Active ETFs: The Next Act

Active ETFs: The Next Act

What’s Driving the Boom in Active ETFs and What’s Coming

July 2021

By Ben Slavin

A boom in actively managed ETFs could be just the start of a shift in a $9.4 trillion industry that has long been a bastion of index-tracking investments.

Investors could be forgiven for failing to notice the 2008 debut of the first actively managed exchange-traded fund (ETF).

Bear Stearns launched the first ETF that invested based on the discretion of human money managers instead of tracking an index just one day after J.P. Morgan Chase & Co. upped its firesale bid to buy the beleaguered investment firm. It was an inauspicious beginning: the Bear Stearns Current Yield Fund survived for less than a year.

Since then, market mavens have repeatedly proclaimed the imminence of the long-awaited boom for active ETFs. This year may finally prove them right.

After more than a decade of fits and starts, active management is gaining traction in ETFs, an industry long viewed as nearly synonymous with plain vanilla index investing. Investors are flooding in at a record pace, enticed by triple-digit returns of some funds and a potent cocktail of pandemic jitters, inflation fears, and interest rate anxiety. Inflows into actively managed U.S. ETFs in the first six months of this year topped $55 billion, swiftly approaching the 2020 full year intake of $59 billion, according to Morningstar (see Figure 1).

Currently, the largest of these funds is the ARK Innovation ETF (ARKK), the flagship fund from ARK Investment Management, a boutique asset manager run by Cathie Wood. The fund raked in more than $15 billion in new investor cash in the past year to become the largest actively managed ETF in the U.S., according to ETF Database. ARK’s other active ETFs are also growing, buoyed by a $17.8 billion haul for the full year ended June 30.

While some investors have been swept up by the eye-popping gains of a few thematic funds, others are seeking safety in active management. Discretionary strategies that use options to limit exposure to stock market downturns have become an increasingly popular way for savers to stay in the stock market, according to reports. And companies sitting on piles of cash are snapping up ultra-short debt ETFs, trying to offset the zero-interest drag of money markets while minimizing the interest rate risk inherent in longer-term bonds.

“Investors out there finally get it,” said Ben Johnson, director of global exchange-traded fund research for Morningstar. “‘Active ETF’ is not an oxymoron. There are a number of funds that have enough of a track record to show they can deliver.”

Passive Legacy

Since the first ETF launched nearly three decades ago, the industry has grown in lockstep with the sort of index tracking strategies championed by the late Vanguard founder John C. Bogle. Bogle sometimes criticized the high fees charged by many mutual funds, whose stock pickers rarely outsmarted the market, according to MarketWatch. Bogle suggested that investors could, at times, be better off investing in inexpensive funds that mimic diversified benchmarks.

His idea caught on, accelerating in the wake of the financial crisis. In August 2019, assets in passive U.S. equity mutual funds and ETFs overtook active for the first time, according to Morningstar.

While that trend shows little sign of an outright reversal, active managers are clawing back some ground. To be sure, active ETFs remain a small piece of the $9.4 trillion global ETF industry, accounting for roughly 4.2% of assets, according to ETFGI, an independent research and consulting firm. But that may be changing. Worldwide assets in active ETFs have more than doubled since the end of 2019, ETFGI data show.

“This year is really the year that we’re seeing net flows into active pick up,” said Deborah Fuhr, founder and managing partner of ETFGI.

Asset managers have accelerated their active activity, staking out new territory in ETFs. In October, BlackRock’s iShares unit launched three new transparent actively managed ETFs, including offerings that provide unique exposure to remote work technology innovations.

“Investors out there finally get it. ‘Active ETF’ is not an oxymoron. There are a number of funds that have enough of a track record to show they can deliver.”

— Ben Johnson, Morningstar

Last year, the industry also saw the long-awaited debut of the first active non-transparent ETFs; there are now three dozen active non-transparent ETFs on the market. This year, firms such as Putnam Investments, T. Rowe Price and Fidelity Investments introduced ETF copycats of popular active mutual funds, including an ETF version of the $27 billion Fidelity Magellan fund. Vanguard, meanwhile, launched its first actively managed bond ETF.

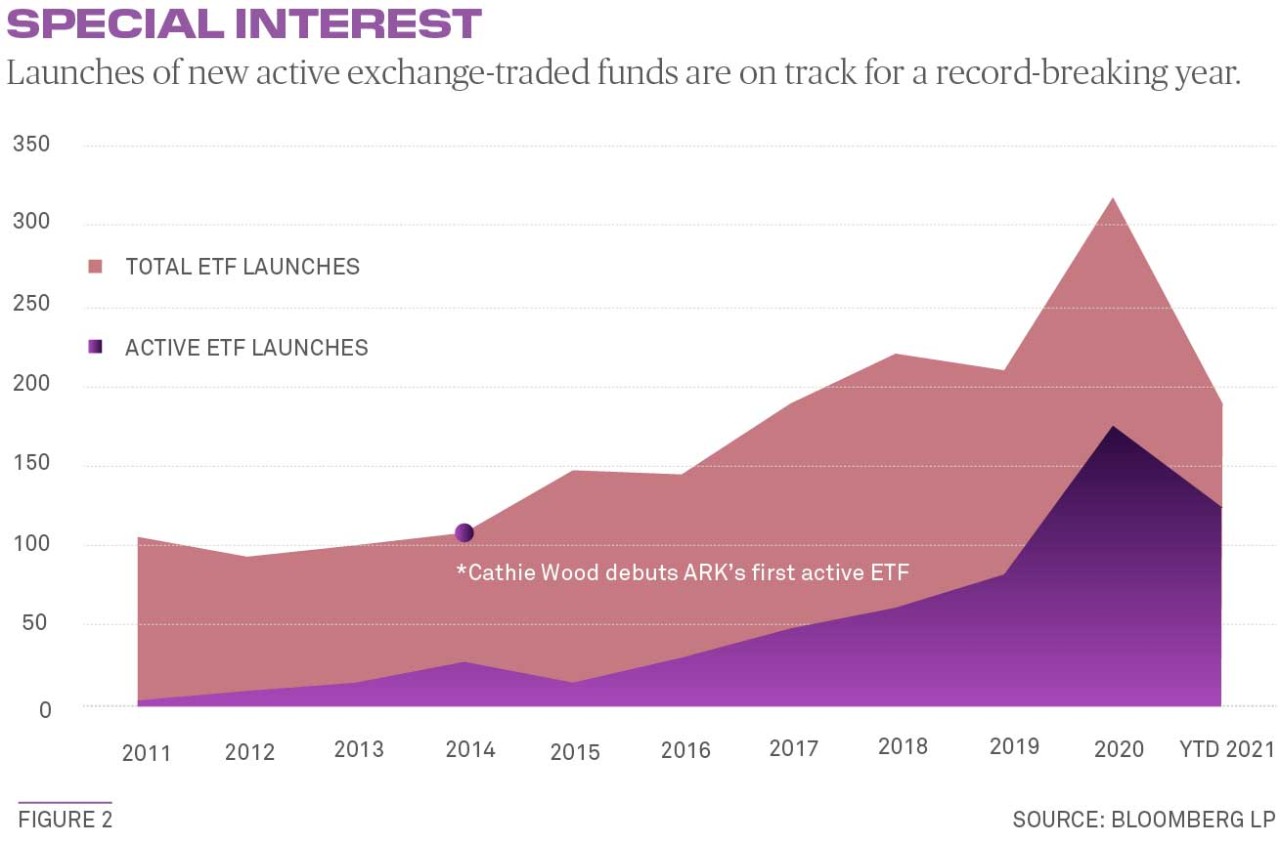

In March, Guinness Atkinson Asset Management completed the first ever conversion of mutual funds into ETFs. Dimensional Fund Advisors followed suit in June, converting four actively managed mutual funds into ETFs, bringing over roughly $30 billion in assets. It was the largest conversion to date, and instantly made DFA one of the 15 largest ETF issuers. So far this year, actively managed ETFs account for nearly 66% of new ETF launches in the U.S., a record, according to data from Bloomberg (see Figure 2).

Behind the Boom

The recent surge is owed to a confluence of circumstances, including two major regulatory changes that made ETFs far more appealing to would-be issuers. In September 2019, the U.S. Securities and Exchange Commission approved the so-called “ETF Rule,” which standardized the regulations for launching and operating ETFs. That same year, the SEC approved the first active non-transparent ETFs, removing a major hurdle that had kept many active managers on the sidelines.

“The ETF Rule leveled the playing field,” said Stephanie Pierce, chief executive officer of ETF, index and cash investment strategies for BNY Mellon Investment Management.

BNY Mellon has filed a registration statement with the SEC to add the first active fund to its ETF lineup, an ultrashort fixed income fund. Ultra-short and short-term debt funds have been one of the most popular segments of the active ETF market, according to a NASDAQ report, as the prolonged era of near-zero interest rates has asset managers and corporate treasurers hunting for safe ways to boost yields.

This year, BNY Mellon also plans to make ETFs from several fund companies available through its short-end investments platform, LiquidityDirectSM.

“Our clients are taking a more sophisticated view in terms of how they manage cash,” said Pierce. “I think we’re going to see more clients who used prime money markets in the past start to use ultra-short-term alongside, or in place of, prime funds.”

Slow Start

The very first ETF — the SPDR S&P 500 ETF Trust — debuted in 1993, but it took another 15 years before the first actively managed ETF reached the market.

After the 2008 Bear Stearns debut, other firms quickly followed suit. PowerShares, now part of Invesco, launched an active fixed income ETF as well as the first active equity ETFs.

Some 54% of respondents to a survey from J.P. Morgan and TrackInsight said they are invested in active ETFs today, up from 31% a year earlier, with 35% saying they would increase their exposure over the next few years (see Figure 3). The share of investors with an exposure of more than 20% to active ETFs has already risen from 4% to 14% (see Figure 4).

“I was surprised — I still am — how long it has taken for active [ETFs] to catch on,” said John Southard, co-founder of PowerShares Capital Management, and now co-founder and chief investment officer of Innovator, another ETF shop.

It wasn’t until PIMCO, a leading name in fixed-income investment management, launched an ETF version of its popular short-term debt strategy in 2009 that active ETFs gained real traction. The PIMCO Enhanced Short Maturity Active Exchange-Traded Fund, which trades under the ticker MINT, capitalized on post-crisis demand for higher yields.

“When PIMCO launched MINT, that was a game changer for active ETFs,” said Todd Rosenbluth, senior director of ETF and mutual fund research at CFRA, a research firm.

Like MINT, the most successful active ETFs piggybacked off the reputation of marquee managers like Bill Gross or Jeff Gundlach. When PIMCO introduced an ETF version of its Total Return Bond Fund in 2012, it was touted by CNN as “a litmus test for the actively managed ETF space.” The following year, State Street partnered with private equity firm Blackstone Group to launch the SPDR Blackstone Senior Loan ETF, an actively managed senior loan strategy. In 2015, State Street launched the SPDR DoubleLine Total Return Tactical ETF. The fund, managed by Gundlach’s DoubleLine Capital, was one of the fastest growing ETFs of the year.

MINT proved to be a long-lasting success, reigning as the largest active ETF on the market for more than a decade. Today, that honor goes to ARKK.

“Active managers have long felt that daily transparency could eat into performance. With the new non-transparent offerings those concerns can be largely put to rest.”

— JC Mas, BNY Mellon

Taking Off

“The biggest reason active management is taking off is Cathie Wood,” said Eric Balchunas, senior ETF analyst at Bloomberg Intelligence. “She really showed how investor demand can be there.”

Wood, ARK’s founder and chief investment officer, began her career as an assistant economist for The Capital Group before taking a job with Jennison Associates. She spent 18 years with the firm in various roles, including chief economist, equity research analyst, portfolio manager and director. She went on to co-found a hedge fund, Tupelo Capital, in 1997 before moving to AllianceBernstein, where she spent 12 years as chief investment officer of global thematic strategies, managing more than $5 billion. Her experience taught her to pay attention to ideas that other investors ignored.

After AllianceBernstein, Wood went out on her own. She founded ARK Investment Management in January 2014. Nine months later, she launched ARK’s first actively managed ETFs.

At the time, many stock pickers were put off by the transparency of ETFs. Unlike mutual funds, the vast majority of ETFs must disclose their holdings every day — an anathema for stock pickers who jealously guard their trading secrets. By opening their books, money managers ran the risk that copycats could muscle in on their best ideas.

Instead of shying away from transparency, Wood embraced it. She made ARK’s investment research public. She published white papers, hosted podcasts, and became a regular guest on financial news shows. She sent out regular emails about her trades and publicized her stock picks on Twitter.

ARK’s first three years were a struggle. In 2015, ARK’s ETFs took in a paltry $17 million combined. Her fortunes began to turn in 2017 when two of her ETFs were among the top performers for the year. Since then, the firm’s flagship fund has continued to beat the market. Through June 30, ARKK returned nearly 576 percent in the past five years, 191.6 percent in the past three, and 73.7 percent in the past year, according to ETF Database.

ARK’s suite of active ETFs has grown increasingly popular because the appetite for investing in technological innovation has expanded, said Renato Leggi, client portfolio manager for ARK. The pandemic also boosted interest in market segments such as work-from-home technology, e-commerce, and genomics — all areas that ARK has specialized in for years, Leggi said. “As a result of the pandemic, we’ve seen an acceleration of the adoption of the technologies that we’re investing in,” Leggi added.

While the firm’s flagship ETF returned triple digits in 2020, investors shouldn’t expect those kinds of gains every year, he said. The firm aims for a 15 percent annualized return, but performance can be volatile year to year, Leggi said.

Two actively managed thematic funds from Amplify ETFs delivered triple-digit returns in the past year. Both funds handily outperformed their index-tracking rivals because their portfolio managers can buy and sell stocks more nimbly than benchmark-bound competitors, said Christian Magoon, founder and CEO of Amplify ETFs. By eschewing an index, Amplify’s active ETFs can also invest in IPOs and some of the smallest companies that would be hard to make room for in a passive strategy, he added.

“These are strategies that require you to be opportunistic and dynamic, and that’s hard to write into index rules,” Magoon said.

Active Defense

Not every investor has been drawn to active ETFs because of a few hot thematic funds. Actively managed defensive strategies have also been a popular way to counter market uncertainty.

Innovator’s three-year-old suite of defined outcome ETFs, which use options to protect investors against market downturns, don’t have the same kind of discretionary strategy, but they are nonetheless part of the active ETF marketplace. The funds took in $1.4 billion in 2020, and another $771 million in the first half of this year.

“People still have wealth protection on their minds,” said Southard, Innovator’s CIO. “It’s hard to invest without thinking about protection when stocks are at all-time highs.”

Another active options strategy that's garnering interest is the Quadratic Interest Rate Volatility and Inflation Hedge ETF, run by Nancy Davis, founder and CIO of Quadratic Capital Management LLC. The fund seeks to protect purchasing power and uses an actively managed portfolio of options and inflation-protected Treasuries to profit from the steepening yield curve. In the two years since its debut, the fund has grown to $3.4 billion in assets.

Exchange-traded commodity products have also gained ground as investors try to hedge their portfolio against inflation in raw materials prices. For example, an actively managed commodity ETF from Invesco gained $2.3 billion in inflows in the first half of 2021.

Fixed Income

While thematic and defensive strategies are gaining ground, fixed income is by far the largest segment of the active ETF marketplace. Fixed income ETFs have grown rapidly in recent years as institutional investors, traders, insurers, and corporate treasurers have added ETFs to their fixed income holdings.

Active management has had a firm foothold in the ETF marketplace since the advent of MINT. And for good reason: Fixed income has proven to be an asset class where active managers have a decent track record of beating their indexed rivals, said Morningstar’s Johnson. Roughly 58% of the assets invested in active ETFs worldwide is in fixed-income funds, according to ETFGI (see Figure 5).

One particularly popular segment has been short-term and ultra-short-term debt funds. The JPMorgan Ultra Short Income ETF has taken in $4.6 billion in the past year, growing to more than $17 billion. It’s now the second largest active ETF after the ARK Innovation ETF, just ahead of MINT.

The BNY Mellon Ultra Short Income ETF, expected to launch in August this year and trade under the ticker BKUI, will be sub-advised by Dreyfus Cash Investment Strategies, BNY Mellon's affiliated money market business and the eighth largest money market fund sponsor in the U.S.

“The yield environment is absolutely the driver,” Pierce said. “What we’re seeing is that clients are struggling for yield, but they don’t want the volatility of the longer-term bond funds.”

The Future of Active

The big question is whether the recent boom in active ETFs is a performance chasing blip, or a lasting commitment to active on the part of both ETF investors and issuers. Money managers are clearly hoping there’s still room for growth. In addition to the ultra-short term debt ETF, BNY Mellon has several other actively managed ETFs in registration, SEC records show. Other firms are also gearing up to enter the active market, or to expand their active roster.

“Given the assets in active mutual funds, we’re still in the first inning for active ETFs,” said Brandon Clark, director of the ETF business for Federated Hermes Inc., an active investing firm with $625 billion under management. Federated, which has yet to launch an ETF, plans to introduce its own suite of active ETFs later this year, Clark said.

Today, there are roughly three dozen non-transparent ETFs on the market, though uptake has been slow, said Johnson. So far, only five have amassed more than $100 million in assets, a crucial threshold that demonstrates the viability of an ETF and helps funds gain access to distribution platforms, he added.

But the active non-transparent space should continue to grow as money managers find new ways to wrap their trading strategies into an ETF, said JC Mas, head of equity and ETF trading for BNY Mellon.

“The ETF structure is a more efficient vehicle,” Mas said. “Active managers have long felt that daily transparency could eat into performance. With the new non-transparent offerings, those concerns can be largely put to rest.”

The key to success in active management is understanding what investors are looking for, said Balchunas, the Bloomberg analyst. So-called closet indexers, who are technically active but stick fairly close to the index, will have a hard time standing out, especially if they’re charging higher fees, he said, but when it comes to niche active strategies like those offered by ARK and Amplify, investors are much less price-sensitive.

“Benchmark huggers who play it safe aren’t going to win investors,” Balchunas said. “Investors want either dirt cheap or shiny objects. They’ve got the boring base of vanilla, and they want a pop of active on top.”

Ben Slavin is head of ETF Services for BNY Mellon.

Questions or Comments?

Contact jeremy. kross@bnymellon.com, ron.hooey@ bnymellon.com, or matthew.camuso@ bnymellon.com, or reach out to your usual relationship manager.