing the talent, pay and funding gap is not just a moral imperative, it’s a financial one. Research from Pipeline Equity, across 4,161 companies in 29 countries, shows that for every 10% increase in intersectional gender equity—encompassing all genders, races, ethnicities and ages—there is a 1-2% increase in revenue.

Pipeline’s API connections feed into client company HR systems so that when they make talent decisions, the software can intercept those decisions, de-bias them, and then make recommendations that are both equitable and in the company’s best financial interest.

“Intersectional gender equity is a quantifiable economic opportunity, not only the right thing to do,” says Katica Roy, Pipeline’s founder and CEO.

It is unclear if the financial services industry can change external perceptions of its norms and reach gender parity, especially considering the new intake of graduates are more demanding of their work-life balance.

“Women cannot address gender imbalances in the workplace alone. Men have an important role to play as powerful stakeholders in most large companies, advocating and taking action to support a more equitable workplace.”

— ANDREA PFENNING, BNY MELLON

But the industry is making a concerted effort. In the U.K., more than 300 financial firms have signed up to a government charter to get more women into finance. As of September 2021, 39% of leadership positions at signatory firms were held by women. In some cases, women in U.K. finance roles have been offered 30% raises to move firms, including guaranteed bonus buyouts.

Management support and trust can help to stem the attrition of women from finance, too. Managers can flex their leadership styles depending on the pace and location of someone’s work, and they can be more transparent about the decisions they make when determining salaries, promotions and raises, so that there are no secret rules for success. Without brighter lines on these factors, women with the necessary experience will struggle to advance, and the financial services pipeline will suffer from a permanent supply-demand imbalance.

Some respondents in Younger’s Cambridge research said their employers had these sorts of policies and other women-friendly initiatives, but that they were too recently deployed and not effectively communicated, so they were under-utilized and failed to have a lasting impact.

“The pandemic has presented the financial services sector with a golden opportunity to level-set the workforce and plan for a return to work that will foster better diversity and inclusion for all,” Younger says.

Katy Burne is editor-in-chief of Aerial View Magazine and a flexible-working mother of two.

Questions or Comments?

Contact Katy.Burne@bnymellon.com or your usual BNY Mellon relationship manager.